CER Apr. 2016

68

ऐዐڟዐڦࡔထ ऐዐڟዐڦࡔထ Adaptive anachronism Adaptive anachronism APRIL 2016 VOL. 27, NO. 1 | www.chinaeconomicreview.com 2016ฤ4Ꮬఓ • Delta forces • Delta forces • Box office boom • Box office boom • • ዐࡔ੨ଭۉฆႜᄽჺ৯Ԓ ߢዐࡔ੨ଭۉฆႜᄽჺ৯Ԓ ߢ• • 3127ႎາኮݕஜᇑ ߌ3127ႎາኮݕஜᇑ ߌ

description

China Economic Review 中经评论

Transcript of CER Apr. 2016

Adaptive anachronismAdaptive anachronism

APRIL 2016 VOL. 27, NO. 1 | www.chinaeconomicreview.com 2016 4

• Delta forces• Delta forces

• Box offi ce boom• Box offi ce boom

• •

• •

ChicagoBooth.edu/impact

Banks Baker, ’05 Head of Publisher Solutions & Innovations, Asia Pacific, Google

HOW DOES THE CHICAGO APPROACH™

HELP BANKS NAVIGATE WHEN CHANGE IS THE ONLY CONSTANT?

Banks Baker has made a career of leading media

organizations into the digital future. There’s

no playbook and the market is moving

in milliseconds. See how Banks has made

The Chicago Approach his own.

Make The Chicago Approach your own

CHICAGO LONDON HONG KONG

Editor-at-large Graham Earnshaw

Co-Publisher Alex Wong Shiu Chung

Executive Editor Graham Earnshaw

Deputy Executive Editor Gao Fei

Associate Editor Rainy Chen, Tom Nunlist

Art Editors Jason Wong

Sales Director Ralph Wang

Account Managers Summer Xia

Distribution Manager Seana Liu

Publisher China Economic Review Publishing

Address The Plaza Building, 102 Lee High Road

London, SE13 5PT, England

Room 1801, 18F,

Public Bank Centre,

120 Des Voeux Road Central,

Hong Kong

ISSN 2073-2570

Hong Kong printer 01 Printing Limited

Suite M, 3/F, Tower 3,

Kwun Tong Industrial Centre,

448 Kwun Tong Road, Kowloon

Hongkong +852 3174 6136

Shanghai +86 21 5187 9633-811

Editorial Department [email protected]

Sales Department (Ads) ( ) [email protected]

EDITOR’S NOTE |

Adaptive anachronism

APRIL 2016 VOL. 27, NO. 1 | www.chinaeconomicreview.com 2016 4

• Delta forces

• Box office boom

•

•

In this issue, China Economic Review takes a look at some

of the big questions of the next phase of the China story, as

reflected in the latest Five Year Plan that will impact fundamen-

tally on China’s economy from this year through to 2021. The

golden years of 10 percent annual growth are clearly behind us,

and the implications of a “new normal” involving slower growth

are only slowly becoming clear. The Plan provides important

insight into how Beijing’s top planners see things. Also in this

issue, we look at the current state of China’s movie industry,

an enormously positive story with booming box office takings

reflecting a shift in middle-class entertainment discretionary

spending habits, and the problems and opportunities raised

by the growing integration of Hong Kong with Shenzhen and

beyond.

China Economic Review | April 2016 03

10

14

22

28

40

20

28

The House View

8 Top-shelf assets

News Highlights

12 News briefs

Cover Story

16 Adaptive anachronism

Economy

30 Delta forces

36 Box offi ce boom

08

15

CONTENT

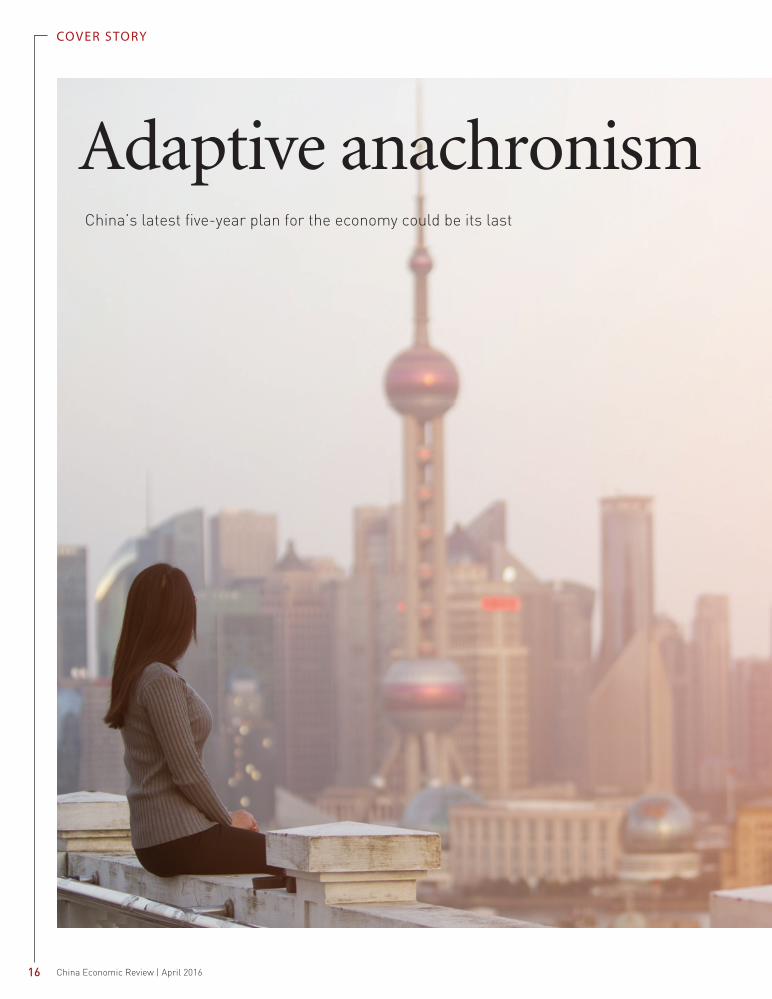

Cover storyAdaptive anachronism16China’s latest fi ve-year plan for the economy could be its last

China Economic Review | April 201604

At EU Business School, you don’t just learn from entrepreneurs, you become one!

Emilija PetrovaManaging Director, Trade Resource GmbHAlumna 2002

Supareak Charlie Chomchan

Managing Director,Pacific Rim Rich Group Co., Ltd.Alumnus 2003

Peter von FortsnerManaging Director, Häusler AutomobilesAlumnus 2010

Roxana FloresFounder, BeCaridadAlumna 2011

Business school is where you build good habits, learn the theory, pick up practical skills and obtain the knowledge necessary to put your ideas into action. You need a business school that will help

you develop both as a businessperson and an entrepreneur. At EU Business School we make a difference in students’ lives and propel them to success.

bH

Managing Director,Pacific Rim Rich Group Co., Ltd.

Managing Director,Häusler Automobiles

Viktor GöhlinFounder, Nokadi Alumnus 2006

Bart van StratenGeneral Manager, Van Straten MedicalAlumnus 1996

Emilija PetrovaManMMMMM aging Director, TTTTTT d Resource GmbTraTrrararararaade ResourceAlummmnammm 2002

Supareak Charlie Chomchan

Managing DirectorPeter von FortsnerM i Di t

Roxana FloresFounder, BeCaridadAlumna 2011

Roxana FlFlFlFloreoreoreoreorer sss

Peter von Fortsner

Viktorr Göö GöhlihlinnFouFoundender,r, NokNokadiadi AluAluuluA mnumnumnumnn s 2s 2s 2s 2s 006006000

BaBarBarBarBaBart vt vvvanan ana StrStrStrateatea ennGenGenGenGenGG eraral MMMMManaa ger, VanVaVanVan Straten MedicalAluAl mnus 1996

YOU!

