Central Florida Community Action Agency, Inc. - cfcaa.org Audited Financial Statements.pdf ·...

25

Central Florida Community Action Agency, Inc. FINANCIAL STATEMENTS September 30, 2016

-

Upload

nguyenthien -

Category

Documents

-

view

215 -

download

2

Transcript of Central Florida Community Action Agency, Inc. - cfcaa.org Audited Financial Statements.pdf ·...

Central Florida Community Action Agency, Inc.

FINANCIAL STATEMENTS

September 30, 2016

Central Florida Community Action Agency, Inc. Table of Contents

September 30, 2016

REPORT Independent Auditors’ Report 1

FINANCIAL STATEMENTS Statement of Financial Position 3 Statement of Activities 4

Statement of Cash Flows 5

Notes to Financial Statements 6 Schedule of Expenditures of Federal Awards 13 Notes to Schedule of Expenditures of Federal Awards 14 Independent Auditors’ Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 16 Independent Auditors’ Report on Compliance for Each Major Program and On Internal Control Over Compliance Required by the Uniform Guidance 18 Schedule of Findings and Questioned Costs 20 Summary Schedule of Prior Audit Findings 22 Corrective Action Plan 23

INDEPENDENT AUDITORS’ REPORT

Board of Directors Central Florida Community Action Agency, Inc. Gainesville, Florida

Report on the Financial Statements

We have audited the accompanying financial statements of Central Florida Community Action Agency, Inc. (a nonprofit organization) (the "Agency"), which comprise the statement of financial position as of September 30, 2016, and the related statement of activities and cash flows for the year then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the Auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the Agency’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Agency’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

‐ 2 ‐

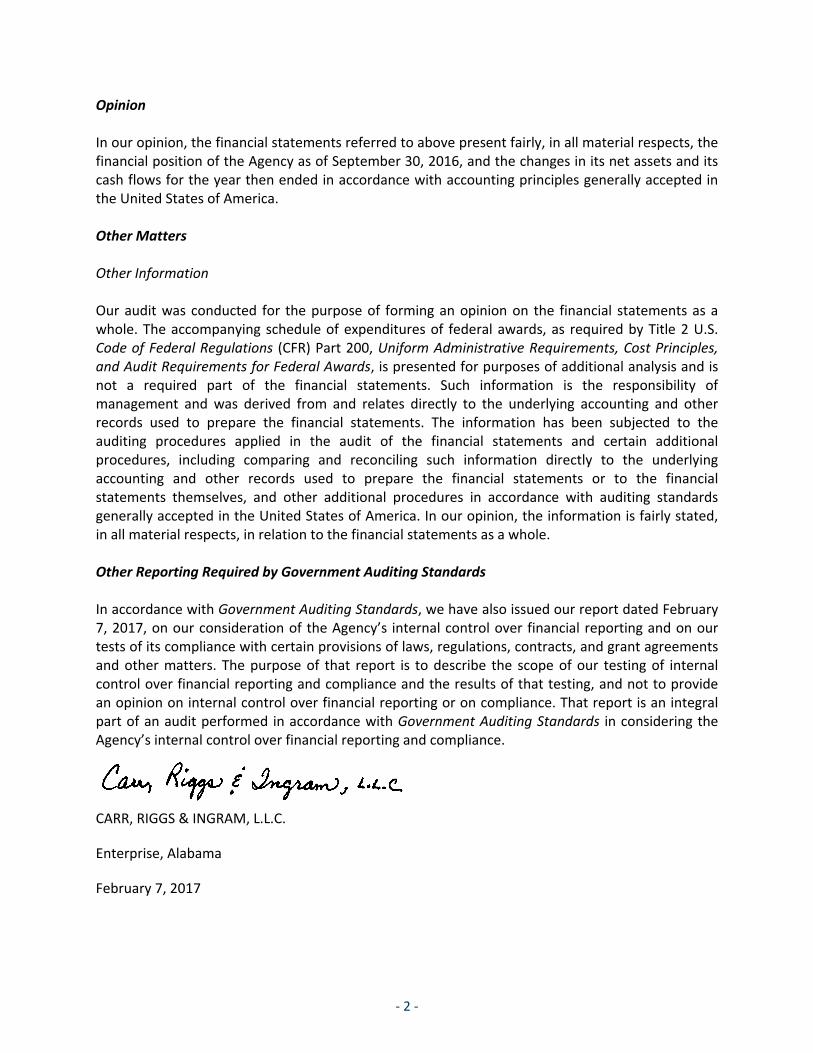

Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Agency as of September 30, 2016, and the changes in its net assets and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Other Matters Other Information Our audit was conducted for the purpose of forming an opinion on the financial statements as a whole. The accompanying schedule of expenditures of federal awards, as required by Title 2 U.S. Code of Federal Regulations (CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, is presented for purposes of additional analysis and is not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated, in all material respects, in relation to the financial statements as a whole. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated February 7, 2017, on our consideration of the Agency’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Agency’s internal control over financial reporting and compliance.

CARR, RIGGS & INGRAM, L.L.C.

