Adapting Healthcare Messages For Pregnant Indigenous Australian Women

Home

© 2018 – FinPro, Inc. 0158 Route 206 North � Gladstone, NJ 07934 � P: (908) 234-9398 � [email protected] � www.finpro.us

Adapting the Community Banking Business Model

Home

© 2018 – FinPro, Inc.

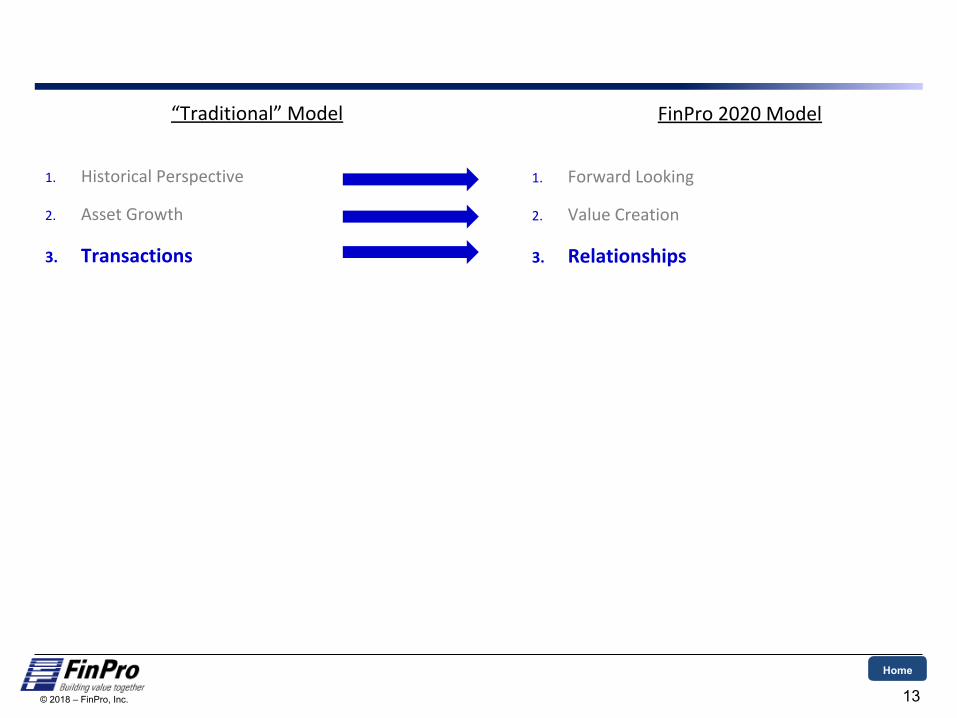

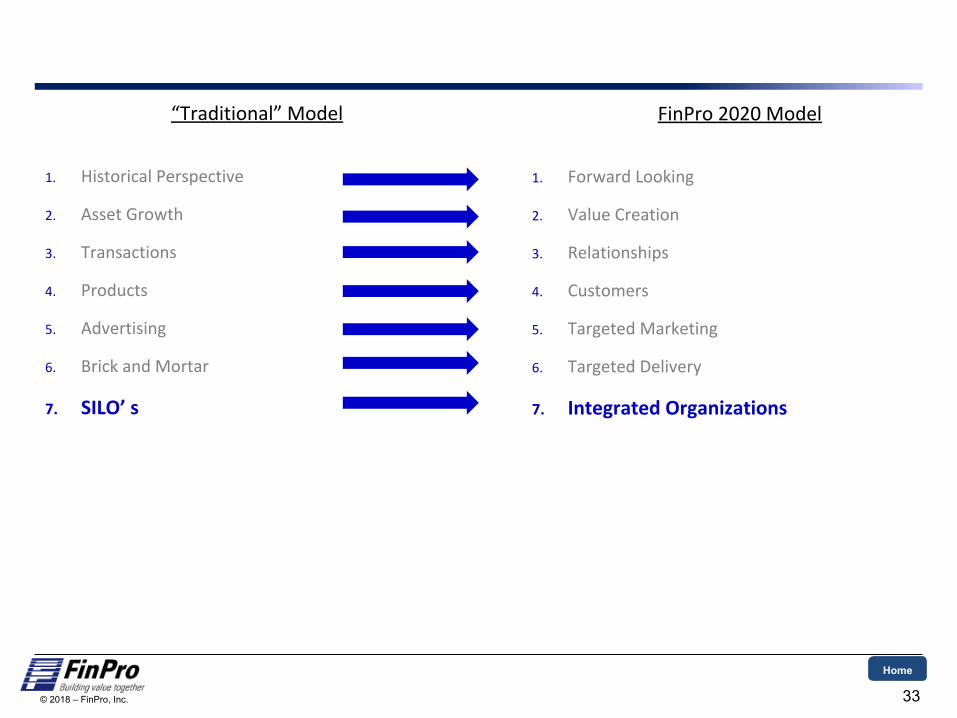

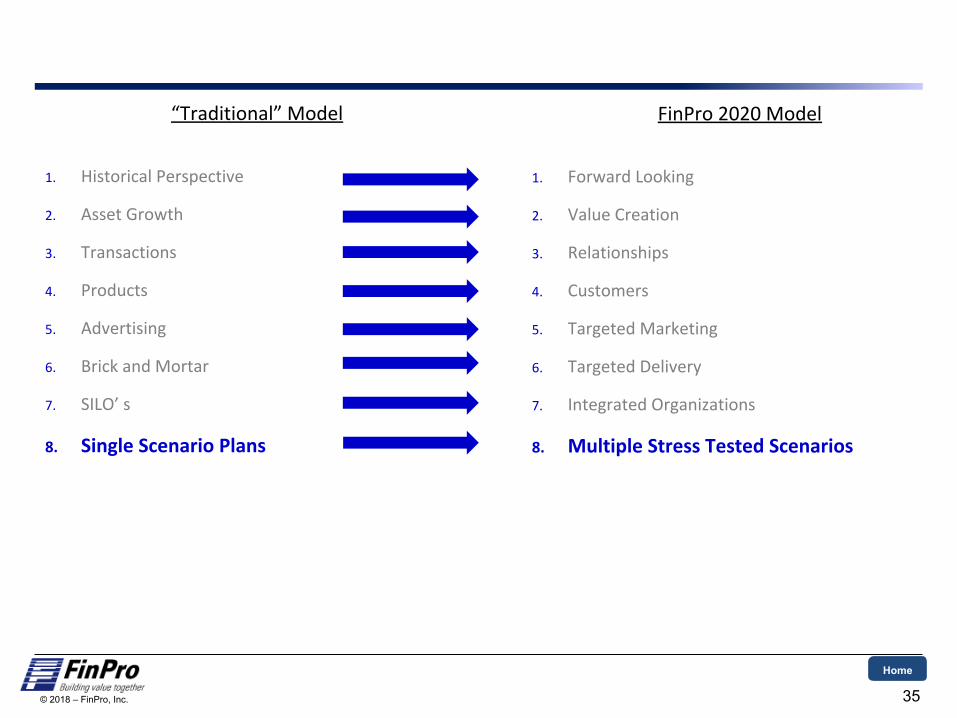

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

8. Single Scenario Plans

9. Regulatory Constraints

10. Departmental Risk

11. Board Micromanagement

12. Human Resources

13. People Intensive

1

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

8. Multiple Stress Tested Scenarios

9. Market Opportunities

10. Integrated ERM

11. Effective Corporate Governance

12. Talent Management

13. Digital Intensive

The “traditional” community banking model may be dead! New organizations with strong leadership will recognize the new paradigm and enact change accordingly . . .