PEOPLE HAVE IDEAS. ENTREPRENEURS MAKE THEM HAPPEN.BARCELONA | GENEVA | MONTREUX | MUNICH | ONLINE

47

34

35

44

47

54

56

60

63

Business Education Focus

50 Melding two schools of thought

52 Entrepreneurship and

Leadership Trends at EU

Look at China

62 The safe world of cartoons

30

CONTENT

22 36

44

56

China Economic Review | April 201606

THE HOUSE VIE W

China’s outbound investment goes from third-world to fi rst-tier

It was barely a month since China

had capped its biggest year ever for

mergers and acquisitions abroad

when word leaked of another record-

breaking bid: China National Chemical

Corp. was reportedly in talks to buy

Swiss agribusiness giant Syngenta for

around US$43 billion.

Less than a day after reports surfaced

on the deal, Syngenta went public with

plans to accept the offer, launching both

firms running through a gauntlet of

daunting regulatory scrutiny and kick-

ing off 2016 with a deal equal to more

than two-thirds of China’s total US$61

billion in completed outbound merger

and acquisition (M&A) transactions for

2015.

Hypotheticals aside, the deal rep-

resents another resounding volley in a

new direction that has come to domi-

nate China’s steadily growing levels of

international investment.

“Chinese investment abroad has

gone from developing countries with

resources to developed countries with

diverse kinds of assets,” said Derek Scis-

sors, a resident scholar at the Ameri-

can Enterprise Institute and author of

the China Global Investment Tracker,

a database that keeps a running total of

major Chinese investments abroad.

Now, as acquisitions continue to

shift in terms of sector and location,

the Syngenta bid has raised questions

about how big Chinese bids can get—

and exactly which companies will be

making them.

New frontiersAIE’s China Global Investment Tracker

is not the only tool for keeping tabs

on outbound investment by mainland

companies, and estimates vary among

aggregators as to exactly how much

China has racked up in recent years.

But virtually all observers agree there

has been a shift away from investments

in commodities, which previously dom-

inated. The AEI database - the scope

of which is limited to deals of at least

US$95 million that can be directly veri-

fied - makes equally clear who the win-

ners and losers are now that Chinese

investor interest has fundamentally

changed, even as the headline figure for

investment abroad has steadily risen.

Perhaps the most visible impact has

been in resources-rich South America.

In 2010 China invested US$33.84 bil-

lion in the region, most of it in energy.

In 2015 that amount had more than

halved, with investments and contracts

falling to US$16.36 billion.

In Europe the trend is just the oppo-

site: Where Chinese investment sat at

a paltry US$9.11 billion in 2010, the

continent was sitting pretty last year at

US$35.13 billion total. An overview of

Chinese foreign direct investment in

Europe by the Mercator Institute for

China Studies and Rhodium Group

showed the majority of that money

flowing into Britain, France and Ger-

many.

Some countries, such as the US and

Australia, have seen relatively strong

investment growth since the database

was started in 2005 up to today even

Top-shelf assets

China Economic Review | April 201608

THE HOUSE VIE W

after rapid diversification began in

2010. Perhaps the biggest loser from

the developed world in recent years has

been Canada, which has seen Chinese

investment shrink precipitously since

2012, when state-run CNOOC bought

Canadian oil-sands firm Nexen for

US$15.1 billion.

Sector by sectorEnergy and metals were once China’s

longtime outbound investment focus

as it sought to feed a boom in the

mainland real estate market and heavy

industry: Between 2008-2010 the two

sectors accounted for about two-thirds

of total outbound investment.

When the AEI database began track-

ing investment in 2005, energy stood

at 42% of the total; it would eventually

rise to 59% in 2010. Investment in met-

als also grew at a rapid clip early in the

century, rising to 27% of the total in

2008.

By 2015 energy’s share had dropped

to a still-respectable 28% of the total,

but metals accounted for only 5%.

The transport sector’s share of

investment has done just the opposite,

rising from a nadir of about 9% in 2010

to 26% in 2015. Scissors said recent

projects went beyond previous years’

model of in-and-out road building:

Chinese firms increasingly stay on after

completing construction of toll roads

and rail lines to run them, while direct

investment has become concentrated in

airlines, aircraft production, shipping

lines and ports.

Real estate, too, been bolstered

by acquisitions in major global hubs

like New York and London as well as

high-profile cities such as Chicago and

Sydney. Total real estate investment –

including off-the-plan and secondary

purchases –accounted for 17% of the

total in 2015, with tourism adding 2-4

percentage points since it was broken

out into its own category in 2013 to

reflect projects abroad that specifically

target Chinese tourists.

But even the latest top-shelf projects

announced by property tycoon Wang

Jianlin - including a EUR3-billion lei-

sure park in France - don’t measure

up to the tech sector in terms of global

attention paid. Whether that is war-

ranted, however, is another matter.

Tech and technicalitiesIn the US in particular, government

sensitivity to Chinese firms attempt-

ing to acquire tech companies or their

subsidiaries appears to be on the rise.

The latest annual report from the Com-

mittee on Foreign Investment in the US

(CFIUS) placed China in the top spot

for the third year running in 2014.

Together with heavy coverage of

deals that fell apart after drawing inter-

est from the committee - such as when

a consortium of mainland firms walked

away from a US$2.8 billion bid for a

unit of Philipps and Unisplendor’s

withdrawal of a bid for 15% of Western

Digital - appear to suggest Washington

has become uneasy with an influx of

Chinese money into America’s tech sec-

tor.

In a February review of transactions

from recent years that were scrutinized

by the CFIUS, Thilo Hanemann and

Daniel Rosen of the advisory firm Rho-

dium Group argued that the perceived

spike in inspections of Chinese bids was

business as usual in light of concurrent

growth in total transactions.

Not that Chinese firms aren’t mak-

ing a concerted effort to snap up deals

in the US semiconductor industry: The

five confirmed major Chinese bids in

the sector last year were worth a cumu-

lative US$5.78 billion.

But the bids that failed to go through

weren’t shocking in light of industry

history: Fairchild Semiconductors

- which rejected a US$2.5 billion bid

from China Resources and Hua Capital

Management in 2015 - had also been

the target of a 1987 bid from Japan’s

Fujitsu that prompted the creation of

the CFIUS in the first place.

All in or all out?A successful bid for Syngenta would

not only reverberate through the global

agribusiness industry—by dint of its

size, it would also mark the reversal of

a trend that has seen private Chinese

investors account for more and more of

total outbound investment.

“For a long time there was no private

investment,” Scissors said. He noted

that while state-owned firms still domi-

nated per dollar spent acquiring assets

abroad, since 2012 private firms had

seen their share rise to about 30% of

outbound investment.

Even if that share falls, it would still

make for gains by private investment in

absolute terms. But Scissors also point-

ed to the latest wave of notable invest-

ments from companies like Wanda and

Haier as potentially reflecting concen-

trated attempts at portfolio diversifica-

tion in the face of diminishing opportu-

nities at home.

“There may be rounds of this,” he

said, as more companies from differ-

ent sectors sought profits offshore—

though he added the likelihood of that

will depend on how top leaders fare in

handling a welter of challenges now fac-

ing China’s economy. “Nothing is set in

stone.”

China Economic Review | April 2016 09

•

•

China Economic Review | April 201610

China Economic Review | April 2016 11

NE WS ROUNDUP

NEWS HIGHLIGHTS

PBOC reached out to US Fed during summer stock crisisDocuments from the US Feder-

al Reserve acquired by Reuters news

agency through a Freedom of Infor-

mation Act request revealed that the

People’s Bank of China reached out to

the US central bank amid the implo-

sion of mainland equity prices in July

of last year to ask for help. An email

to a senior Fed staffer, the PBOC chief

representative for the Americas pointed

to the Fed’s handling of the 1987 US

stock market crash, noting "my Gover-

nor would like to draw from your good

experience." The email reply included

a short summary of the Fed’s measures

in 1987 and dozens of Fed transcripts,

reports and statements--all of which

were publicly available.