Enterprise, Alabama

February 7, 2017

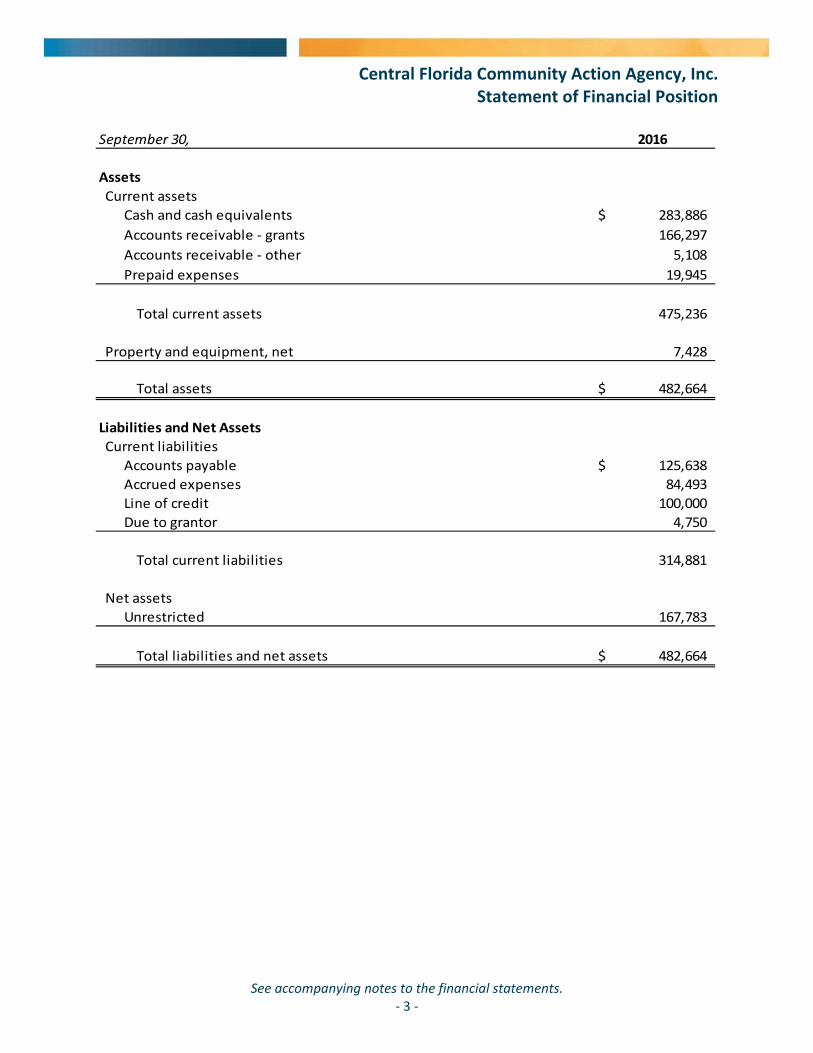

Central Florida Community Action Agency, Inc. Statement of Financial Position

See accompanying notes to the financial statements. ‐ 3 ‐

September 30, 2016

Assets

Current assets

Cash and cash equivalents 283,886$

Accounts receivable ‐ grants 166,297

Accounts receivable ‐ other 5,108

Prepaid expenses 19,945

Total current assets 475,236

Property and equipment, net 7,428

Total assets 482,664$

Liabilities and Net Assets

Current liabilities

Accounts payable 125,638$

Accrued expenses 84,493

Line of credit 100,000

Due to grantor 4,750

Total current liabilities 314,881

Net assets

Unrestricted 167,783

Total liabilities and net assets 482,664$

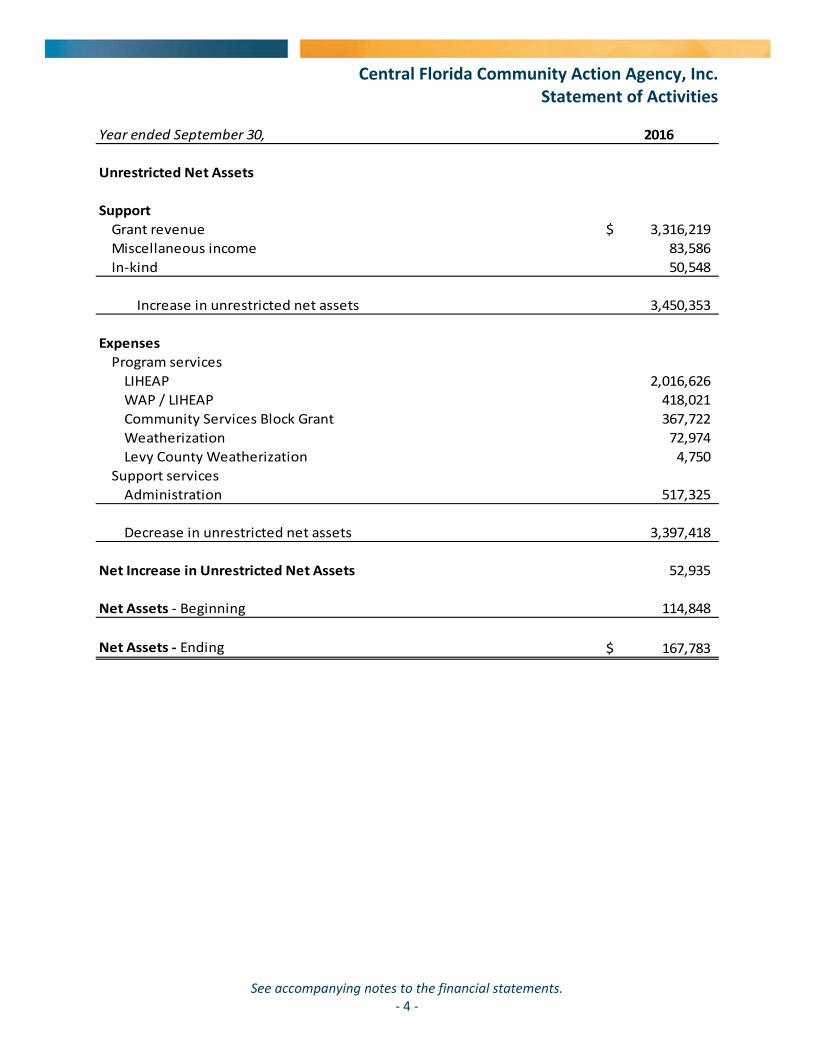

Central Florida Community Action Agency, Inc. Statement of Activities

See accompanying notes to the financial statements. ‐ 4 ‐

Year ended September 30, 2016

Unrestricted Net Assets

Support

Grant revenue 3,316,219$

Miscellaneous income 83,586

In‐kind 50,548

Increase in unrestricted net assets 3,450,353

Expenses

Program services

LIHEAP 2,016,626

WAP / LIHEAP 418,021

Community Services Block Grant 367,722

Weatherization 72,974

Levy County Weatherization 4,750

Support services

Administration 517,325

Decrease in unrestricted net assets 3,397,418

Net Increase in Unrestricted Net Assets 52,935

Net Assets ‐ Beginning 114,848

Net Assets ‐ Ending 167,783$

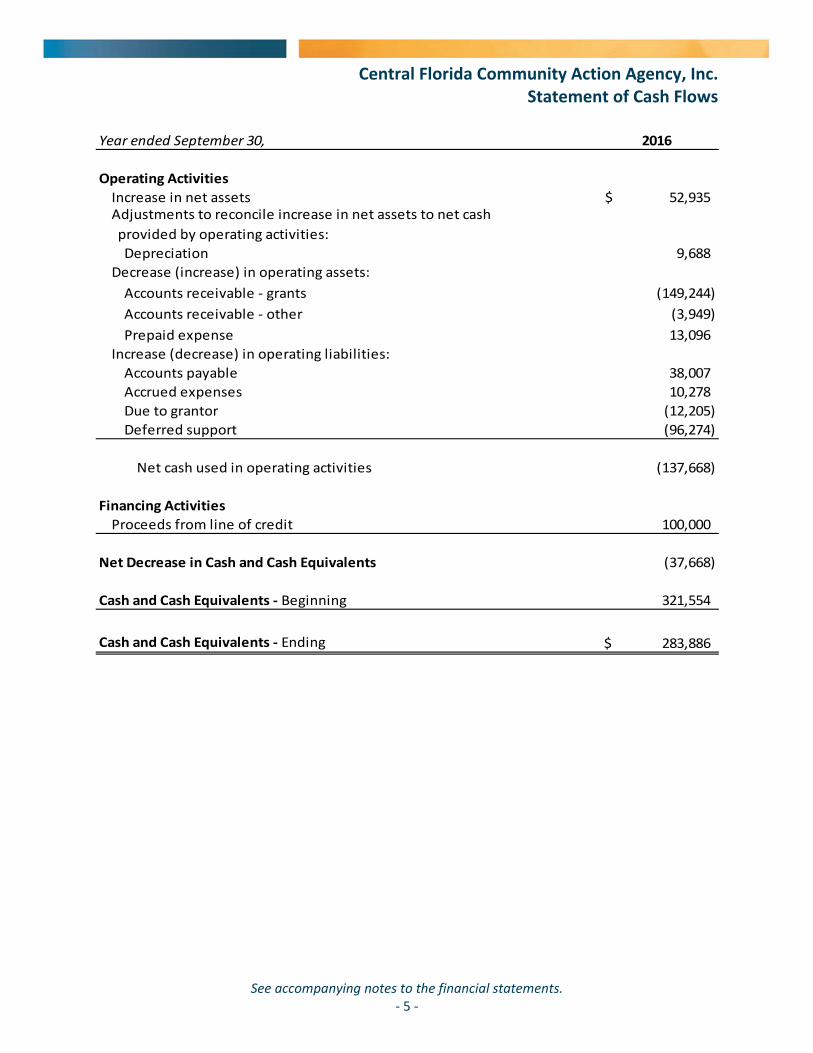

Central Florida Community Action Agency, Inc. Statement of Cash Flows

See accompanying notes to the financial statements. ‐ 5 ‐

Year ended September 30, 2016

Operating Activities

Increase in net assets 52,935$

Depreciation 9,688

Decrease (increase) in operating assets:

Accounts receivable ‐ grants (149,244)

Accounts receivable ‐ other (3,949)

Prepaid expense 13,096

Increase (decrease) in operating liabilities:

Accounts payable 38,007

Accrued expenses 10,278

Due to grantor (12,205)

Deferred support (96,274)

Net cash used in operating activities (137,668)

Financing Activities

Proceeds from line of credit 100,000

Net Decrease in Cash and Cash Equivalents (37,668)

Cash and Cash Equivalents ‐ Beginning 321,554

Cash and Cash Equivalents ‐ Ending 283,886$

Adjustments to reconcile increase in net assets to net cash

provided by operating activities:

Central Florida Community Action Agency, Inc. Notes to Financial Statements

‐ 6 ‐

NOTE 1 ‐ SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Organization Central Florida Community Action Agency, Inc. (the “Agency”) is a non‐profit agency engaged in the administration of federal, state, and local grants intended to aid in the reduction of the effects of poverty on the economically disadvantaged in Alachua, Levy, and Marion counties located in the State of Florida. The Agency is organized on a non‐stock basis and is dependent on contributions and grants as its sources of funds. Basis of Reporting The financial statements of the Agency are prepared using the accrual basis of accounting. With this measurement focus, all assets and all liabilities associated with the operation of the Agency’s funds are included on the statement of financial position. The statement of activities presents increases (e.g., revenues and support) and decreases (e.g., expenses) in the net total assets. Generally grant revenues are earned, becoming unrestricted, as qualified expenses are made and performance occurs. The Agency reports deferred revenue, if applicable, on its statement of financial position. Deferred revenues arise when resources generated by exchange transactions are received by the Agency before it has a legal claim to them, as when grant monies are received prior to the incurrence of qualifying expenditures. In subsequent periods, when revenue recognition criteria are met, or when the Agency has a legal claim to the resources, the liability for deferred revenue is removed from the statement of financial position and revenue is recognized. Financial Statement Presentation The Agency follows FASB ASC Topic 958, Not‐for‐Profit Entities. Under FASB ASC Topic 958, the Agency is required to report information regarding its financial position and activities according to three classes of net assets (unrestricted net assets, temporarily restricted net assets, and permanently restricted net assets) based upon the existence or absence of donor‐imposed restrictions. All assets and all liabilities associated with the operations of the Agency are included on the statement of financial position. The direct costs of providing the various programs and other activities have been summarized by program in the statement of activities. The cost of administering the various programs has been combined and reported as a separate line item in the statement of activities. Income Taxes The Agency has been granted an exemption from income taxes under Internal Revenue Code Section 501(c)(3) as a non‐profit corporation. The Agency applies the provisions of FASB ASC Topic 740 Income Taxes. This topic requires, among other things, the Agency to assess uncertain tax positions and the likelihood that such positions will be upheld by applicable taxing authorities. For