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2

FinPro 2020 Model

1. Forward Looking

Home

© 2018 – FinPro, Inc.

This holistic process provides multiple scenarios which can be stress tested on an individual variable or complete DFAST scenario basis . . .

3

Historic Analysis:Reactionary process using stale data

Dynamic Analysis:Forward looking pro-active process

Don’t stress test here Model & stress test here

Traditional Future

Decision

Tree 1

Decision Tree 2

Stress Test 2

Stress

Test 1

Selected Planning ScenarioHistorical Performance Analysis

Home

© 2018 – FinPro, Inc.

Complicating the need to look forward, markets are no longer simply geographically defined so the traditional quantitative monitoring mechanisms much change. . .

In the new paradigm, they must measure market share by:

§ Customer Segment

§ Delivery Channel

§ Line of Business (Product)

§ Niche

§ Geography

4

Banks have traditionally measured market share by geography and then by Line of Business (Product).

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

5

FinPro 2020 Model

1. Forward Looking

2. Value Creation

Home

© 2018 – FinPro, Inc.

How to create and sustain value . . .

6

1. Understand Value Concepts

- How to measure value

- How to realize value

- How to quantify value

2. Know the Market Conditions for Multiples

- Trading multiples

- Take-out multiples

3. Evaluate your organizations current value proposition

- Value creators and detractors

- Your current market multiples compared to the industry

- Understand what your value is in a sale today

4. Create a strategic plan to maximize value

- Determine the level of value creation needed for your organization.

- Create a financial forecast of what the Company needs to be in 3 to 5 years to achieve this target

- Identify a decision tree to determine the potential paths to achieve success

5. Execute on the strategic plan

- Remove obstacles and hold individuals accountable

- Constantly re-evaluate to find better strategies and improve performance

Home

© 2018 – FinPro, Inc.

The strategic value model drives home this point . . .

7

Home

© 2018 – FinPro, Inc. 8

Value is driven by EPS and TBVS . . .

Stock price has a strong correlation to Earnings Per Share as the R2 value of 79.64% is approaching 1.0.

Stock price has a strong correlation to Tangible Book Value Per Share as the R2 value of 85.32% is approaching 1.0.

Sources:SNL Financial

Home

© 2018 – FinPro, Inc. 9

Banks trade on EPS and TBVS based on where they are in their life cycle . . .

Home

© 2018 – FinPro, Inc.

Risk, Governance and Regulation drives Strategy drives Value . . .

10

RegulationGovernanceRisk

Market Multiple

TBVS or

EPS

Strategy

ValueC A M E L S +

Risk, Governance and Regulation drives strategy drives value

Market Multiples are “the market’s perception of the risk profile of the bank”Strategy is executed both organically and via acquisition

M&A Organic

Home

© 2018 – FinPro, Inc.

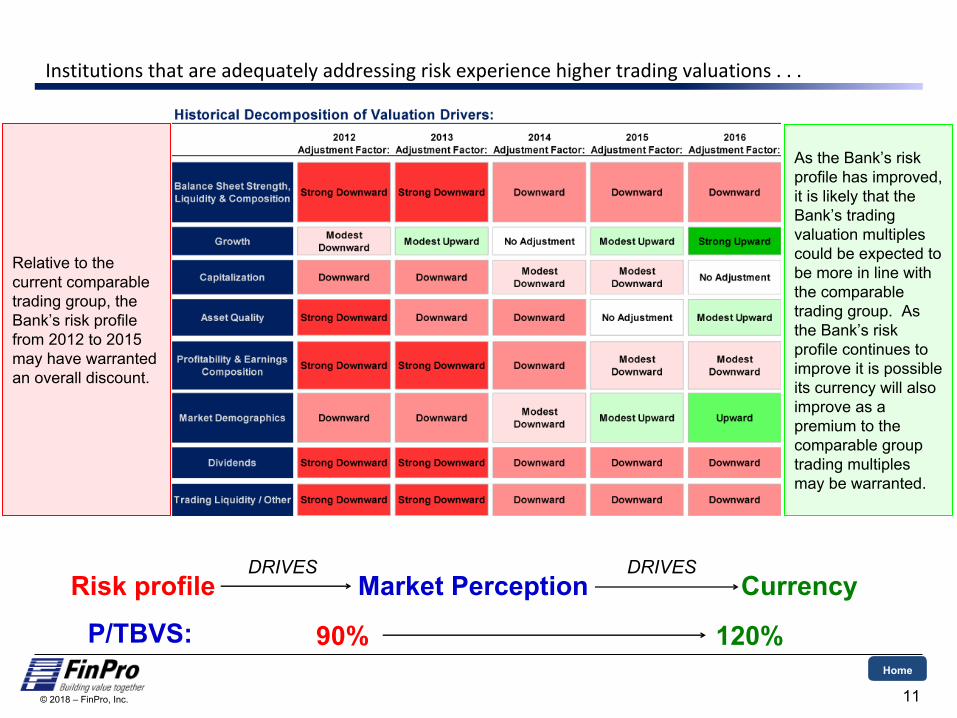

Institutions that are adequately addressing risk experience higher trading valuations . . .

11

Risk profile Market Perception CurrencyDRIVES DRIVES

P/TBVS: 90% 120%

Relative to the current comparable trading group, the Bank’s risk profile from 2012 to 2015 may have warranted an overall discount.

As the Bank’s risk profile has improved, it is likely that the Bank’s trading valuation multiples could be expected to be more in line with the comparable trading group. As the Bank’s risk profile continues to improve it is possible its currency will also improve as a premium to the comparable group trading multiples may be warranted.

Home

© 2018 – FinPro, Inc.

Improving your risk profile builds as much value as growing earnings . . .

12

EPS Multiple Stock Price

Today $ 5.00 12.00 $ 60.00 12 Months $ 5.50 12.00 $ 66.00

Change $ 0.50 - $ 6.00 10.00% 0.00% 10.00%

EPS Multiple Stock Price

Today $ 5.00 12.00 $ 60.00 12 Months $ 5.00 15.00 $ 75.00

Change $ - 3.00 $ 15.00 0.00% 25.00% 25.00%

EPS Multiple Stock Price

Today $ 5.00 12.00 $ 60.00 12 Months $ 5.50 15.00 $ 82.50

Change $ 0.50 3.00 $ 22.50 10.00% 25.00% 37.50%

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

13

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

Home

© 2018 – FinPro, Inc. 14

The concentric circle of Relationship . . .