PBOC governor warns China’s corporate debt too highZhou Xiaochuan, governor of the Peo-

ple’s Bank of China, cautioned that

corporate debt levels are too high, The

Financial Times reported, citing com-

ments given at a meeting with business

leaders in Beijing. "Lending and other

debt as a share of GDP, especially cor-

porate lending and other debt as a share

of GDP, is on the high side," Zhou said,

adding that highly leveraged economies

were more vulnerable to macroeconom-

ic risk. The Bank for International Set-

tlements has warned that a recent spike

in corporate and private debt in emerg-

ing markets was "eerily reminiscent" of

the financial boom in advanced econo-

mies ahead of the global financial crisis.

China’s international patent fil-ings jumped 16% in 2015China’s total global patent filings

jumped 16% to 29,846 in 2015 from the

previous year, Tech In Asia reported,

citing data from the World Intellectual

Property Organization on filings valid

in 148 countries under the global Patent

Cooperation Treaty. China smartphone

manufacturer Huawei filed for 3,898

patents, making it the world’s most

active filer for the second year running

and exceeding runner-up Qualcomm

by more than 60%. Huawei competitor

ZTE filed 2,155 patents to come in at

third place globally. While the uptick in

patent filings does not necessarily trans-

late to an increase in feasible products or

innovation, it does suggest China is tak-

ing international patents more seriously.

ENN to purchase $750mn stake in Australian gas supplier SantosPrivate Chinese natural gas distributor

ENN will become the largest sharehold-

er in Australian gas producer Santos

with the purchase of a US$750 million

stake from mainland private equity

fund Hony Capital, Reuters reported,

citing a statement from the distributor.

"We are gaining a strategic investor and

partner in Hony Capital whose deep

China experience and global outlook

can help us accelerate future growth

overseas," ENN Group chairman Wang

Yusuo said. Bankers have said private

distributors in China are seeking to lock

in supplies of liquefied natural gas to

ease their dependence on state-owned

behemoths such as Sinopec, CNOOC

and PetroChina.

China Economic Review | April 201612

China announces first-ever ener-gy consumption capChina released its first energy con-

sumption cap, targeting 5 billion tons

of standard coal equivalent by 2020,

Reuters reported, citing figures from

the latest five-year plan. Yang Fuqiang,

senior adviser at the Natural Resourc-

es Defense Council, said the 5 billion

figure was calculated by combining

China’s 6.5% economic growth projec-

tions for 2016-2020 with its target to

cut energy intensity by 15% over the

same period. "Based on my experience

the government plans are conservative,"

Yang said. "There could be a higher

18% cut in energy intensity, and that

means energy consumption could be

kept at about 4.8 billion tons."

Facebook’s Zuckerberg meets with China propaganda chiefFacebook chief executive and found-

er Mark Zuckerberg met with China’s

propaganda chief Liu Yunshan. Accord-

ing to state news service Xinhua, Liu

told Zuckerberg he hoped Facebook

could share its experience with Chi-

nese firms to help "Internet develop-

ment better benefit the people of all

countries". The meeting is the latest

in a string of thus far fruitless efforts

by Zuckerberg to get access to China’s

hundreds of millions of Internet users,

and comes on the heels of the Face-

book founder’s highly-publicized jog

through Tiananmen Square while air

pollution in Beijing stood at 15 times

recommended levels.

Hebei will shutter 60% of steel mills by 2020Hebei province announced it will shut-

ter 240 of 400 steel factories by 2020,

Caixin reported, citing an announce-

ment from the provincial governor. As

the province weans itself off steel, it will

lose RMB180 billion in revenue and lay

off more than one million workers. New

projects have been banned until the

province reaches a production target of

200 million tons per year. The bulk of

the cuts will be made by smaller opera-

tors with a capacity below 300,000 tons

per year. Concrete production capac-

ity will also be slashed by two-thirds, or

some 60 million tons, and coal and glass

production will be cut as well.

XMC breaks ground on $24bn factory as part of China chip-making driveState-owned contract chipmaker XMC

is investing US$24 billion in building

out its semiconductor production and

supply chain capabilities as part of a

government push to make inroads into

the strategic sector, The Wall Street

Journal reported. An XMC spokesman

said the money, largely from a nation-

al semiconductor fund and provincial

government of Hubei, would be invest-

ed in three stages: an initial factory

focused on flash-memory production,

another plant producing chips, and a

third phase centered on devoted facili-

ties for suppliers. While the massive

project is a first among China’s chip-

makers, many analysts are skeptical the

company can catch up to regional rivals

in South Korea and Taiwan.

China-backed bank says more than 30 countries await member-shipMore than 30 countries are waiting to

join the China-backed Asian Infrastruc-

ture Investment Bank (AIIB), adding

to its 57 founding members, its presi-

dent said. The AIIB, first proposed less

than two years ago, has become one of

China’s biggest foreign policy successes.

Despite the opposition of Washington,

almost many major U.S. allies - Aus-

tralia, Britain, German, Italy, the Philip-

pines and South Korea - have joined.

Tencent’s annual net profit rises 21% to $4.45bn in 2015Chinese online services conglomerate

Tencent reported a 21% increase in net

profit to RMB28.81 billion (US$4.455

billion) for 2015. Total annual revenue

rose 30% from 2014, driven largely by

smartphone games sales and online

advertising, with average monthly active

users of the company’s Weixin social

network and e-commerce platform

rising to 697 million. Chief Executive

Pony Ma said a major goal for 2016 was

to expand Tencent’s advertising busi-

ness - which saw revenue grow by 110%

in 2015 - by adding more mobile adver-

tising inventory. Ma added that Tencent

had no plans to spin off Weixin.

NE WS ROUNDUP

China Economic Review | April 2016 13

China Economic Review | April 201614

China Economic Review | April 2016 15

Adaptive anachronism

COVER STORY

China Economic Review | April 201616

China’s latest fi ve-year plan for the economy could be its last

COVER STORY

they will have to learn the hard way that

these complex and globally integrated

economies, they can’t be guided by a

government so easily anymore.”

Bits of history, repeatingChina’s first five-year plan in the true

Soviet sense came shortly after the

founding of the PRC. After initial suc-

cess in boosting industrial output, Mao

Zedong almost brought the just-birthed

state to its knees in 1958 with the disas-

trous follow-up of the Great Leap For-

ward resulting in, according to some

estimates, tens of millions of deaths in

an attempt to cram decades’ worth of

industrialization into half of just one.

Despite serious drawbacks, the old

planning apparatus continued to direct

economic activity even after Mao’s

death in 1976, though centralized plan-

ning of resource allocation was drasti-

cally curtailed starting in the mid-1980s,

at least for sectors not considered vital

to continued party control.

It wasn’t until after the troubles

of 1989 and the collapse of the Soviet

Union that five-year plans lost their

old role: In 1993 the party’s Central

Committee ordered officials to “take

markets as the foundation,” and by the

time the 9th FYP rolled around in 1996

the party-state had begun drastically

reconfiguring the purpose and process

of planning.

In place of a static blueprint, FYPs

were recast as an adaptive, continuous

cycle of policy coordination, imple-

mentation, evaluation, and later,

adjustment. The new planning system

helped preserve the central leadership’s

influence over China’s economy and

ensured continued political control

The outline for China’s 13th

five-year plan is not sum-

mer beach reading: The

22,000-character document, which lays

out in the broadest terms how China’s

leaders want the country’s economy to

develop between now and 2020, is the

peak of consensus policymaking for

which Beijing’s mandarins are famous.

And as with many a seemingly bind-

ing document in China, the plan serves

as the opening salvo for the start of the

real negotiations, as lower echelons of

government begin to interpret the latest

round of orders from on high to better

suit an almost endless variety of agendas

at every ministry, regulator, region and

locality.

In the two decades since the party

largely abandoned its old Soviet-style

economic planning system for a more

adaptive model, the central leadership

has managed to broadly bend China’s

legion of competing interests toward

key developmental targets. But as Chi-

na’s economy grows more complex

and difficult to direct, the feasibility of

this generally successful five-year plan

(FYP) system may be coming to an end.

How the party handles that transition

- and the circumstances under which it

occurs - could have a serious impact on

the party’s legitimacy.