Central Florida Community Action Agency, Inc. Notes to Financial Statements

‐ 7 ‐

NOTE 1 ‐ SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) the purposes of taxation, management has determined that the Agency’s tax‐exempt status is not in jeopardy at September 30, 2016. As such, a provision for income taxes has not been provided. The Agency believes that it has appropriate support for the income tax positions taken and to be taken on its tax returns and that its accruals for tax liabilities are adequate for all open tax years (after 2012 for federal) based on an assessment of many factors including experience and interpretations of tax laws applied to the facts of each matter. The Agency has concluded that there are no significant uncertain tax positions requiring disclosure, and there are no material amounts of unrecognized tax benefits. Cash and Cash Equivalents For purposes of the statement of cash flows, the Agency considers all unrestricted highly liquid investments with an initial maturity of three months or less to be cash equivalents. Advertising Costs Advertising costs are expensed as incurred. Amounts are not considered material to the financial statements. Property and Equipment It is the Agency’s policy to capitalize fixed assets with an initial acquisition price in excess of $5,000. Lesser amounts are expensed as incurred. Purchased fixed assets are capitalized at cost. Donations of fixed assets are recorded as contributions at their estimated fair value. Fixed assets acquired with grant funds are capitalized and a corresponding contribution is recognized. Such items acquired under grants from federal and state sources are considered to be owned by the Agency while used in the programs for which they are purchased or in programs authorized in the future. However, the funding source has a reversionary interest in the property. The historical cost and book value of assets in which grantors hold a reversionary interest was $148,879 and $5,482 at September 30, 2016. Fixed assets purchased or donated are depreciated based on estimated useful lives using the straight‐line method as follows: Buildings 39 Years Office furniture and equipment 5‐7 Years Recognition of Grantor/Donor Restrictions Support that is restricted by the grantor/donor is reported as an increase in unrestricted net assets if the restriction expires in the reporting period in which the support is recognized. All other grantor/donor‐restricted support is reported as an increase in temporarily or permanently restricted net assets, depending on the nature of the restriction. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets.

Central Florida Community Action Agency, Inc. Notes to Financial Statements

‐ 8 ‐

NOTE 1 ‐ SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued) Management Estimates and Assumptions The preparation of financial statements in conformity with generally accepted accounting principles (GAAP) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates. Grants Most of the Agency’s revenues are in the form of grants from federal and state sources. All grants received are renewable on an annual basis and the Agency is dependent on these grants for continued activity. The Agency’s ability to continue operations if the grant programs were lost or canceled are unknown. Economic Dependency – Grants Approximately 97% of the entity’s grant revenues were provided by the U.S. Department of Health and Human Services for fiscal year 2016. Net Assets The Agency’s net assets are classified as follows:

Unrestricted – These are net assets that are not subject to donor‐imposed stipulations. Temporarily Restricted – These are net assets that are subject to donor‐imposed stipulations that may or will be met, either by actions of the Agency, and/or the passage of time. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the statement of activities as net assets released from restrictions. The Agency had no temporarily restricted net assets as of September 30, 2016 and 2015. Permanently Restricted – These are net assets that are required to be maintained in perpetuity with only the income to be used for the Agency’s activities due to donor‐imposed restrictions. The Agency had no permanently restricted net assets as of September 30, 2016 and 2015.