Customer

Family

Friends

Neighbors

Business Associate

Home

© 2018 – FinPro, Inc. 15

Internal relationships provide access and influence . . .

Don

Admin

Counsel

Wife

Home

© 2018 – FinPro, Inc.

The key to relationships is understanding who is the gatekeeper . . .

16

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

17

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

Home

© 2018 – FinPro, Inc.

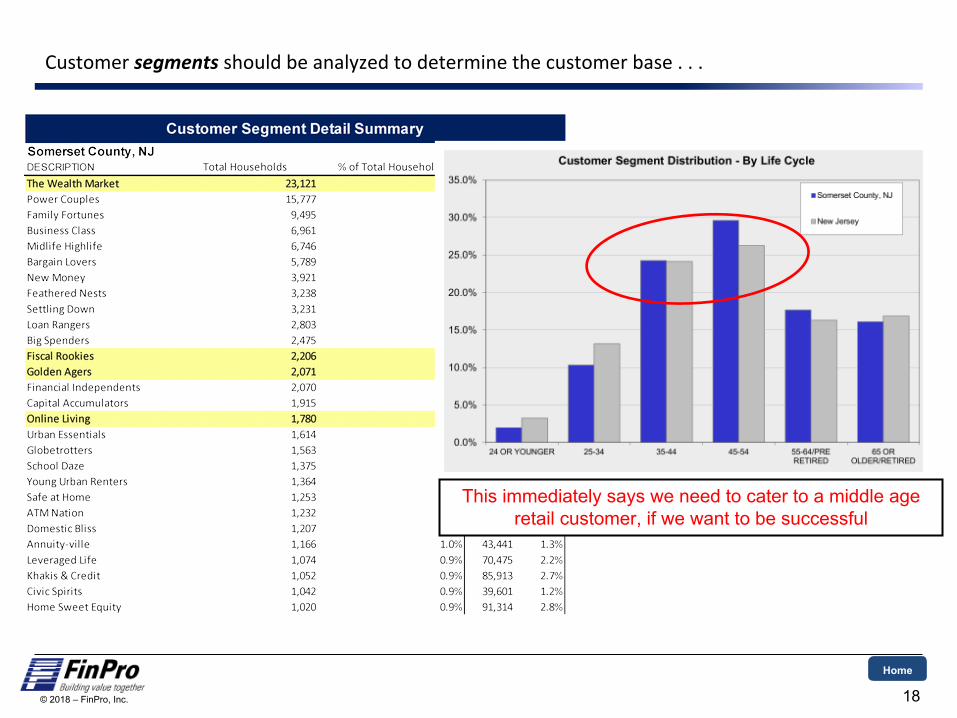

Customer segments should be analyzed to determine the customer base . . .

18

This immediately says we need to cater to a middle age retail customer, if we want to be successful

Home

© 2018 – FinPro, Inc.

As such we must understand the needs and markets accordingly . . .

§ 65 years and older with strong income producing assets.

§ Invest in corporate and municipal bonds, government securities, fixed-rate annuities and savings accounts.

§ Own multiple annuities and long-term care insurance.

§ Leave investment decisions to brokers at full-service brokerage firms focused on recurring income.

§ High levels of deposits, low level of loans.

19

Golden AgersThe Wealth Market Online LivingFiscal Rookies§ Young couples and

families.§ Relatively high incomes§ 25- to 44-year-olds § Not saving a lot of

money § Average levels of

income-producing assets.

§ Carry debt from student and auto loans

§ First home mortgages§ Dabbling in investment-

style insurance and mutual funds for their 401(k)s.

§ Suburban couples over age 55, with more than $1 million in income-producing assets.

§ Investing in a broad range of stocks, corporate/municipal bonds, mutual funds and real estate.

§ Hiring a financial managers, estate planners and full-service brokers.

§ Limited utilization of borrowings.

§ Large deposit balances waiting to be deployed into earning assets.

§ 25- to 34-year-old couples and families, upper middle class living in suburban towns and areas.

§ High utilization of online banking, stock trading and bill paying.

§ Own a homes and have upscale incomes, but only have modest levels of income-producing assets and are still paying off student and personal loans.

§ Purchase life insurance policy to protect the family.

Home

© 2018 – FinPro, Inc.

Commercial customer segmentation is also critical (based on NAICS codes) . . .

20

- Cash Management- Payment Card Processing- On Site ATM / Branch- Wire Transfer / Money Order

Management

- IOLTA Accounts- ESCROW Accounts- Fraud / Identity Protection- Tax Filing Documentation- Foreign Currency Exchange- Asset Management

Food and Beverage Stores 8,750 1.9%

Crop Production 616 0.1%

Professional, Scientific, and Technical Services 51,043 11.2%

- Equipment Financing- Business Lines of Credit- Real Estate Financing- Business Overdraft Protection

Home

© 2018 – FinPro, Inc.

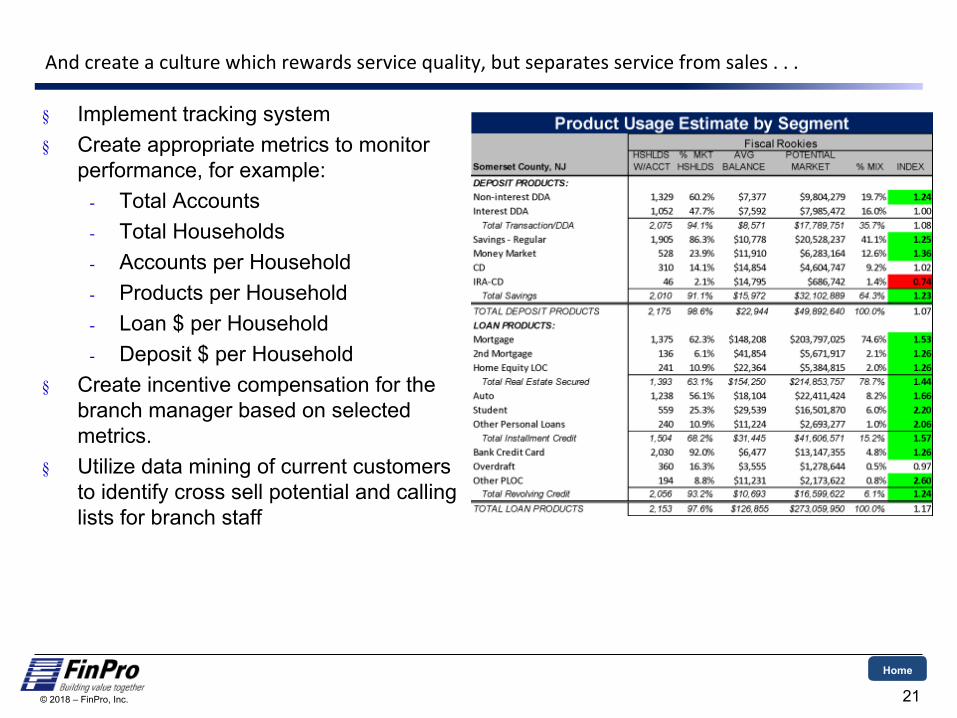

§ Implement tracking system§ Create appropriate metrics to monitor

performance, for example:- Total Accounts- Total Households- Accounts per Household- Products per Household- Loan $ per Household- Deposit $ per Household

§ Create incentive compensation for the branch manager based on selected metrics.