“What’s at stake here is this idea that

a national economy can still be guid-

ed by a party center and a strong gov-

ernment in these times of turbulence

and of structural transformation,” said

Sebastian Heilmann, founding direc-

tor of the Mercator Institute for China

Studies and author of multiple research

papers on China’s planning system.

“This is rather shaky, and I think

China Economic Review | April 2016 17

while also decentralizing decision-

making and providing room for market

forces to play a greater role.

Plan as processPreparation for each FYP can begin as

early as two years before publication,

according to an in-depth analysis of

the planning system co-authored by

Heilmann and Oliver Melton, of the US

Department of State.

The party’s Central Committee typi-

cally approves plan guidelines towards

the end of the year before a given plan-

ning period begins, outlining its content

in broad terms. The National Develop-

ment and Reform Commission then

hammers out the details before Chi-

na’s legislators rubber-stamp a broad,

finalized outline in March, during the

annual session of the National People’s

Congress (NPC).

From there, thousands of sub-plans

are issued by lower levels of govern-

ment, working out the concrete details

of how to actually implement the out-

lined policies.

More recent plans have further con-

solidated the changes of the 1990s: The

11th FYP actually changed its title from

“imperative plan” (jihua) to “coordina-

tive plan” (guihua), and divided top

economic targets into two categories:

“indicative” and “binding”. The lat-

ter are viewed as government prom-

ises, and are used to measure cadres’

performance in annual evaluations to

encourage implementation. The 12th

FYP was the first to fully employ the

new target framework, and further

institutionalized the planning process

under the direction of the NDRC.

With so much advance notice and a

preview of its basic content months in

advance, few were surprised by the con-

tent of the 13th FYP when its full text

was published on March 17. But that

doesn’t mean the plan wasn’t important

- or even surprising - in its own right.

Lukewarm receptionWith the debut of the latest FYP, ana-

lysts and economists issued a raft of

notes generally stating a lack of surprise

at the targets announced for the new

FYP; discounting the possibility of an

immediate hard landing; and expressing

unease over the retention of a growth

goal for headline GDP.

Concern was particularly keen

among those whose estimates already

peg China’s growth below 6.5%, the

average annual rate of expansion the

plan calls on the country to maintain

for the next five years.

“It’s a tough one,” said Julian Evans-

Pritchard, China economist with Capi-

tal Economics. “At least on our measure

the economy is already growing below

that level, so there’s a question of what

are they going to do over the next five

years.”

Pritchard-Evans said he expected

authorities would likely fudge the num-

bers rather than deploy another massive

stimulus like that seen in 2009, which

like that one could prove harmful to the

COVER STORY

China Economic Review | April 201618

COVER STORY

economy in the long run by driving up

overcapacity and wasteful spending.

But he added, “you do wonder why

they still see the need to stand by this

target. Obviously the target was set by

the previous administration, but drop-

ping it would’ve been the right thing

to do.”

While the 6.5% growth goal is not

technically a binding target, it is based

on a basic calculation of how much

growth is necessary to meet the party’s

Centenary Goals, which call for ending

absolute poverty and doubling average

disposable income by 2020.

Heilmann noted that while officials

at the NDRC had expressed doubts to

him about the feasibility and cost of the

poverty alleviation goal, Xi’s repeated

emphasis of the goal as a top-level tar-

get meant the government was likely to

spend heavily on it.

He added that this wasn’t the only

policy target requiring headline growth

to remain high. “It’s actually the base-

line—so this must be achieved, oth-

erwise most of the other goals will not

be achievable,” he said. “The signal is

made clear in this plan, again, that even

though 6.5% was not announced as a

‘binding’ target, it is actually the foun-

dation for most of the other efforts.”

On targetsThose efforts are many, but perhaps the

biggest chunk of text in the 13th FYP

goes toward highlighting the impor-

tance of innovation for China’s econ-

omy.

That focus has been visible since the

Central Committee released its guide-

lines last year. Scott Kennedy, direc-

tor of the Project on Chinese Business

and Political Economy at the Center

for Strategic and International Studies,

wrote of the party leadership’s proposal:

“At its heart, this plan is about innova-

tion first and foremost,” with a focus on

addressing legal, financial and institu-

tional obstacles to innovation.

Kennedy noted that the question

of how exactly to measure China’s

progress toward becoming a more

innovative society remained unan-

swered ahead of the outline’s publica-

tion in March.

The final text does place tremendous

emphasis on innovation, particularly

the role of entrepreneurs and individual

researchers, calling for their role in con-

tributing to national innovation to be

strengthened, the benefits they receive

from their work to be greater, and their

involvement in government policymak-

ing expanded.

Heilmann noted that the outline

even grants entrepreneurs a “right to

speak up” on government decisions in

the field of innovation, though he was

skeptical a top-down policy, likely driv-

en by more state-backed investment

programs, would be enough to spur

bottom-up innovation.

For those workers being forced out

of overcapacity sectors but who are less

entrepreneurially inclined, the plan calls

for the provision of vocational educa-

tion free of charge by 2020.

That aligns with the objective of

restructuring China’s economy away

from heavy industry, and like the recent

announcement of a relatively small

RMB100 billion buffer fund for those

let go due to overcapacity cuts, it may

also reflect policymakers’ optimism

about the likely levels of unemployment

resulting from economic transition.

Damien Ma, a fellow at the Paulson

Institute, said that among top policy-

makers, there was “a sincere sense that

they do believe the services sector will

be the savior in absorbing unemploy-

ment.”

Ma said that while some had called

for a greater fiscal deficit to help cush-

ion the blow of shutting down overca-

pacity sectors, belief in the sustainabil-

ity of services sector growth had likely

convinced the center it didn’t need

China Economic Review | April 2016 19

COVER STORY

to dole out large sums of money for

layoffs that were ultimately far small-

er than those made in the late 1990’s

under then-premier Zhu Rongji.

Modesty: The best policy?Yet if services are to provide salva-

tion from rising unemployment, the

party is not anxious to divulge exactly

how. In fact, the 13th FYP doesn’t even

include a section on the role of services

in the economy, in stark contrast to the

emphasis of the 12th FYP.

“I think this is kind of a systematic

blind spot in the plan. I must really say,

it surprises me,” Heilmann said, adding

that based on the lack of detail and a

relatively unambitious target of 65% for

services’ contribution to GDP by 2020,

“the services sector is underpowered in

this plan. No doubt.”

The plan’s latest targets for lower-

ing emissions and pollution relative

to energy consumption are likewise

fairly modest, Ma noted, which was

par for the course thanks to previous

plans’ reduction targets having already

snapped up most of the low-hanging

fruit.

“If you’ve been tracking this for the

last few years, this should not have been

a surprise,” he said, pointing instead to

more ambitious goals for development

of green finance and green technology,

in addition to more integrated planning

on economic growth and the environ-

ment.

“I think that there’s less emphasis on

growth targets and more emphasis on

development in a more holistic sense,

which I find somewhat encouraging

compared to the previous plans,” Ma

said.

Caution breeds dangerWhen it comes to the most urgently

needed economic reforms, though,

the 13th FYP is far less ambitious. The

same relatively smaller cuts to heavy

industry’s workforce that aim to keep

unemployment down keep expenses at

the often state-owned firms employing

them up.

Meanwhile, state-owned firms look

likely to continue receiving state sup-

port even if unprofitable, with policy-

makers encouraging mergers instead of

allowing firms to go out of business.

“From the language of the NPC and

FYP, it seems their policy is to avoid

layoffs and bankruptcies at all costs,”

said Evans-Pritchard. “The prob-

lem with that is it’s sending a message

that they’re not really willing to accept

there’s a certain amount of pain that

comes with this restructuring.”

While he said Capital Economics

didn’t expect policymakers to run out

of ammo to shore up the economy in

the short run, the firm was far less opti-

mistic about China’s prospects beyond

the end of 2016.

“I think the trouble is the economy

still remains on a downward trajectory,”

he said. “Partly it’s structural, but there

is still, I think, the potential for China

to be growing faster than it is at the

moment if they remove some of these

structural barriers.”