When an expense is incurred that can be paid using the resources above, the Agency’s policy is to first apply the expense towards restricted resources, and then towards unrestricted resources. Subsequent Events The Agency has evaluated subsequent events through the date of issuance of these financial statements and has determined that no events occurring subsequent to year end warranted disclosure.

Central Florida Community Action Agency, Inc. Notes to Financial Statements

‐ 9 ‐

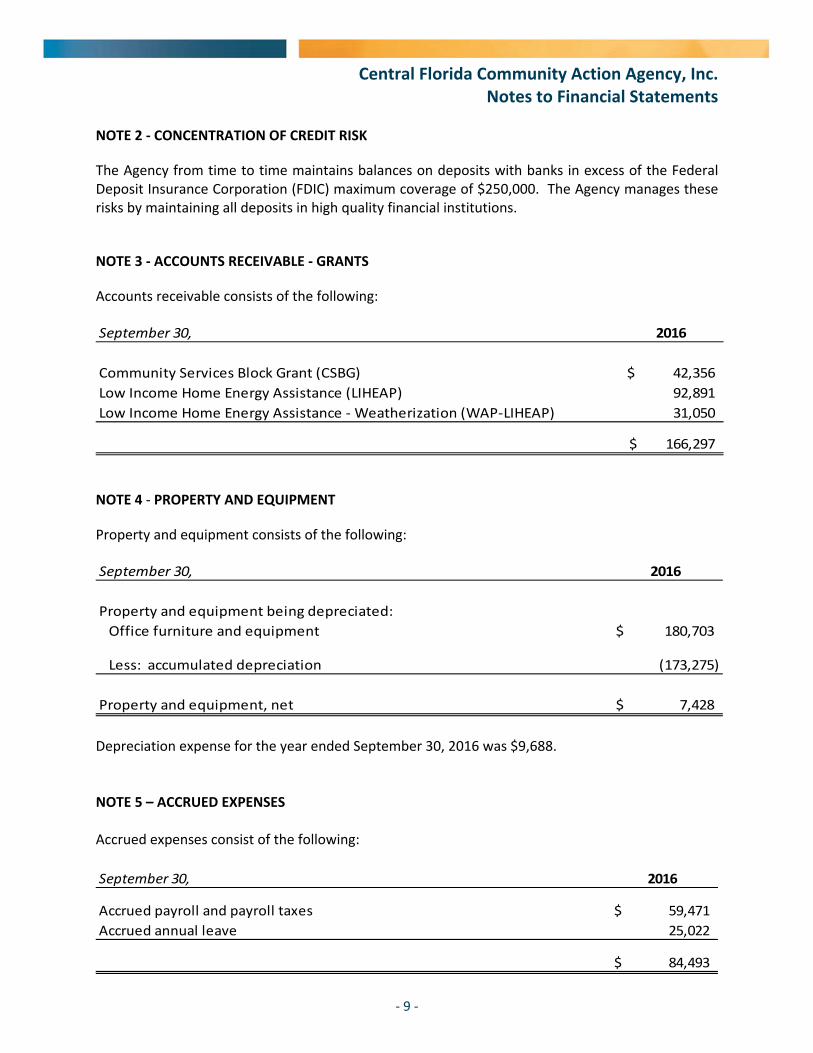

NOTE 2 ‐ CONCENTRATION OF CREDIT RISK

The Agency from time to time maintains balances on deposits with banks in excess of the Federal Deposit Insurance Corporation (FDIC) maximum coverage of $250,000. The Agency manages these risks by maintaining all deposits in high quality financial institutions.

NOTE 3 ‐ ACCOUNTS RECEIVABLE ‐ GRANTS

Accounts receivable consists of the following:

September 30, 2016

Community Services Block Grant (CSBG) 42,356$

Low Income Home Energy Assistance (LIHEAP) 92,891

Low Income Home Energy Assistance ‐ Weatherization (WAP‐LIHEAP) 31,050

166,297$

NOTE 4 ‐ PROPERTY AND EQUIPMENT

Property and equipment consists of the following:

September 30, 2016

Property and equipment being depreciated:

Office furniture and equipment 180,703$

Less: accumulated depreciation (173,275)

Property and equipment, net 7,428$

Depreciation expense for the year ended September 30, 2016 was $9,688. NOTE 5 – ACCRUED EXPENSES Accrued expenses consist of the following:

September 30, 2016

Accrued payroll and payroll taxes 59,471$

Accrued annual leave 25,022

84,493$

Central Florida Community Action Agency, Inc. Notes to Financial Statements

‐ 10 ‐

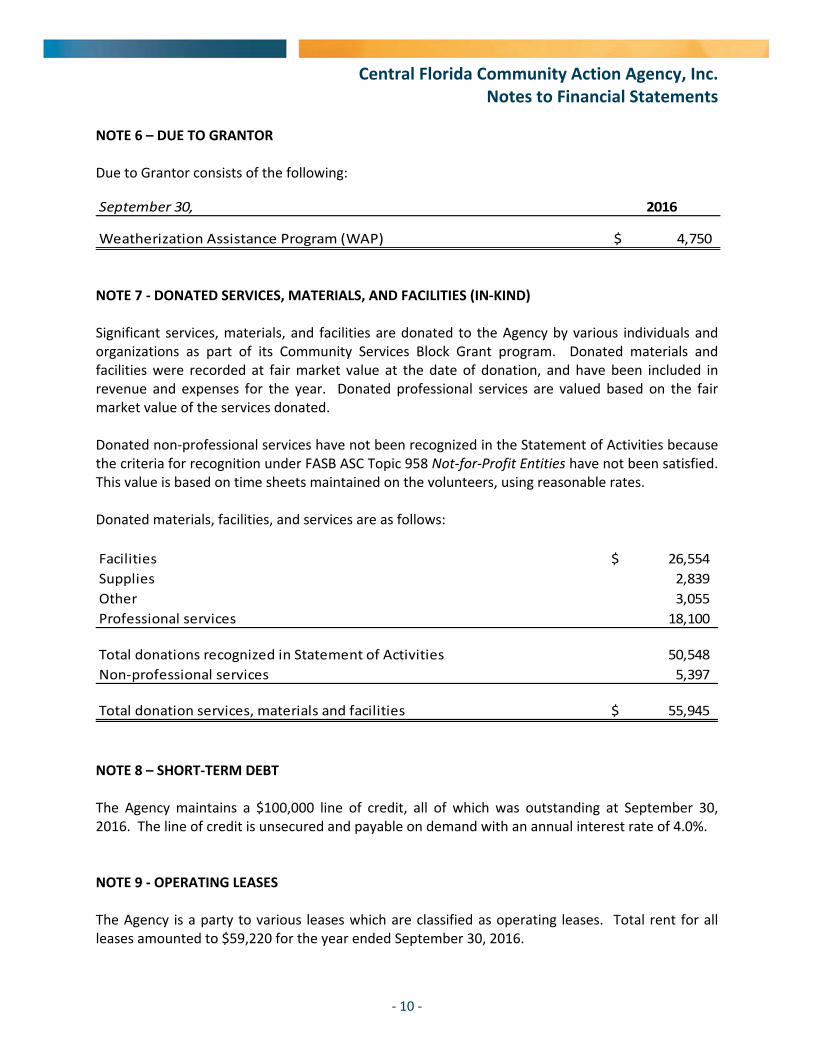

NOTE 6 – DUE TO GRANTOR Due to Grantor consists of the following:

