COELUROSAURIA - University of Maryland, Department of Geology

Upload

ambrose-lambertCategory

view

215download

2

Bureau of Economic Geology, The University of Texas at Austin

Oil & Gas InvestmentUSEIA, April 7-8, 2009

©CEE-UT, 2

Dr. Michelle Michot Foss, CEE-UT

Trends Drivers

• Upstream cost structures and margins relative to financing

• Demand-side pricing policies by governments (oil)• Impact of financial markets• Resources and opportunities – “frontier” oil• “Frontier” natural gas• Cross-commodity pricing (fuel competition) – the

challenge of building value for nat gas• Climate• Investment trends – invest in what you know

©CEE-UT, 3

Dr. Michelle Michot Foss, CEE-UT

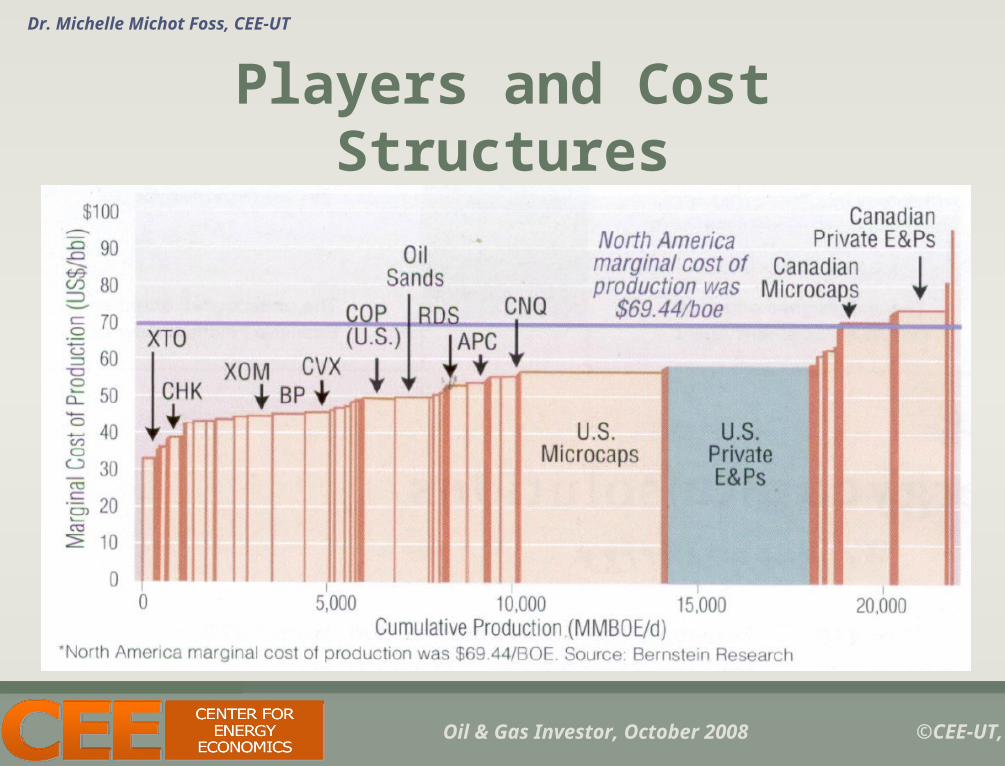

Players and Cost Structures

Oil & Gas Investor, October 2008

©CEE-UT, 4

Dr. Michelle Michot Foss, CEE-UT

ONGC

PetroBangla

OGDCL

QP KPC

Average NOC

Gazprom

ECOPETROL

StatoilHydro

PTT

GDF

Sonatrach

PETROBRAS

PDVSA

PEMEX

PetronasSinopec

PetroChina

CNOOC

Rosneft

Kazmun-aigas

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

45 50 55 60 65 70 75 80 85 90

Average All Scores

Re

se

rve

Re

pla

ce

me

nt

Ra

te (

BO

E,

%)

AverageEast Asia and PacificEurope and Central AsiaLatin America and CaribbeanMiddle East and North AfricaSouth AsiaSub-Saharan Africa

Improvements in NOCs’ reserve replacement rate are supported by improvements in governance, more effective and stable alliances between NOCs and IOCs, sound competitive frameworks, and progressive fiscal regimes…