While unprofitable state firms could

still be kept alive by rolling over loans

or other similar measures, locking up

resources just to keep them from col-

lapsing would be a serious drag on Chi-

na’s long-run potential growth.

Marie Diron, senior vice-president

for sovereign ratings at Moody’s, said

the firm was paying close attention to

how China planned to balance the three

objectives of supporting growth, push-

ing forward with reform, and main-

taining economic, financial and social

stability—and whether it could.

“In the plan, if we can summarize

it very succinctly, the emphasis is very

much on growth and stability, possibly

at the expense of reforms, or at least the

reforms that could jeopardize its growth

and stability objectives,” Diron said.

From a sovereign risk perspective

that suggested supportive growth policy

in the years ahead, she said, leading to

a further increase in leverage, one of

China Economic Review | April 201620

COVER STORY

the key drivers of risk that had led to

Moody’s to recently downgrade China’s

debt rating to negative.

With great power…Perhaps the most surprising change in

the 13th FYP comes in the final chapter

on implementation, where the lead-

ership role of the party - specifically

the Leading Group for Financial and

Economic Affairs, led by Xi Jinping - is

emphasized.

It’s a substantial change from pre-

vious plans, whose implementation

was overseen chiefly by the National

Development and Reform Commission,

nominally on behalf of the state, rather

than the party.

It’s yet another move that further

centralizes power under Xi—but it also

concentrates still more responsibility

to deliver on the plan’s binding targets,

as well as to ensure the targeted growth

rate on which they depend.

Yet China’s economy may be get-

ting too unruly for even the new FYP

system. Heilmann even went as far

as to suggest the 13th plan might be

China’s last, should target figures’ tra-

jectories begin falling wide enough of

their marks—though the optics of that

transition could be spun as an eco-

nomic triumph if the party proves deft

enough.

“The trick that they could still pull

is to say they [have been] successful in

realizing the decisive role of markets

and competition. Then the five-year

plans are not as necessary anymore,”

he said.

For now, at least, the planning sys-

tem is quite intact, and gearing up for

the issuance of more detailed imple-

mentation plans from countless par-

ty-state organs; the contradictions at

the heart of many policy goals remain

serious, and with so much power now

gathered in his hands, Xi is under pres-

sure to deliver on his policy promises as

well as those of his predecessors.

Whether Xi can deliver 6.5% GDP

growth is far from certain, and whether

he could own up to falling short of that

goal is even less so. As his diminished

counterpart, Premier Li Keqiang, told

reporters at the close of the NPC: “it

would be impossible for me” to say

China might fall short of its growth tar-

get.

Truer words were rarely spoken.

China Economic Review | April 2016 21

China Economic Review | April 201622

China Economic Review | April 2016 23

China Economic Review | April 201624

China Economic Review | April 2016 25

China Economic Review | April 201626

China Economic Review | April 2016 27

China Economic Review | April 201628

2015

China Economic Review | April 2016 29

In March, in the face of protests

from opposition lawmakers,

Hong Kong’s Legislative Coun-

cil approved additional funding of

HK$19.6 billion (US$2.52 billion) for

an already over-budget high-speed rail

link to the mainland cities of Shenzhen

and Guangzhou.

The new funding round pushed

the project’s cost way above an orig-

inal estimated budget of US$8.3 bil-

lion, and some lawmakers and citizen

groups have called for the project to be

scrapped due to the ballooning budget

and possible border control complica-

tions. A document from the Transport

and Housing Bureau also cut forecasts

of the rail’s economic return from 6%

to 4%. But the territory’s government

said in December that abandoning the

project would entail a loss of US$9.7

billion.

That some people in Hong Kong

still want the territory to cut its losses

partly reflects just how deep ambiva-

lence toward greater integration with

the mainland runs. But there may be no

other option.

Since the onset of global financial

crisis in 2007, the Pearl River Delta has

been scrambling to better integrate and

restructure its economy away from

low-end, export-dependent manu-

facturing—with mixed results. The

region’s top-tier cities have leveraged

their administrative advantages to move

toward higher tech and services, but a

lack of regional planning has left other

cities in what is now the world’s largest

urban corridor locked into the old and

Delta forces

increasingly untenable model, fighting

for low-margin scraps and lacking in

skilled human capital.

Meanwhile, the region’s onetime

one-stop global hub for all things

China, Hong Kong, faces a crisis of

identity as competition from mainland

cities in key sectors like logistics and

tech development grows, calling into

question the economic role and politi-

cal autonomy of the special autono-

mous region as it is drawn ever closer

into the mainland’s orbit.

As central and provincial govern-

ment officials deploy all manner of car-

rots and sticks to corral regional actors

toward some form of more sustainable

development, the differing and often

conflicting motivations driving the

megacity’s urban centers may make

Hong Kong’s future increasingly depends on the megacity across the border

ECONOMY

China Economic Review | April 201630

them unruly to move forward on any-

thing but their own terms. But the clock

is already ticking on how long the delta

can hold out.

“There is intense competition from

nearby countries like Thailand, Malay-

sia and Indonesia, which have a similar

industrial structure and export struc-

ture,” said Xu Jiang, associate profes-

sor at the Chinese University of Hong

Kong’s Department of Geography and

Resource Management and president of

the Hong Kong Geographical Society,

whose research focuses on the delta’s

development. “The Pearl River Delta

cannot rely on low-end manufacturing

anymore.”

Victim of successFrom the 1980s to early 2000s, the

Pearl River Delta embraced a low-end,

export-driven manufacturing model of

economic growth facilitated by sup-

portive government policy and a mas-

sive influx of foreign capital.

The risks inherent in that model

became apparent with the onset of the

global financial crisis in 2007, which

served as a wake-up call for govern-

ment officials and business interests in

the region. By 2008, policymakers were

pushing an agenda of economic restruc-

turing, with top-tier cities leading the

way toward high-value manufacturing

and services sectors.

Since the crisis, Guangzhou has

become a services hub for the region,

while Shenzhen, situated across the

border from Hong Kong and long a

dynamo of entrepreneurial ambition,

has developed into the start-up capi-

tal of China’s tech sector. Hong Kong

remains, for now, the region’s financial

lynchpin. But these are exceptions.

By and large, though, the Pearl River

Delta has become a victim of its own

success: Most cities are locked into an

old economic growth model, facing

diminishing returns as their factories

compete for already-slim profit margins

with near-identical competitors next

door.

This lock-in has been fostered by

three decades of devolution in which

economic decision-making power grew

increasingly concentrated at the munic-

ipal level throughout China. Short-term

obsession with the profits closest at

hand continues to be spurred on by

local officials who rely on small factories

for tax revenue and to meet official eco-

nomic growth goals.

But even as officials chase promo-

tions, they, too, can recognize that the

flaws of the old model are glaring: It is

increasingly expensive, produces heavy

pollution, is incredibly inefficient, pro-

vides low differentiation, and lacks the

necessary coordination to allow for

more productive specialization.

Power in politicsThe central government isn’t entirely

powerless in the face of freewheeling

metropolitan economies, though. Since

2000, high-capital projects have become

increasingly important to the Pearl

ECONOMY

China Economic Review | April 2016 31

River delta’s economy relative to

overseas funding, Xu said. She noted

that these often need central govern-

ment approval, putting a fair bit of poli-

cymaking power back in Beijing’s hands.

The central government also retains

control over appointment of leaders in

cities like Shenzhen and approval for

key policy and administrative changes.

Since 2008, Guangdong’s provincial

government has been working with the

central government to use that poli-

cymaking leverage to push forward a

“double shift” in the region’s economy:

1. The delta’s core area shifts away

from low-end, labor-intensive, pol-

luting industries to favor sectors with

higher returns on investment;

2. The core’s labor pool shifts from

migrants to high-value workers.

But the central government has nat-

urally favored top-tier cities of Guang-

dong and Shenzhen where it has more

influence on policymakers’ decisions.

This has resulted in state and foreign

funding being funneled to these “sub-

provincial” level cities as safest options

for all involved.