September 30, 2016

Weatherization Assistance Program (WAP) 4,750$

NOTE 7 ‐ DONATED SERVICES, MATERIALS, AND FACILITIES (IN‐KIND) Significant services, materials, and facilities are donated to the Agency by various individuals and organizations as part of its Community Services Block Grant program. Donated materials and facilities were recorded at fair market value at the date of donation, and have been included in revenue and expenses for the year. Donated professional services are valued based on the fair market value of the services donated. Donated non‐professional services have not been recognized in the Statement of Activities because the criteria for recognition under FASB ASC Topic 958 Not‐for‐Profit Entities have not been satisfied. This value is based on time sheets maintained on the volunteers, using reasonable rates. Donated materials, facilities, and services are as follows:

Facilities 26,554$

Supplies 2,839

Other 3,055

Professional services 18,100

Total donations recognized in Statement of Activities 50,548

Non‐professional services 5,397

Total donation services, materials and facilities 55,945$

NOTE 8 – SHORT‐TERM DEBT The Agency maintains a $100,000 line of credit, all of which was outstanding at September 30, 2016. The line of credit is unsecured and payable on demand with an annual interest rate of 4.0%. NOTE 9 ‐ OPERATING LEASES The Agency is a party to various leases which are classified as operating leases. Total rent for all leases amounted to $59,220 for the year ended September 30, 2016.

Central Florida Community Action Agency, Inc. Notes to Financial Statements

‐ 11 ‐

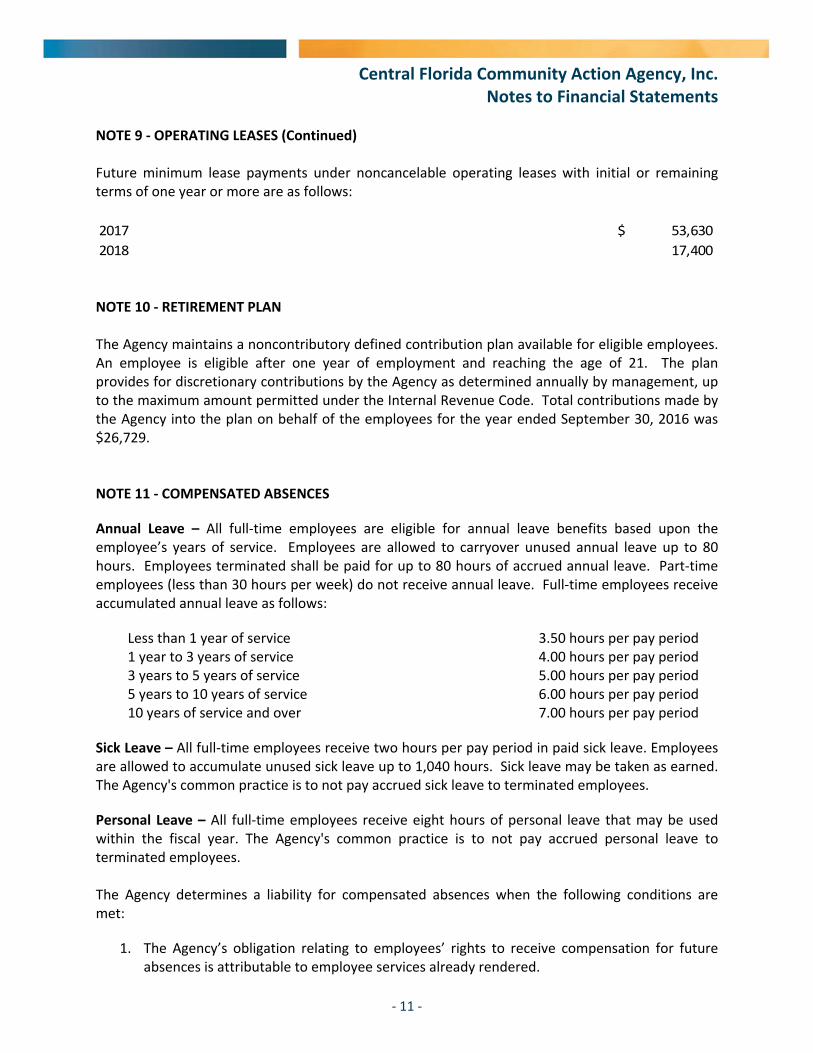

NOTE 9 ‐ OPERATING LEASES (Continued) Future minimum lease payments under noncancelable operating leases with initial or remaining terms of one year or more are as follows:

2017 53,630$

2018 17,400

NOTE 10 ‐ RETIREMENT PLAN The Agency maintains a noncontributory defined contribution plan available for eligible employees. An employee is eligible after one year of employment and reaching the age of 21. The plan provides for discretionary contributions by the Agency as determined annually by management, up to the maximum amount permitted under the Internal Revenue Code. Total contributions made by the Agency into the plan on behalf of the employees for the year ended September 30, 2016 was $26,729. NOTE 11 ‐ COMPENSATED ABSENCES

Annual Leave – All full‐time employees are eligible for annual leave benefits based upon the employee’s years of service. Employees are allowed to carryover unused annual leave up to 80 hours. Employees terminated shall be paid for up to 80 hours of accrued annual leave. Part‐time employees (less than 30 hours per week) do not receive annual leave. Full‐time employees receive accumulated annual leave as follows:

Less than 1 year of service 3.50 hours per pay period 1 year to 3 years of service 4.00 hours per pay period 3 years to 5 years of service 5.00 hours per pay period 5 years to 10 years of service 6.00 hours per pay period 10 years of service and over 7.00 hours per pay period

Sick Leave – All full‐time employees receive two hours per pay period in paid sick leave. Employees are allowed to accumulate unused sick leave up to 1,040 hours. Sick leave may be taken as earned. The Agency's common practice is to not pay accrued sick leave to terminated employees.

Personal Leave – All full‐time employees receive eight hours of personal leave that may be used within the fiscal year. The Agency's common practice is to not pay accrued personal leave to terminated employees. The Agency determines a liability for compensated absences when the following conditions are met:

1. The Agency’s obligation relating to employees’ rights to receive compensation for future absences is attributable to employee services already rendered.