A Citizen’s Guide to NOCs, CEE and World Bank, www.worldbank.org/noc

©CEE-UT, 5

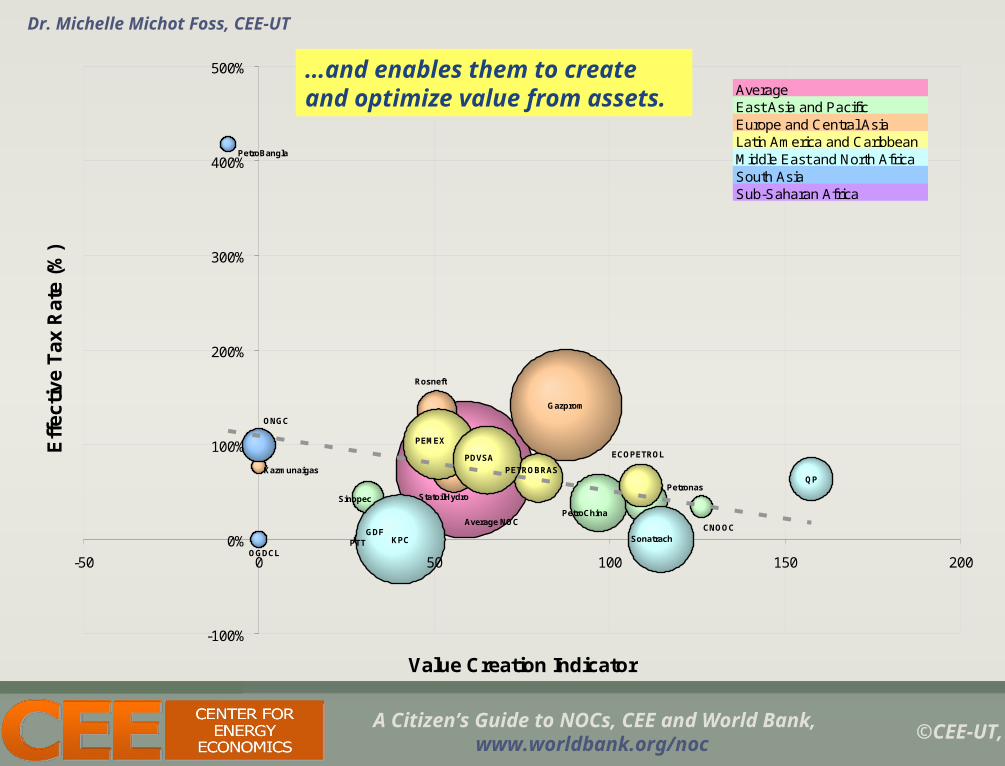

Dr. Michelle Michot Foss, CEE-UT

ONGC

PetroBangla

OGDCL

QP

KPC

Average NOC

Gazprom

ECOPETROL

StatoilHydro

PTTGDF

Sonatrach

PETROBRAS

PDVSA

PEMEX

PetronasSinopec

PetroChina

CNOOC

Rosneft

Kazmunaigas

-100%

0%

100%

200%

300%

400%

500%

-50 0 50 100 150 200

Value Creation Indicator

Eff

ec

tiv

e T

ax

Ra

te (

%)

AverageEast Asia and PacificEurope and Central AsiaLatin America and CaribbeanMiddle East and North AfricaSouth AsiaSub-Saharan Africa

…and enables them to create and optimize value from assets.

A Citizen’s Guide to NOCs, CEE and World Bank, www.worldbank.org/noc

©CEE-UT, 6

Dr. Michelle Michot Foss, CEE-UT

A Citizen’s Guide to NOCs, CEE and World Bank, www.worldbank.org/noc

©CEE-UT, 7

Dr. Michelle Michot Foss, CEE-UT

Non-Commercial PerformanceContributions by Type/Revenue (%)

24 316

23

58

-4

31

16

22

-4-20

0

20

40

60

80

100

StatHydro Petrobras Sinopec Petrochina Pemex

Taxes, Roys., Bonuses Price Subsidies

Direct Social Expenses Excess Labor Cost

CEE-UT

©CEE-UT, 8

Dr. Michelle Michot Foss, CEE-UT

IEA, NYMEX

Oil Demand Growth by Region, 2006-2008 (YTD)