§ Utilize data mining of current customers to identify cross sell potential and calling lists for branch staff

And create a culture which rewards service quality, but separates service from sales . . .

21

Home

© 2018 – FinPro, Inc.

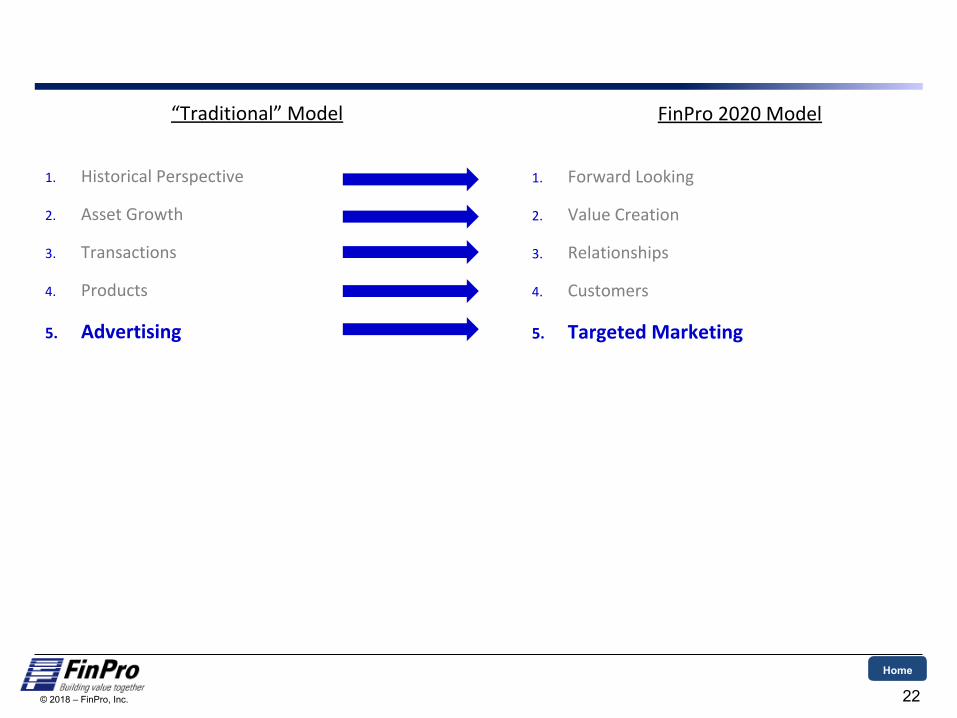

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

22

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

Home

© 2018 – FinPro, Inc. 23

Can they really do that?

Home

© 2018 – FinPro, Inc. 24

Bank segment share and a list of targeted households will focus sales efforts . . .

Home

© 2018 – FinPro, Inc. 25

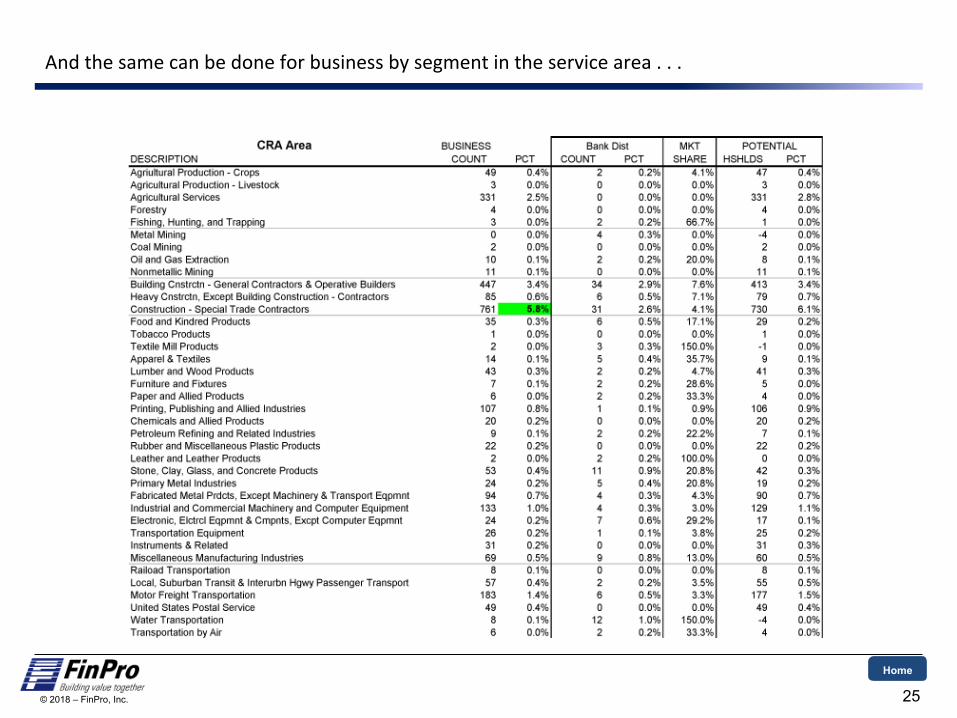

And the same can be done for business by segment in the service area . . .

Home

© 2018 – FinPro, Inc. 26

Once the markets and customers are identified, banks must ensure that they have the right FRANCHISE - people, systems and delivery channels in place . . .

Segment

Identi-fication

Ascertain

Needs

Link

ProductsTo Needs

Effective

Delivery ofProducts

Sales

Culture

Sales Process

Home

© 2018 – FinPro, Inc. 27

The data is available for how people get information and entertainment . . .

Home

© 2018 – FinPro, Inc. 28

And there is considerable lifestyle data available . . .

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

29

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

Home

© 2018 – FinPro, Inc. 30

The impact of changing demographics can be seen clearly as branches are declining while deposits continue to rise . . .

Note: Data provided by SNL Financial

Home

© 2018 – FinPro, Inc.

Refocus on business development instead of traditional branch managers and expand electronic media outlets and delivery . . .