Central Florida Community Action Agency, Inc. Notes to Financial Statements

‐ 12 ‐

NOTE 11 ‐ COMPENSATED ABSENCES (Continued)

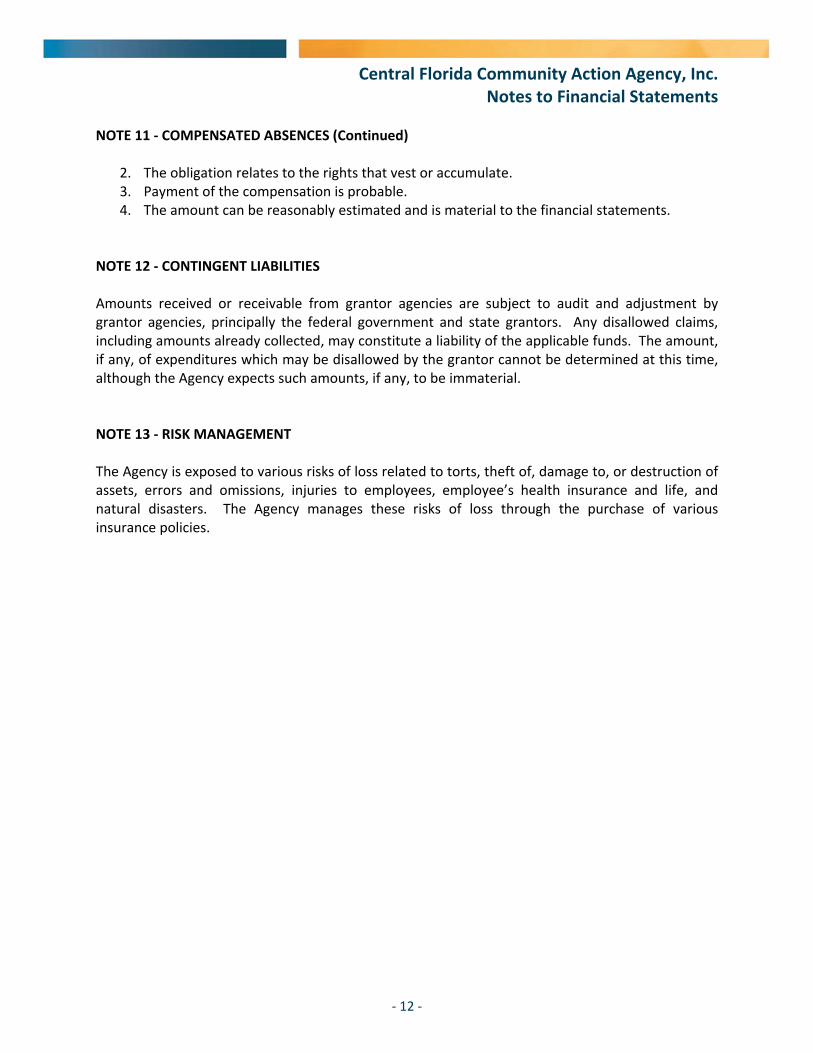

2. The obligation relates to the rights that vest or accumulate. 3. Payment of the compensation is probable. 4. The amount can be reasonably estimated and is material to the financial statements.

NOTE 12 ‐ CONTINGENT LIABILITIES Amounts received or receivable from grantor agencies are subject to audit and adjustment by grantor agencies, principally the federal government and state grantors. Any disallowed claims, including amounts already collected, may constitute a liability of the applicable funds. The amount, if any, of expenditures which may be disallowed by the grantor cannot be determined at this time, although the Agency expects such amounts, if any, to be immaterial.

NOTE 13 ‐ RISK MANAGEMENT The Agency is exposed to various risks of loss related to torts, theft of, damage to, or destruction of assets, errors and omissions, injuries to employees, employee’s health insurance and life, and natural disasters. The Agency manages these risks of loss through the purchase of various insurance policies.

Central Florida Community Action Agency, Inc. Schedule of Expenditures of Federal Awards

For the Year Ended September 30, 2016

See accompanying notes to Schedule of Expenditures of Federal Awards. ‐ 13 ‐

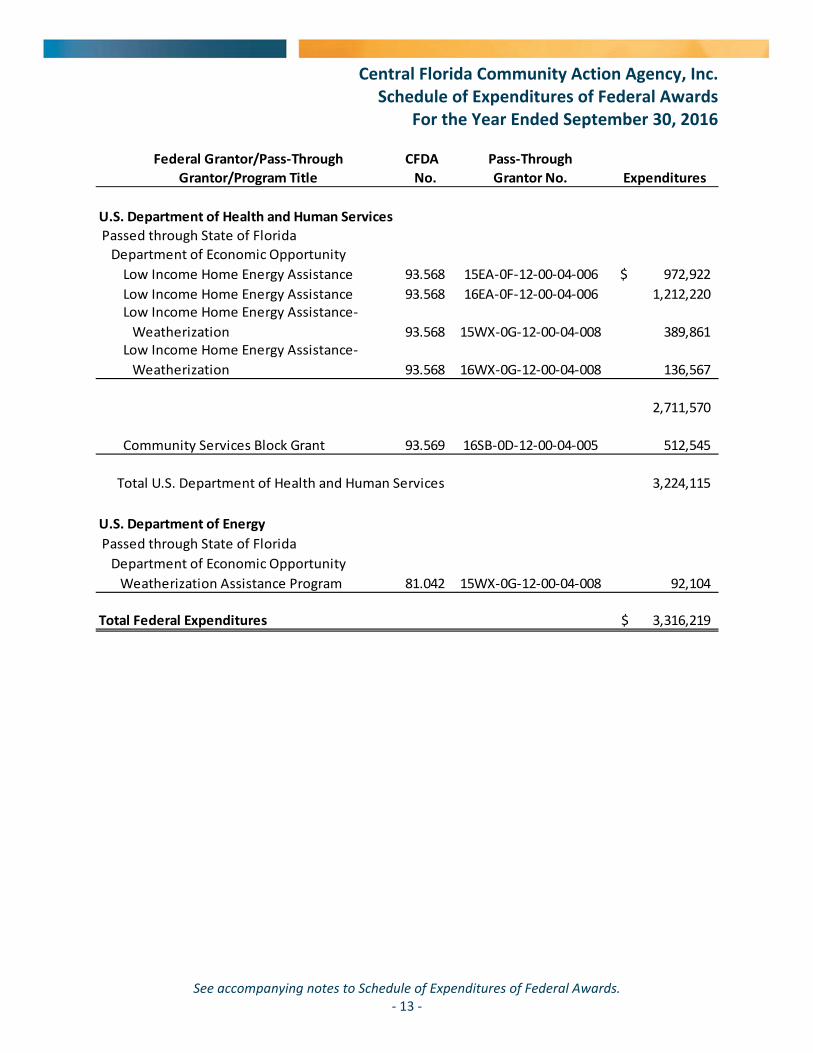

Federal Grantor/Pass‐Through CFDA Pass‐Through

Grantor/Program Title No. Grantor No. Expenditures

Passed through State of Florida

Department of Economic Opportunity

Low Income Home Energy Assistance 93.568 15EA‐0F‐12‐00‐04‐006 972,922$

Low Income Home Energy Assistance 93.568 16EA‐0F‐12‐00‐04‐006 1,212,220Low Income Home Energy Assistance‐