Roads to the capitalStymied by economics, policymakers

are increasingly trying to tie Pearl River

Delta cities’ transportation systems

together—low-hanging fruit in terms of

regional integration.

“When talking about regional plans,

that’s one of the easier places to start

because in general it’s less controver-

sial,” said Daniel Hedglin, an urban

planner and co-founder of the China

Urban Development Blog.

Hedglin said the large and highly-

concentrated population distributed

among numerous cities – which grew

together as outlying factory zones

pulled them into countryside – make

the delta a natural target for region-

al governance. In lieu of established

regional governance system, infrastruc-

ture can also act as important first step

in building inter-city trust.

Xu noted that if the Pearl River Delta

truly hopes to achieve economic great-

ness, it will need networks both local

and global to get there. “If you look

at world history, all the great cities are

supported by vast transportation arter-

ies connecting their vital commercial

organs with the outside world.” While

she warned that few believe infra-

structure actually guarantees growth,

Xu added that “without infrastructure

you’re definitely a loser.”

But for the only truly cosmopolitan

city in the delta, growing interconnect-

edness with the rest of the region pro-

vokes deep unease.

Hard to portThere may not be anything inherent-

ly malevolent about the Hong Kong-

Guangdong High Speed Rail project.

But while its growing price tag might

be reason enough to complain, the local

backlash goes beyond pure economics.

“I do feel like the more relationships

there are in different areas, the more

that [Hong Kong’s] sense of independ-

ence may be threatened,” said Hedglin.

The fact that the pro-Beijing top

politician in Hong Kong, C.Y. Leung,

has proven to be the least popular chief

executive in the territory’s history is

likely not helping.

The Umbrella Movement of 2014

has been cast by some observers as a

rejection of Leung’s (and by extension,

Beijing’s) “economics only” approach

to political reform. State media have

framed local outrage at denial of full

universal suffrage in favor of an elec-

tion only among Party-approved chief

executive candidates as unnecessarily

politicizing governance.

Yet for all the benefits brought on by

business ties to the rest of the river delta,

Hong Kong’s economic success is like-

wise inextricably tied the foundational

governance feature that most differenti-

ates it from the mainland: Rule of law.

Xiangming Chen, founding dean and

director of the Center for Urban and

Global Studies at Trinity College, said

that while Hong Kong may never again

be the sole gateway to China for the

world, it still has “irreplaceable advan-

tages in terms of financial strengths.”

“Economic autonomy,” Chen said,

“will continue to differentiate it from

any other top-tier mainland city in

terms of being a financial hub.” After

all, for mainland firms serious about

going public, the stock exchange of

choice is still in Hong Kong, not Shang-

hai or Shenzhen.

But that also increases Hong Kong’s

dependence on China’s economy, as

reflected by the March 12 downgrading

ECONOMY

China Economic Review | April 201632

of the territory’s long-term debt and

issuer ratings from “stable” to “nega-

tive” by ratings agency Moody’s. The

firm cited risks to China’s economic

stability and growing political links

weighing on Hong Kong’s institutional

strength as the basis for revising its rat-

ing of the territory’s financial outlook—

which came just three days after the rat-

ings agency downgraded its outlook on

China’s government debt to “negative”.

Yet Hong Kong’s other econom-

ic roles are being usurped as well:

Guangzhou now has its own deepwater

port and a thriving business services

sector, while Shenzhen is becoming a

booming center for tech R&D as well as

home to the mainland’s online services

conglomerates.

And the disappearance of five book-

sellers connected to a Hong Kong pub-

lishing house notorious for putting

out salacious political tell-alls – and

the equally suspicious circumstances

around their reappearance on the main-

land, apparently assisting with a crimi-

nal investigation – beg the question of

how long Hong Kong’s autonomy, and

thus the foundation for its biggest busi-

ness advantages, can really last.

Questions unansweredHowever, as the relationship between

Hong Kong and the rest of the delta

develops, transition is likely unavoid-

able, notes Chen: “No city will monopo-

lize a unique set of functions forever,”

and neither Hong Kong nor its neigh-

bors across the border are any exception.

The provincial government slogan

“teng long huan niao” describes pol-

icymakers’ plans for the delta’s core:

“Loose the birds from their cage and

bring in new ones”.

Old industries are to be pushed to

the less-developed periphery in the

province’s northern and western reach-

es, and in recent years, Chen said, the

center of manufacturing gravity has

indeed shifted across the Xi River to

less-developed cities such as Jiangmen.

Yet when it comes to the region’s

most famous city, Xu said that differing

government objectives will remain a key

challenge to regional integration of the

Pearl River Delta: Where Guangdong

still prioritizes economic growth above

all, Hong Kong’s population is increas-

ingly concerned with environmental

and social issues.

ECONOMY

China Economic Review | April 2016 33

2016

2015 10

8

6

4

2

0

-2

-4

2009

3.1 3.1

-3.4

3.1

5.44.2

3.4 3.63.3 3.4

1.7 1.2 1.1 1.8 2.0 2.2

5.2

7.5%

6.3

5.0 4.64.0

4.5

2010 2011 2012 2013 2014 2015 201600999

3 4

3.11.7 1.2 1.1 1.8 2.0 2.2

2010020100 20112011 20122012 20132013 20142014 20152015 2011620116

3..1 3 1

55.45.44.24.2

3.43.4 3 63.63.33.3 3 43.4

5.26.3

5.0 4.64.0

4.5

3 13.1

China Economic Review | April 201634

China Economic Review | April 2016 35

China’s economy grew at the

slowest rate in a quarter-cen-

tury last year by official meas-

ure, but that economic gloom couldn’t

dampen an unqualified box-office

boom: Annual ticket sales revenue rose

48.7% at mainland theaters in 2015 to a

record total of US$6.78 billion (RMB44

billion).

While 2014 saw China’s film indus-

try grow more industrial as moviegoers’

tastes filtered back to production studi-

os through an ever-expanding phalanx

of theaters, 2015 saw it double down on

a drive toward consumer-facing cine-

ma. Where ticket sales were once all the

feedback studios needed, online lit and

streaming series now provide edgier

film fodder. That has kicked efforts to

capitalize on intellectual property into

overdrive—one major consequence of

which is that Chinese firms are sud-

denly as eager as Hollywood studios to

exercise their copyrights.

“Copyright is now becoming a sword

in the hands of Chinese rights owners,”

said Mathew Alderson, partner at Harris

& Moure, PLLC and frequent contribu-

tor on Chinese copyright law for the

China Law Blog. “Chinese companies

are not going to spend a lot of money

acquiring rights from foreign sources

only to let Chinese pirates in the next

province free-ride on the investment.”

Offshore, but close to homeThat interest in IP is also reflected in

Chinese films’ growing dominance of

the domestic box office: Only three of

the top ten films from 2015 came from

US studios, down from five in 2014.

And while the top spot did go to

Box offi ce boom

Universal Pictures’ “Furious 7” with a

box-office take of US$390.9 million,

the Hong Kong-China co-production

“Monster Hunt” was only about US$9

million behind. Figures from the State

Administration of Press, Publication,

Radio, Film and Television (SARFT)

likewise showed Hollywood movies’

share of annual mainland box-office

revenue fell to 38.4% in 2015, down

from 45.5% the year prior.

Movies l ike “Monster Hunt”

embody two trends highlighted by

Michael Keane, professor of Chinese

media at Curtin University: The grow-

ing popularity of action comedies that

appeal to younger audiences and con-

tinued collaborations between Hong

Kong and China. Such co-productions

allow mainland investors to funnel

funds to Hong Kong studios which can

take advantage of less stringent content

controls and local directors willing to

work on movies that could see a main-

land release, even if they couldn’t get

made there.

The record revenue generated by

“Monster Hunt” has since been thrown

into question, with accusations of

late-run box-office inflation eventu-

ally substantiated by a mea culpa from

the film’s distributor. But much of that

revenue was real, and the potential of

action-comedy co-productions was

demonstrated again with even greater

gusto by the success of “The Mermaid”

in 2016.