31

Human Delivery

Digital Delivery

Call Center Delivery

Mini Branch Delivery

Home

© 2018 – FinPro, Inc.

The structure of the delivery systems should be predicated on the product types (deposit maintenance, money transfer, customer communication) and target customer . . .

Source: Federal Reserve: Consumers and Mobile Financial Services 2014 32

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

33

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

Home

© 2018 – FinPro, Inc. 34

Integrating the organization requires a reworking of the organization structure to make it customer centric, not product centric . . .

Asset Mngmt InsuranceDeposits

Trust

C & I

CRE

Cash Mngmt

Relationship Manager Credit Cards

Mortgage Brokerage

401k529 AccountsCustomer

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

8. Single Scenario Plans

35

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

8. Multiple Stress Tested Scenarios

Home

© 2018 – FinPro, Inc.

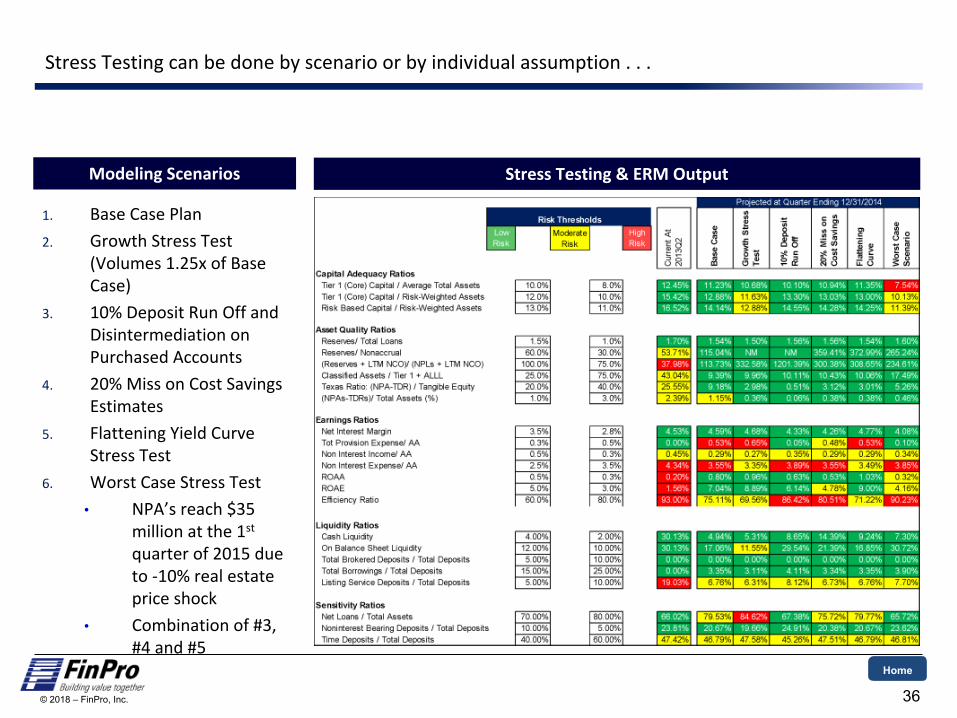

Stress Testing can be done by scenario or by individual assumption . . .

36

1. Base Case Plan

2. Growth Stress Test (Volumes 1.25x of Base Case)

3. 10% Deposit Run Off and Disintermediation on Purchased Accounts

4. 20% Miss on Cost Savings Estimates

5. Flattening Yield Curve Stress Test

6. Worst Case Stress Test

• NPA’s reach $35 million at the 1st quarter of 2015 due to -10% real estate price shock

• Combination of #3, #4 and #5

Modeling Scenarios Stress Testing & ERM Output

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

8. Single Scenario Plans

9. Regulatory Constraints

37

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

8. Multiple Stress Tested Scenarios

9. Market Opportunities

Home

© 2018 – FinPro, Inc.

2015 2017

38

Capital

Asset Quality

Management

LiquidityLegal &Regulatory

ReputationITValuation

CorpGovernance

BSA

Strategic

RiskManagement

Compliance

Operational

Sensitivity

The chart above illustrates the CAMELS+ components and the overall regulatory focus on each component. Over time, each of these components shift based upon the overall projected banking environment.

Earnings

CRA

Based on recent exam report findings, regulators are focusing more on liquidity risk, corporate governance, risk management and information technology (IT) risks . . .

Home

© 2018 – FinPro, Inc.

Now is the time to conduct deposit loyalty and propensity to renew studies . . .

§ Data is collected from the Bank for each of the Propensity to Renew factors

1. Relationship (number of accounts/services)

2. Transactions (number of transactions a month)

3. Price (above/below market rate)

4. Geography (within/outside market area)

5. Digital Footprint (utilization of digital services)

6. Tenure (age of account)

7. Size (balance of account)

39

Home

© 2018 – FinPro, Inc.

Beware of Pending Regulatory issues and change.

§ Key concepts

- Credible challenge

- Presumptive knowledge

- Documentation Reality

§ Pending changes

- Otting is confirmed as Comptroller of Currency

- Jelena McWilliams nominated as Chair of the FDIC

- Mick Mulvaney – Temporary Head of CFPB

§ Some politicians apoplectic over demise of consumer activism

§ Powell is new FRB Chair

- Quarles as Vice Chair and head of Supervision

- FRB – Vice Chair and 3 other Open FRB Board Seats (4 of 7 empty)

- Thomas Barkin named as Richmond Fed President

- Williams at New York Fed

40

Home

© 2018 – FinPro, Inc. 41

Will the new Regulatory regime promote new entrants?

1. New comprehensive FDIC guidance2. OCC pushing for new charters, and was pushing for broader authorities3. States, FDIC pushing for more entrants4. Federal Reserve in fight to remain relevant5. Elimination of one size fits all mentality6. Promoting denovos