Weatherization 93.568 15WX‐0G‐12‐00‐04‐008 389,861Low Income Home Energy Assistance‐

Weatherization 93.568 16WX‐0G‐12‐00‐04‐008 136,567

2,711,570

Community Services Block Grant 93.569 16SB‐0D‐12‐00‐04‐005 512,545

3,224,115

U.S. Department of Energy

Passed through State of Florida

Department of Economic Opportunity

Weatherization Assistance Program 81.042 15WX‐0G‐12‐00‐04‐008 92,104

Total Federal Expenditures 3,316,219$

U.S. Department of Health and Human Services

Total U.S. Department of Health and Human Services

Central Florida Community Action Agency, Inc. Notes to Schedule of Expenditures of Federal Awards

For the Year Ended September 30, 2016

‐ 14 ‐

NOTE 1 – BASIS OF PRESENTATION

The accompanying Schedule of Expenditures of Federal Awards (SEFA) or (the “Schedule”) summarizes the federal expenditures of the Agency under programs of the federal government for the year ended September 30, 2016. The amounts reported as federal expenditures were obtained from the Agency’s general ledger. Because the Schedule presents only a selected portion of the operations, it is not intended to and does not present the financial position or changes in net assets of the Agency.

For purposes of the Schedule, federal awards include all grants, contracts, and similar agreements entered into directly with the federal government and other pass‐through entities. The Agency has obtained Catalog of Federal Domestic Assistance (CFDA) numbers to ensure that all programs have been identified in the Schedule. CFDA numbers have been appropriately listed by applicable programs. Federal programs with different CFDA numbers that are closely related because they share common compliance requirements are defined as a cluster by the Uniform Guidance. No clusters were identified in the Schedule.

NOTE 2 – RELATIONSHIP OF THE SCHEDULE TO PROGRAM FINANCIAL REPORTS

The amounts reflected in the financial reports submitted to the awarding federal and/or pass‐through agencies and the Schedule may differ. Some of the factors that may account for any difference include the following:

The Agency’s fiscal year end may differ from the program’s year end. Accruals recognized in the Schedule, because of year end procedures, may not be reported in

the program financial reports until the next program reporting period. Fixed assets purchases and the resultant depreciation charges recognized as fixed assets in

the Agency’s financial statements and as expenditures in the program financial reports.

NOTE 3 – BASIS OF ACCOUNTING

This Schedule was prepared on the modified accrual basis of accounting. The modified accrual basis differs from the full accrual basis of accounting in that expenditures for property, and equipment are expensed when incurred, rather than being capitalized and depreciated over their useful lives, and expenditures for the principal portion of debt service are expensed when incurred rather than being applied to reduce the outstanding principal portion of debt which conforms to the basis of reporting to grantors for reimbursement under the terms of the Agency’s federal grants.

NOTE 4 – FEDERAL PASS‐THROUGH FUNDS

The Agency is also the sub‐recipient of federal funds that have been subjected to testing and are reported as expenditures and listed as federal pass‐through funds. Federal awards other than those indicated as pass‐through funds are considered to be direct.

Central Florida Community Action Agency, Inc. Notes to Schedule of Expenditures of Federal Awards

For the Year Ended September 30, 2016

‐ 15 ‐

NOTE 5 – CONTINGENCIES Grant monies received and disbursed by the Agency are for specific purposes and are subject to review by the grantor agencies. Such audits may result in requests for reimbursement due to disallowed expenditures. Based upon prior experience, the Agency does not believe that such disallowance, if any, would have a material effect on the financial position of the Agency. As of September 30, 2016, there were no material questioned or disallowed costs as a result of grant audits in process or completed. NOTE 6 – NONCASH ASSISTANCE The Agency did not receive any federal noncash assistance for the fiscal year ending September 30, 2016. NOTE 7 – INDIRECT COST The Agency has not elected to use the 10% de Minimis indirect cost rate.

‐ 16 ‐

INDEPENDENT AUDITORS’ REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS Board of Directors Central Florida Community Action Agency, Inc. Gainesville, Florida We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of Central Florida Community Action Agency, Inc. (the "Agency"), which comprise the statement of financial position as of September 30, 2016, and the related statement of activities, and cash flows for the year then ended, and the related notes to the financial statements, and have issued our report thereon dated February 7, 2017. Internal Control Over Financial Reporting In planning and performing our audit of the financial statements, we considered the Agency’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the Agency’s internal control. Accordingly, we do not express an opinion on the effectiveness of the Agency’s internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies and therefore, material weaknesses or significant deficiencies may exist that were not identified. We did identify a deficiency in internal control, described in the accompanying schedule of findings and questioned costs that we considered to be material weakness and identified as [2016‐001].

‐ 17 ‐

Compliance and Other Matters As part of obtaining reasonable assurance about whether the Agency’s financial statements are free from material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. We noted certain matters that we reported to management of the Agency in a separate letter dated February 7, 2017. Agency’s Response to Findings The Agency’s response to the findings identified in our audit is described in the accompanying schedule of findings and questioned costs. The Agency’s response was not subjected to the auditing procedures applied in the audit of the financial statements and, accordingly, we express no opinion on it. Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the Agency’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the Agency’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

CARR, RIGGS & INGRAM, L.L.C. Certified Public Accountants February 7, 2017

‐ 18 ‐

INDEPENDENT AUDITORS’ REPORT ON COMPLIANCE FOR EACH MAJOR PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE REQUIRED BY THE UNIFORM GUIDANCE Board of Directors Central Florida Community Action Agency, Inc. Gainesville, Florida Report on Compliance for Each Major Federal Program We have audited Central Florida Community Action Agency, Inc. (the "Agency's") compliance with the types of compliance requirements described in the OMB Compliance Supplement that could have a direct and material effect on the Agency's major federal program for the year ended September 30, 2016. The Agency’s major federal programs are identified in the summary of auditor’s results section of the accompanying schedule of findings and questioned costs. Management’s Responsibility

Management is responsible for compliance with the requirements of federal statutes, regulations, and terms and conditions of its federal awards applicable to its federal programs.

Auditors’ Responsibility

Our responsibility is to express an opinion on compliance on the Agency’s major federal program based on our audit of the types of compliance requirements referred to above. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the audit requirements of Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). Those standards and the Uniform Guidance require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about the Agency’s compliance with those requirements and performing such other procedures as we considered necessary in the circumstances.

We believe that our audit provides a reasonable basis for our opinion on compliance for the major federal program. However, our audit does not provide a legal determination of the Agency’s compliance.

Opinion on Each Major Federal Program

In our opinion, the Agency complied, in all material respects, with the types of compliance requirements referred to above that could have a direct and material effect on each of its major federal programs for the year ended September 30, 2016.