The co-produced action-comedy

flick recently became the first in main-

2015: The year China’s fi lm industry doubled down on IP

ECONOMY

China Economic Review | April 201636

land box-office history to pass the

RMB3 billion mark, setting an all-time

record—dethroning “Furious 7” and

even doing decent business during a

limited release in the States, much to

Hollywood’s chagrin.

Clampdown coming?The allegations of box office fraud that

dogged “Monster Hunt” appear to have

prompted regulators to enact new ticket

sales rules and even agree to let Hol-

lywood studios audit Chinese box office

receipts, according to The Hollywood

Reporter. The draft text for China’s new

Film Industry Promotion Law, made

public in November, would also pro-

vide more box office regulation, but it

doesn’t stop there.

While it fails to open up film pro-

duction and distribution to foreign

firms or lift the onerous quota system

for foreign films, Alderson noted that

the draft law “would definitely stream-

line the official co-production process

for foreign producers.” He added the

draft law also gave express official recog-

nition of the need for improvements in

the system of film finance and the need

for tax incentives for local producers.

Barring major changes before it’s

passed – always a possibility – the new

law would encourage financial institu-

tions to provide financing and other

services to facilitate the growth of Chi-

na’s film industry, including recom-

mending pledge services for film-related

intellectual property.

Such high-level government recogni-

tion of intellectual property’s impor-

tance reflects IP’s newly elevated status

in China. The recently-launched indus-

try news site China Film Insider even

deemed it “the industry buzzword of

2015.” With good reason.

Ecosystems evolvingAll the buzz makes sense in light of the

fact that some of last year’s top per-

formers at the box office had roots in

shows or sketches that streamed exclu-

sively online, a development Alderson

said was reflective of deeper changes in

audience interest and industry funding.

“We are seeing domestic motion pic-

tures emerging rapidly out of so-called

online literature,” Alderson said, refer-

ring to China’s vibrant online commu-

nities focused on writing and video pro-

duction. Indeed, China’s submission to

the 2016 Academy Awards, “Go Away,

Mr. Tumor”, originated as an online

comic strip.

The film was also co-produced by

Wanda Pictures, a unit of mainland

conglomerate Wanda Group. While the

firm’s recent acquisition of Legendary

Entertainment made waves, Wanda

has also invested in the Beijing comedy

theater Happy Donut as an incubator

which has since become a film produc-

tion unit that turns out low-budget

comedies.

Along with Tencent and Alibaba,

Wanda is shooting to become a con-

tent production house that sidesteps

the old model and responds more to

consumer trends. While Keane warned

that further restrictions on online

content could curtail up-and-coming

online sources of new IP, it was too

soon to say what approach regulators

would take.

He added that it was easy to imag-

ine China’s streaming sites (LeTV and

Youku Tudou) and content producers

(Tencent, Alibaba, Wanda) ultimately

converging on an industry model in

which the respective content ecosystems

of major players vie for user eyeballs—

as is already the case in the US with

Netflix and Amazon.

Even then it’s possible that crowd-

funding could disrupt the film indus-

try’s current trajectory, as it has once

already: “Monkey King: Hero is Back”

wouldn’t have made it through the final

stages of production without a vital

boost via crowdfunding, much of it

from parents who pitched in to get their

children’s names in the movie’s cred-

its. After flirting with nonexistence, the

animated feature went on to snag the

tenth-place spot on last year’s list of top

box-office hits in China.

“Crowdfunding is the question on

people’s lips,” Keane said. The model

remains largely unregulated in China –

always a potential pitfall for any media

enterprise. But he said it real, untapped

potential that could ruffle not a few

industry feathers. “If it can be better

regulated,” he said, “it could have a

major impact.”

That is as big an “if” as one is like to

encounter in the mainland film indus-

try. But if funding follows suit with Chi-

nese cinema’s increasingly consumer-

facing content, it may prove not a ques-

tion of “if”, but “when”.

ECONOMY

China Economic Review | April 2016 37

China Economic Review | April 201638

14:00~17:002015 9

SPASPA

18:00~19:00 ( )

06:30~08:30 ( )1,500

09:00~12:00760 700

LED

12:00~14:00 ( )

14:00~17:0010

15:30~16:00logo

19:00~21:00 ( )

08:00~09:00 ( )

10:00

82,000 ICCA)

5TripAdvisor

403

(ICCA)10,000

9,0002000

122 3100070571 879908880571 [email protected] www.naradahz.com

The New Landmark of Yellow Dragon Business Area

on on

122 SHUGUANG ROAD, HANGZHOU, CHINA P.C. 310007122

Facing to the Precious Stone Hill beside the West Lake, Zhejiang Narada Grand Hotel is adjacent to the

Zhejiang World Trade International Exhibition Center in which a large “marketing conference” of more than

2,000 people could be held. And it is also a short walk from the Dragon Sports Center – a place for sporting

event or concert. The hotel that possesses 403 deluxe rooms blends perfectly modern style with beautiful

natural scenery. Looking out from window, Precious Stone Hill Floating in Rosy Cloud and Yellow Dragon

Cave Dressed in Green are in sight.

2000

403

Deluxe room priced at RMB 788 net per night (including 2 buffet breakfast in Window Pavilion )

For information or booking, please contact by phone at +86 (0571) 87950193 or 87990888 to 57.

788 ( )

+86 (0571) 87950193 87990888 57

China Economic Review | April 201640

2012-2018

3

2

1

02012

0.30.4

0.60.9

1.2

1.5

1.9

2013 2014 2015 2016e 2017e 2018e

%

%

2.5%

56.4% 54.2% 45.7% 38.5% 28.4% 27.4% 28.2%

3.7% 5.4% 8.6% 11.7% 15.1% 19.4%

China Economic Review | April 2016 41

VS

China Economic Review | April 201642

China Economic Review | April 2016 43

China Economic Review | April 201644

China Economic Review | April 2016 45

China Economic Review | April 201646

China Economic Review | April 2016 47

TAKING TAKEOUT INTO THE 21ST CENTURYBy 2004, the Internet had already

revolutionized the way consumers bought

music, asked questions, and communicated

with one another. But ordering food was

another story: most customers still used paper

menus. And if restaurants offered online

ordering, their sites were often clunky and

inconsistent.

Hungry and overworked one evening, then-

software engineer Matt Maloney, ’10, and a

colleague dreamed up the idea: an easy-to-use

online ordering site with abundant nearby

options to choose from. They got started right

away, collecting menus from local restaurants

and trying to sell the idea to them in a way that

worked for both parties.

But how far could he take this promising

hypothesis? “We were solving a problem, but

we weren’t building a business.”

Using the analytical frameworks of The Chicago

Approach, Maloney and his business partner

developed a two-sided data model to both

persuade skeptical restaurant owners to buy in

and encourage consumers to place their orders

on their laptops and phones instead of the old-

fashioned way. The idea, dubbed GrubHub, won

first place in Chicago Booth’s Edward L. Kaplan,

’71, New Venture Challenge in 2006. Less than

a decade later, Maloney, as CEO, led GrubHub

through an IPO.

The company now represents 35,000 takeout

restaurants in more than 900 US cities and

London, and is on track to report a 2015 net

revenue well over $350 million—success that

Maloney can trace back to the New Venture

Challenge and The Chicago Approach.

“Chicago Booth showed me how to

build a business.”

ADVERTISEMENT

“WE WERE SOLVING A PROBLEM,

BUT WE WEREN’T BUILDING A BUSINESS.

CHICAGO BOOTH SHOWED ME HOW

TO BUILD A BUSINESS.” Matt Maloney, ’10, CEO, GrubHub Inc.

Since 1898, we have produced ideas and

leaders that shape the world of business.

With campuses in Chicago, London, and

Hong Kong, Chicago Booth faculty, alumni,

and students continue to be key influencers

and innovators in the global marketplace.

We are the first and only business school

with permanent campuses on these three

continents.