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

8. Single Scenario Plans

9. Regulatory Constraints

10. Departmental Risk

42

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

8. Multiple Stress Tested Scenarios

9. Market Opportunities

10. Integrated ERM

Home

© 2018 – FinPro, Inc. 43

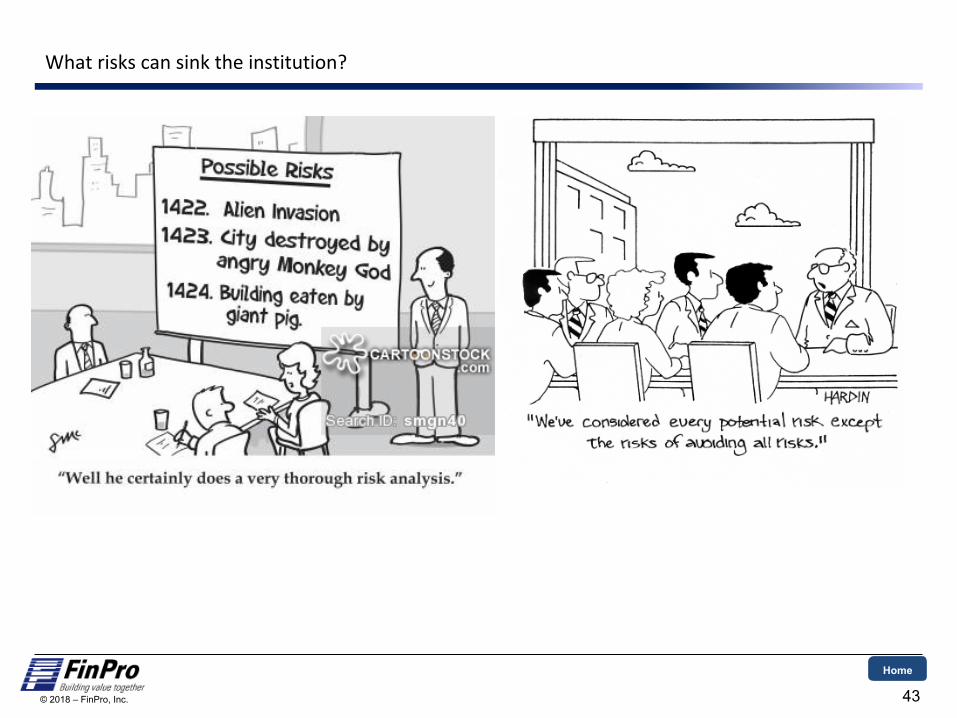

What risks can sink the institution?

Home

© 2018 – FinPro, Inc.

The regulators have recommended utilization of a stress testing framework within ERM that includes . . .

§ Augmenting risk identification and measurement

§ Estimating business line revenues and losses and informing business line strategies

§ Identifying vulnerabilities and assessing their potential impact

§ Assessing capital adequacy and enhancing capital planning

§ Assessing liquidity adequacy and informing contingency funding plans

§ Contributing to strategic planning

§ Enabling senior management to better integrate strategy, risk management, and capital and liquidity planning decisions

§ Assisting with recovery planning

44Source: Proposed Guidance on Stress Testing for Banking Organizations with more than $10 billion in Total Consolidated Assets issued June 7, 2011.

Home

© 2018 – FinPro, Inc.

The regulators understand that ERM and stress testing are forward looking, ongoing, size dependent, and integrated into the normal management decision making process . . .

§ The agencies have issued the proposed guidance “… to emphasize the importance of stress testing as an ongoing risk management practice that supports banking organizations’ forward-looking assessment and better equips them to address a range of adverse outcomes.”

§ “A banking organization should develop and implement its stress testing framework in a manner commensurate with its size, complexity, business activities, and overall risk profile.”

§ “A banking organization should ensure that the stress testing framework is not isolated within a banking organization’s risk management function, but is firmly integrated into business lines, capital and asset-liability committees, and other decision-making bodies.”

45Source: Proposed Guidance on Stress Testing for Banking Organizations with more than $10 billion in Total Consolidated Assets issued June 7, 2011.

Home

© 2018 – FinPro, Inc.

As such, the regulators have called for more detailed integrated modeling and analytics . . .

1. Scenario analysis

- A bank applies historical or hypothetical scenarios to assess the impact of various events and circumstances, including extreme ones.

2. Sensitivity analysis

- A bank’s assessment of its exposures, activities, and risks when certain variables, parameters, and inputs are “stressed” or “shocked”.

3. Enterprise-wide stress testing

- A bank’s assessment of the impact of certain specified scenarios on the banking organization as a whole, particularly on capital and liquidity.

4. Reverse stress testing

- Allows banks to assume a known adverse outcome and then deduce the types of events that could lead to such an outcome.

46Source: Proposed Guidance on Stress Testing for Banking Organizations with more than $10 billion in Total Consolidated Assets issued June 7, 2011.

Home

© 2018 – FinPro, Inc.

When implemented successfully, ERM . . .

§ Builds and protects shareholder value

§ Improves bank performance by focusing Board and Management

§ Identifies, measures, monitors, and controls all risks on an integrated basis

§ Avoids unnecessary regulatory downgrades and associated costs

§ Limits liability of Boards and Officers

§ Becomes the source document for strategic planning

§ Provides quarterly asset/liability and stress testing analytics

47

Home

© 2018 – FinPro, Inc.

Effective ERM can help an institution avoid a downgrade in its CAMELS rating, which would put an institution under stress in a number of areas and materially limit the banks plans for the immediate future . . .

§ Increased FDIC premiums.

§ Increased operating expense, including higher audit and examination expense and increased legal and professional fees.

§ Limitations on borrowing at the FHLB and unsecured lines.

§ Prohibition on the use of brokered deposits.

§ Deposit rate restrictions limited to the national rate cap.

§ Forced reductions in loan concentrations.

§ Limits on allowable growth.

§ Higher capital requirements.

§ Increased liquidity requirements.

§ Can subject the Bank to informal or formal enforcement actions

48

Home

© 2018 – FinPro, Inc. 49

An effective ERM program should account for regulatory “hot buttons” when assessing the level and trend of the Bank’s risk profile . . .

Home

© 2018 – FinPro, Inc. 50

What external risks could derail new banks?

1. Weakening economy at some point- Fear of recession- Current levels of debt cannot be sustained- Rates and Yield Curve

2. Bad Political Policy3. Intended and unintended consequences of Federal Tax Law4. Regulatory Overreach

- Losing our competitive advantages- More costly, ineffective rules

5. Inability to execute new business model6. Changing Customer needs and expectations

Home

© 2018 – FinPro, Inc. 51

The problem is not revenue, it is SPENDING . . .

Reagan

Clinton

Bush

Obama

Home

© 2018 – FinPro, Inc.

Neither party can spell fiscal discipline, witness the recently approved Federal Budget . . .

52

Home

© 2018 – FinPro, Inc.

Which causes the Federal Debt to grow at an increasing pace . . .

53

Home

© 2018 – FinPro, Inc.

And the Federal Reserve plan to unwind Quantitative Easing could cause rapid rising rates and could throw the economy into recession . . .

54

Home

© 2018 – FinPro, Inc. 55

Current levels of debt cannot be sustained . . .

1. Federal Debt > $20 Trillion2. States are in bad shape – So they can’t raise taxes to solve problem

- Puerto Rico- Connecticut- New Jersey- Illinois

3. Cities are in trouble – Will States allow Municipal Bankruptcy?- Hartford- Chicago- Detroit- Portland????

Home

© 2018 – FinPro, Inc. 56

Bank consequences from economy . . .

§ Rates will rise if:- The markets believe in continued reform - FRB holds or shrinks its portfolio- GDP sustains at 3% or more

§ Rates fall if:- Congress continues to be inept at everything- More qualitative easing occurs- GDP returns to around 1.5%

§ Any of the current bubbles burst- Education- Automobile- Jumbo Residential- Agriculture- Multifamily- CRE

Home

© 2018 – FinPro, Inc. 57

What does the State Tax landscape look like?