‐ 19 ‐

Report on Internal Control Over Compliance

Management of the Agency is responsible for establishing and maintaining effective internal control over compliance with the types of compliance requirements referred to above. In planning and performing our audit of compliance, we considered the Agency’s internal control over compliance with the types of requirements that could have a direct and material effect on its major federal program to determine the auditing procedures that are appropriate in the circumstances for the purpose of expressing an opinion on compliance for the major federal program and to test and report on internal control over compliance in accordance with the Uniform Guidance, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of the Agency’s internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. A significant deficiency in internal control over compliance is a deficiency, or a combination of deficiencies, in internal control over compliance with a type of compliance requirement of a federal program that is less severe than a material weakness in internal control over compliance, yet important enough to merit attention by those charged with governance. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be material weaknesses or significant deficiencies. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified. The purpose of this report on internal control over compliance is solely to describe the scope of our testing of internal control over compliance and the results of that testing based on the requirements of the Uniform Guidance. Accordingly, this report is not suitable for any other purpose.

CARR, RIGGS & INGRAM, L.L.C.

Certified Public Accountants

February 7, 2017

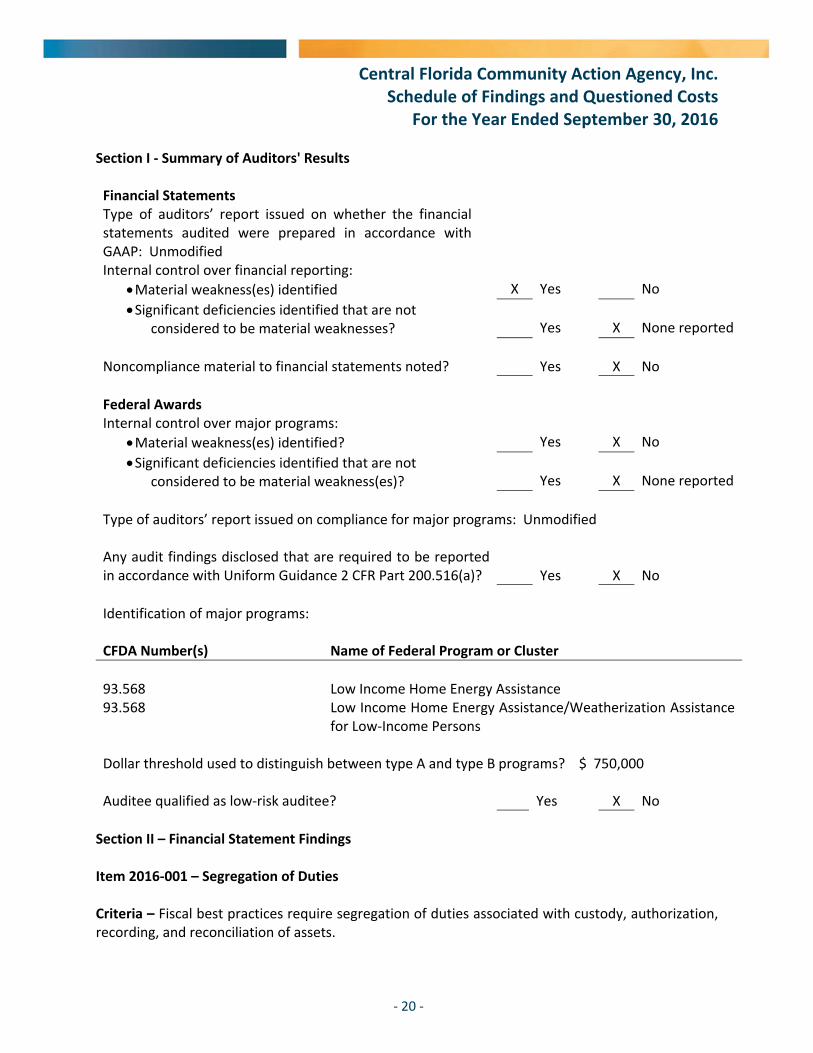

Central Florida Community Action Agency, Inc. Schedule of Findings and Questioned Costs

For the Year Ended September 30, 2016

‐ 20 ‐

Section I ‐ Summary of Auditors' Results Financial Statements Type of auditors’ report issued on whether the financial statements audited were prepared in accordance with GAAP: Unmodified

Internal control over financial reporting:

Material weakness(es) identified X Yes No

Significant deficiencies identified that are not considered to be material weaknesses?

Yes

X

None reported

Noncompliance material to financial statements noted? Yes X No

Federal Awards Internal control over major programs:

Material weakness(es) identified? Yes X No

Significant deficiencies identified that are not considered to be material weakness(es)?

Yes

X

None reported

Type of auditors’ report issued on compliance for major programs: Unmodified Any audit findings disclosed that are required to be reported in accordance with Uniform Guidance 2 CFR Part 200.516(a)?

Yes

X

No

Identification of major programs: CFDA Number(s) Name of Federal Program or Cluster

93.568 Low Income Home Energy Assistance 93.568 Low Income Home Energy Assistance/Weatherization Assistance

for Low‐Income Persons Dollar threshold used to distinguish between type A and type B programs? $ 750,000 Auditee qualified as low‐risk auditee? Yes X No

Section II – Financial Statement Findings Item 2016‐001 – Segregation of Duties Criteria – Fiscal best practices require segregation of duties associated with custody, authorization, recording, and reconciliation of assets.

Central Florida Community Action Agency, Inc. Schedule of Findings and Questioned Costs

For the Year Ended September 30, 2016

‐ 21 ‐

Condition – Due to the Human Resource Director and other employees vacating employment during the fiscal year the accounting department was left susceptible to a segregation of duties issue. The Chief Financial Officer took on the individual responsibilities that included setting up all employees in payroll, entering payroll, and transmitting the payroll funds for disbursement. Additionally, she was also responsible for preparing and documenting all accounts payable disbursements and preparing the checks for payment. This results in a deficiency relating to the control and recording of disbursements. It was also noted that this same employee had the ability to add and delete users to the accounting software while having access to all modules within the accounting system, as well as prepare and record all journal entries, with no review process in place. Effect – The ability of one user to have unlimited access to accounting software and to authorize, initiate and record transactions without proper review and approval could result in misappropriation of assets. Recommendation – We recommend that the Agency implement procedures that ensure adequate segregation of duties, such as removing a user who has unlimited access in the accounting software from also have the ability to add and remove users, adding a review process for journal entries, and eliminating setting up employees in payroll from being with the person who also pays those disbursements. Where these adequate segregations cannot be reached, due to limitations in staff size, we recommend implementation of mitigating controls. Section III – Federal Award Findings and Questioned Costs No such findings noted.

Central Florida Community Action Agency, Inc. Summary Schedule of Prior Audit Findings for Federal Awards

For the Year Ended September 30, 2016

‐ 22 ‐

Financial Statement Findings 2015‐001 Corrected

Central Florida Community Action Agency, Inc. Corrective Action Plan

For the Year Ended September 30, 2016

‐ 23 ‐