Chicago Booth is integral in building the next

generation of business leaders—no matter

the stage of their careers. We offer one MBA

with four flexible formats: Full-Time MBA,

Evening MBA, Weekend MBA, and Executive

MBA, as well as custom Executive Education

Programs to help leaders stay ahead of the

ever-evolving business landscape.

Students from more than 50 countries come

to learn from our award-winning faculty

and engage with more than 49,000 alumni

worldwide in every industry. Our

discipline-based approach to business

education transforms our students into

confident, effective, respected business

leaders prepared to face the toughest

challenges.

CHICAGO APPROACH, GLOBAL PRESENCE

ChicagoBooth.edu/impact

MAKE THE CHICAGO APPROACH YOUR OWN.

CHICAGO

HONG KONG

LONDON

THE CHICAGO APPROACH™

IS GIVING RISE TO LEADERS WITH

ENDURING IMPACT IN THE WORLD.

ADVERTISEMENT

BUSINESS EDUCATION FOCUS

Melding two schools of thought

MBA program offers students

global experiences through

classes in Shanghai and

Oslo.

Since its establishment in 1996, the

BI-Fudan MBA Program, organized by

Fudan University’s School of Manage-

ment and the BI Norwegian Business

School, has cultivated more than 2,000

Chinese and foreign professionals.

This year, the program celebrates its

20th anniversary in China.

“During the past 20 years, our stu-

dents’ aspirations have been dynamic

and in parallel with global economic

developments,” said Benedicte Brogger,

associate dean of the BI-Fudan MBA

Program.

“Today, our most popular electives

are courses that teach our MBA stu-

dents how to work with ideas, wealth

management and innovation.”

The part-time program, which lasts

two years, has most of its classes taught

in Shanghai, though part of the pro-

gram is also taught in Norway. The pro-

gram also focuses on offering students a

more international and innovative way

of thinking.

The program was ranked sixth by the

Financial Times among the world’s top

part-time MBA programs.

The best of both

One of the goals for the English-taught

program is to teach students about

capitalizing on different business cul-

tures and making their own competitive

advantages.

The program invites both interna-

tional and Fudan professors to share

their expertise, while students share

their experiences with their peers to

learn from each other.

The administrators of the program

spend a great deal of time planning the

classes because they are combining a

wide breadth of experiences from vari-

ous industries and disciplines.

According to a survey by the pro-

gram’s administration, the program’s

combination of Chinese and Nordic

business cultures is greatly valued by the

students.

The program is the most com-

prehensive academic collaboration

between Norway and China and serves

as an important bridge between the two

countries. For over 20 years, the pro-

gram has helped MBA students become

successful in their international careers.

Improving capabilities

Over 90 percent of BI-Fudan MBA

students work for large multination-

al businesses, and many Fortune 500

companies have sent employees to this

program.

Three years after graduation, stu-

dents see, on average, an 83-percent

salary increase.

They come from a variety of indus-

tries and disciplines, but those from the

healthcare, IT and the automotive sec-

tors are highly represented.

“The students struggle with some

of the same problems. Working in a

2000professionals

have graduated from the BI-Fudan MBA Program

China Economic Review | April 201650

BUSINESS EDUCATION FOCUS

multinational company, and exceeding

their international managers’ expecta-

tions by leading a group of people from

various nations is challenging,” said Xu

Huizhong, executive director of the BI-

Fudan MBA Program.

“In our program they come together

and share their experiences and solve

problems they meet together.”

When asked why they chose to

attend the program, 93.7 percent of

the students in this year’s class said

“improving management capabilities”

is their top priority.

“This program is about acquiring

the right business skills, collaborating in

groups and improving our knowledge,”

said a student from the program.

“It also gives us friends for life. It’s

not that the network is not important,

it’s just that sharing your experience

with peers and learning from each other

is the best way to make friends for life.”

Truly international

It is not just the location of the class-

rooms that make for an invaluable

international experience. It is also the

program’s mix of faculty.

More than 75 percent of the faculty

comes from European countries such as

Spain, Germany, the Netherlands and

Norway.

Both schools are committed to allo-

cating the best professors for the pro-

gram. Most of the Fudan and BI profes-

sors have been teaching in the program

for more than 10 years.

Active alumni network

The program has its own alumni organ-

ization called Join & Share, which cel-

ebrated its 10th anniversary last year.

It provides the alumni with both

social and academic events, and

includes several different clubs and sub-

groups based on the students’ interests.

There are over 2,000 alumni from the

MBA program, many of whom have

gone on to top business careers.

One of the most active groups is

the IT-club, which organizes meetings

about information technology. More

relaxing, and certainly more social, is

the wine club. Students can join and

share their love of French, Italian or

even the increasingly famous Shandong

wine.

Entrepreneurial spirit

The Nordic Hub Partnership, BIFu-

dan MBA’s partnership program with

Nordic companies in Shanghai, seeks to

strengthen the interaction among stu-

dents, businesses and the program’s fac-

ulty. Most of the students seek to boost

their careers within the companies they

currently work for. Through the entre-

preneurial network, students interested

in startups can find a network of like-

minded individuals.

Moving ahead

The strong relationship between Fudan

University School of Management and

the BI Norwegian Business School will

continue to develop as they work to

educate the top Chinese and foreign

business professionals.

The need for such education will

increase as China’s economy continues

to rely more and more on innovative

companies with new technologies and

challenges.

The need for business people with

an international capability to lead and

manage global teams from all over

the world will grow stronger as more

and more Chinese companies venture

abroad.

90Percent

of BI-Fudan MBA students work for large multinationals

China Economic Review | April 2016 51

BUSINESS EDUCATION FOCUS

The relevance of giving multidisciplinary and practical tools

Entrepreneurship and Leadership Trends at EU

Entrepreneurship & EU

With the business paradigm shifting

due to technological advances, entre-

preneurship is becoming a widespread

necessity. Individuals, especially the

young, are presented with opportu-

nities, and as such, there is a call for

additional awareness and training.

According to the International Labour

Organization (ILO), in order to meet

the demands of the generation joining

the labor market in upcoming years,

there is a need to create more than 300

million new jobs by 2020. The crea-

tion of jobs that contribute to sustain-

able and inclusive growth are of utmost

importance. Analysts also believe that

growth in the EU region relies heavily

on entrepreneurship and new venture

creation.

Instigating and fostering an entre-

preneurial spirit is an essential goal at

EU Business School. In order to catalyze

economic and entrepreneurial activ-

ity, current and future students need

to be trained and prepared. At EU, we

provide an environment and a focus to

cultivate both entrepreneurship and the

spirit that goes with it.

Candidates for the EU Entrepre-

neurship MBA course are given practi-

cal tools to help them create their own

businesses. Professors have a broad

range of experience to help entre-

preneurs with topics that range from

R&D and New Product Development

to human resources and leadership.

EU helps students identify business

opportunities and write effective busi-

ness plans, and provides them with the

know-how to develop new products.

This enables students to understand the

necessary elements of getting something

off the ground.

Focus is not limited to the specific

Entrepreneurship and New Venture

Creation courses that are part of the

EU MBA in Entrepreneurship program;

other options which help students to

broaden their knowledge and give them

a good platform to start their own busi-

ness include Innovation and Leader-

ship, and Technology and Change

Management. We believe in looking at

the bigger picture, which is an integral

factor to success in business.

Sharing the Multidisciplinary

Approach

Cross-discipline support for entrepre-

neurship and intrapreneurship is essen-

tial. Many large companies implement

intrapreneurial activities by divesting

authority down the organization and

initiating small projects with shorter life

cycles. Young people new to the work-

place need, therefore, to have a wider

understanding of how a business works

and know-how to manage the risk asso-

ciated with this. Students leaving EU

with an MBA will have the academic

background – and more important-

China Economic Review | April 201652

BUSINESS EDUCATION FOCUS

ly, will have developed the pragmatic

approach – necessary to deal with top-

ics related to entrepreneurship and an

understanding of how intrapreneurship

will work.

New Media & SMEs

The Internet has changed the rules of

the game. New technologies associ-

ated with the Internet are revolution-