Source: Kiplinger

Best Tax StateNext Best StateNeutralBad Tax StateHorrific Tax State

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

8. Single Scenario Plans

9. Regulatory Constraints

10. Departmental Risk

11. Board Micromanagement

58

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

8. Multiple Stress Tested Scenarios

9. Market Opportunities

10. Integrated ERM

11. Effective Corporate Governance

Home

© 2018 – FinPro, Inc.

Corporate Governance Guidance . . .

• OCC – Spring 2016

• FDIC – Spring/Summer 2016

• Federal Reserve – August 2017

59

FEDERAL RESERVE SYSTEM [Docket No. OP–1570] Proposed Guidance on Supervisory Expectations for Boards of Directors AGENCY: Board of Governors of the Federal Reserve System (Board). ACTION: Notice; extension of comment period. SUMMARY: On August 9, 2017, the Board published in the Federal Register proposed guidance on supervisory expectations for boards of directors. To facilitate effective public comment on the proposal, the Board previously extended the comment period from October 10, 2017, to November 30, 2017. The Board has determined that an additional extension of the comment period until February 15, 2018, is appropriate

Home

© 2018 – FinPro, Inc.

• Strategic risk remains an ongoing concern.

• Banks are several years into the risk accumulation phase of the economic cycle.

• The banking environment continues to evolve, with growing competition among banks, nonbanks, and financial technology firms.

• Banks are increasingly offering innovative products and services, enabling them to better meet the needs of their customers.

• While doing so may heighten strategic risk if banks do not use sound risk management practices that align with their overall business strategies, failure to innovate to meet evolving needs or financial services may place a bank at a competitive disadvantage

• Strategic risk primarily includes adequacy of business models, board and management succession, breadth and depth of staff expertise, and the search for new market niches.

• Heightened lending competition pushes some banks to relax credit structure and terms as these banks adopt growth strategies that target new business segments.

• Banks are increasingly adopting innovative products, services, and processes in response to the evolving demand. Doing so often involves assuming unfamiliar risks, expanded reliance on third-party relationships, and the need to update or acquire new information systems and technology platforms.

• In this extended low interest rate environment some banks are reaching for yield by extending asset duration.

60

The OCC identifies Strategic risk in the following areas . . .

Home

© 2018 – FinPro, Inc.

• Re asserts the definitive guidance contained in the FDIC Pocket Guide for Directors

• Duty of loyalty and care

• Comply with federal and state statutes, rules and regulations

• Added clarification

ü Not involved in day to day operations

ü Establish acceptable risk levels

ü Ensure that policies, procedures and practices are in place

ü Monitor Senior management and business operations

• Risk culture

• Ethical culture

61

The FDIC followed suit and issued a Supervisory Insights dedicated entirely to Corporate Governance . . .

Home

© 2018 – FinPro, Inc.

• Select and retain competent management, talent development and succession planning

• Supervise management

• Understand the bank’s risk profile

• Set risk objectives and parameters

• Establish, with management, long and short term business objectives

• Strategic planning

• Maintain independence

• Adopt operating policies

• Monitor operations and oversee business performance

• Provide for independent reviews

• Heed supervisory reports

• Keep informed, and

• Ensure meeting community’s credit needs

62

The FDIC Pocket Guide for Directors . . .

Talent ManagementERMStrategic PlanningCorporate Governance

Home

© 2018 – FinPro, Inc.

• Set clear, aligned, and consistent direction regarding the firm’s strategy and risk tolerance

• Actively manage information flow and Board discussions

• Hold senior management accountable

• Support the independence and stature of independent risk management and internal audit

• Maintain a capable board composition and governance structure

63

The Federal Reserve has also clarified Corporate Governance . . .

Home

© 2018 – FinPro, Inc.

To manage the risks that Corporate Governance brings, a comprehensive and integrated system is required . . .

64

Home

© 2018 – FinPro, Inc.

• New Jersey Bankers and FinPro have partnered to establish Director Certification Program

• Regulators want training tied to Bank risk priorities

ü FinPro will match training opportunities to Bank specific risk assessments

ü FinPro will match training to regulatory hot buttons

• Certification credits are established every year, typically 15 credits required

§ Each vehicle will provide a takeaway checklist

§ Custom training is done using bank specific data

§ Automated system tracks progress at:

- New Jersey Program level

- Bankwide level

- Individual Director level

65

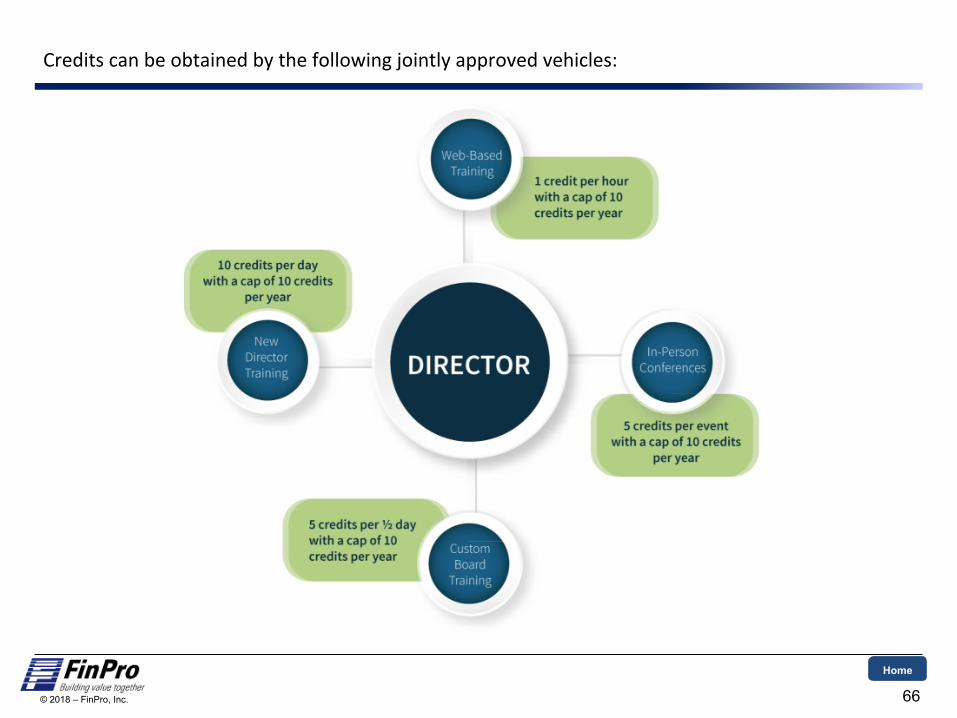

Good Corporate Governance demands ongoing training . . .

Home

© 2018 – FinPro, Inc. 66

Credits can be obtained by the following jointly approved vehicles:

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

8. Single Scenario Plans

9. Regulatory Constraints

10. Departmental Risk

11. Board Micromanagement

12. Human Resources

67

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

8. Multiple Stress Tested Scenarios

9. Market Opportunities

10. Integrated ERM

11. Effective Corporate Governance

12. Talent Management

Home

© 2018 – FinPro, Inc.

What is Talent Management . . .

Effective Talent Management is about

§ Performance Feedback

§ Employee Engagement

§ Effective Training

§ Succession Planning

Which results in the creation of value through

§ Attracting the RIGHT people

§ Retaining the RIGHT people

§ Promoting the RIGHT people

68

Home

© 2018 – FinPro, Inc.

The Matrix is also effective in determining which employees to retain . . .

4. Strong Technician 2. Strong Performer 1. Outstanding

7. Adequate Performer 5. Solid Performer 3. Future Star

9. Poor Performer 8. Under Performer 6. Raw Talent

69

Per

form

ance

Potential

Home

© 2018 – FinPro, Inc.

“Traditional” Model

1. Historical Perspective

2. Asset Growth

3. Transactions

4. Products

5. Advertising

6. Brick and Mortar

7. SILO’ s

8. Single Scenario Plans

9. Regulatory Constraints

10. Departmental Risk Assessments

11. Board Micromanagement

12. Human Resources

13. People Intensive

70

FinPro 2020 Model

1. Forward Looking

2. Value Creation

3. Relationships

4. Customers

5. Targeted Marketing

6. Targeted Delivery

7. Integrated Organizations

8. Multiple Stress Tested Scenarios

9. Market Opportunities

10. Integrated ERM

11. Effective Corporate Governance

12. Talent Management

13. Digital Intensive

Home

© 2018 – FinPro, Inc. 71

Financial Institutions must remember that this iteration is continued evolution as opposed to revolution . . .

Early 20th Century

1970s 1990s Now

Centered around regulated financial institutions

Non-financialnon-regulated companies

Home

© 2018 – FinPro, Inc.

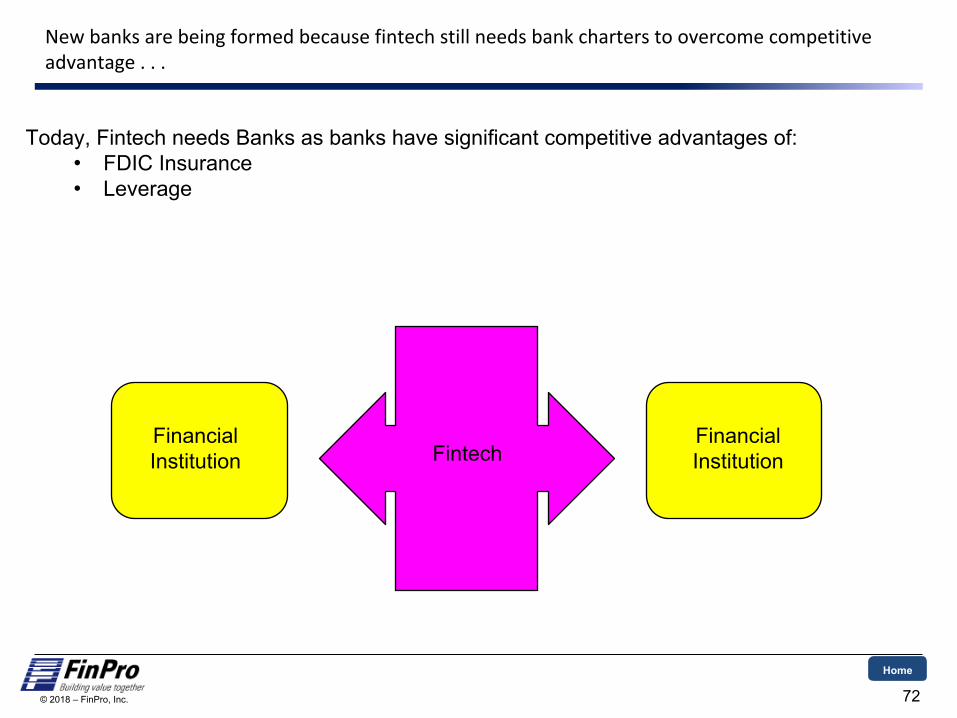

New banks are being formed because fintech still needs bank charters to overcome competitive advantage . . .

72

FintechFinancial Institution

Financial Institution

Today, Fintech needs Banks as banks have significant competitive advantages of:• FDIC Insurance• Leverage

Home

© 2018 – FinPro, Inc.

73

We must change from the traditional model to ensure future success . . .

ü Changing Demographics

ü Changing Technology

ü Continued Regulatory /

Compliance Burden

ü Unstable Economic Rate

Environment

ü New Under Regulated Non-

bank Competition

ü Under Educated and

Under Trained Staff

ü Single Analysis Engine

ü Individual Variable and

Total Scenario Stress

Testing

ü Corporate Governance

ü Board Training

ü Customer Segmentation

ü Talent Management

ü New Delivery Channels

ü Risk Management

ü Regulatory Expertise

ü Improve Delivery

• Human Branches

• Digital Branches

• Brick & Mortar

ü Focus on customers (not

products)

ü Relationship – not

transactions

ü Talent Management

• Few employees

• More expensive

• Better Educated

ü Creating the right brand in a

highly commoditized world

The Face of Community Banking is Changing . . .

Each Bank will Need the Following Tools . . .

So, To Create Value . . .

Home

© 2018 – FinPro, Inc. 74

Some ways in which Directors can determine how they are doing?

1. Are we spending our time on strategy and “what-ifs” or are we misfocused on history?2. Are we doing the seven things to build value?3. Have we built the spider web of relationships for our Board and Senior Officers?4. Have we identified our target customers? Are they in our markets? Are we measuring and

benchmarking correctly?5. Are we still brick and mortar dependent? How effective are our digital delivery channels?6. Are we still structured in a SILO format? 7. Does our budget and plan include multiple scenarios presented in a decision tree format?8. Do we CAMELS + self assess? Are we current in our regulatory understanding?9. Do we know our prioritized risks? Do we have mitigation plans in effect?10. Do we have an integrated sound Corporate Governance system? 11. How do we manage our people? Do we train for succession or simply have a chart?12. Do we have the data we need to analyze our Company on a go forward basis?

Home

© 2018 – FinPro, Inc.

For more information, please contact

Donald Musso, President

Scott Hein, Director

Emeritus Professor of Finance –Texas Tech University

75

© 2016 – FinPro, Inc. 76

Thank you for participating in today’s conference . . .

For more information, please contact us directly at:

Donald Musso, PresidentScott Polakoff, Executive Vice President

Scott Hein, DirectorTim Koch, Director

[email protected]@finpro.us