-1.2-1

-0.8-0.6-0.4-0.2

00.20.40.60.8

11.21.4

China Middle East Other non-OECD Asia

OECD Rest of World World

mm

b/d

2006 2007 2008 YTD

WTI Price (Real), 2006-2008 (YTD)

0

5

10

15

20

25

30

35

40

WTI Price (Real)m

mb

/d

2006 2007 2008 YTD

Subsidies and Demand

©CEE-UT, 9

Dr. Michelle Michot Foss, CEE-UT

Not All Opportunities are the Same

From Holditch, 2005, “Statistical Correlations in Tight Gas Sands”, American Association of Petroleum Geologists (AAPG) Hedberg Conference Proceedings. http://www.searchanddiscovery.net/documents/abstracts/2005hedberg_vail/abstracts/extended/holditch01/holditch01.htm

©CEE-UT, 10

Dr. Michelle Michot Foss, CEE-UT

Electron Imagery of Barnett Fractures

Gale, J. F. W., Reed, R. M., and Holder, Jon, 2007, Natural fractures in the Barnett Shale and their importance for hydraulic fracture treatments: AAPG Bulletin, v. 91, no. 4, p. 603–622.

©CEE-UT, 11

Dr. Michelle Michot Foss, CEE-UT

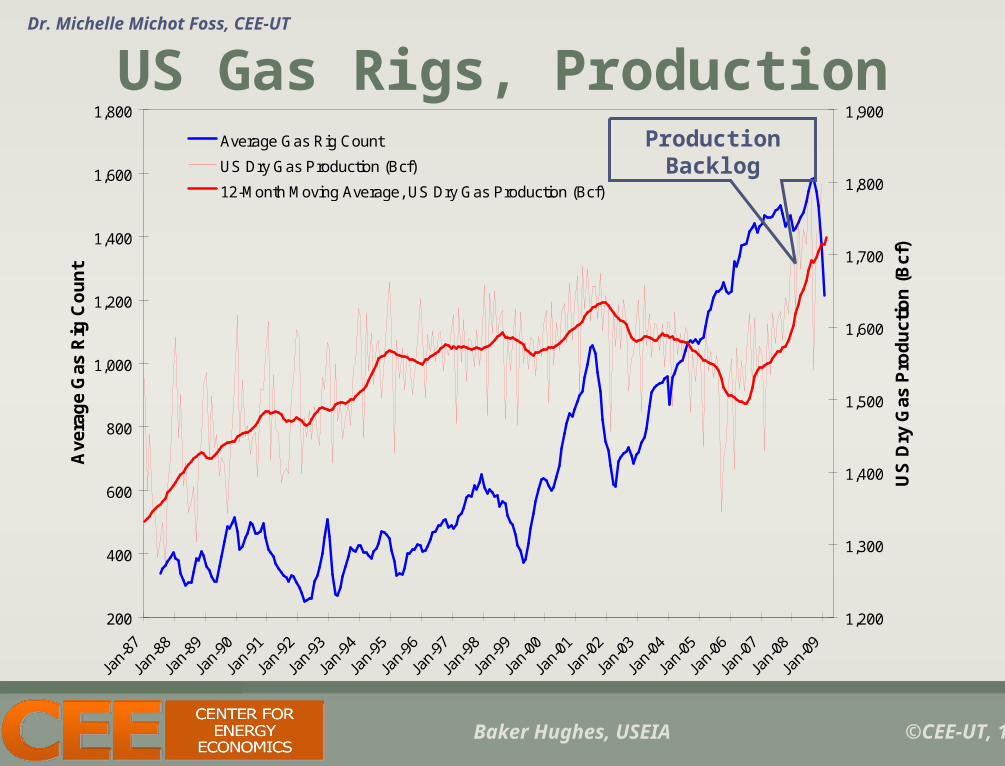

US Gas Rigs, Production

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Ave

rag

e G

as R

ig C

ou

nt

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

US

Dry

Gas

Pro

du

ctio

n (

Bcf

)

Average Gas Rig Count

US Dry Gas Production (Bcf)

12-Month Moving Average, US Dry Gas Production (Bcf)

Baker Hughes, USEIA

Production Backlog

©CEE-UT, 12

Dr. Michelle Michot Foss, CEE-UT

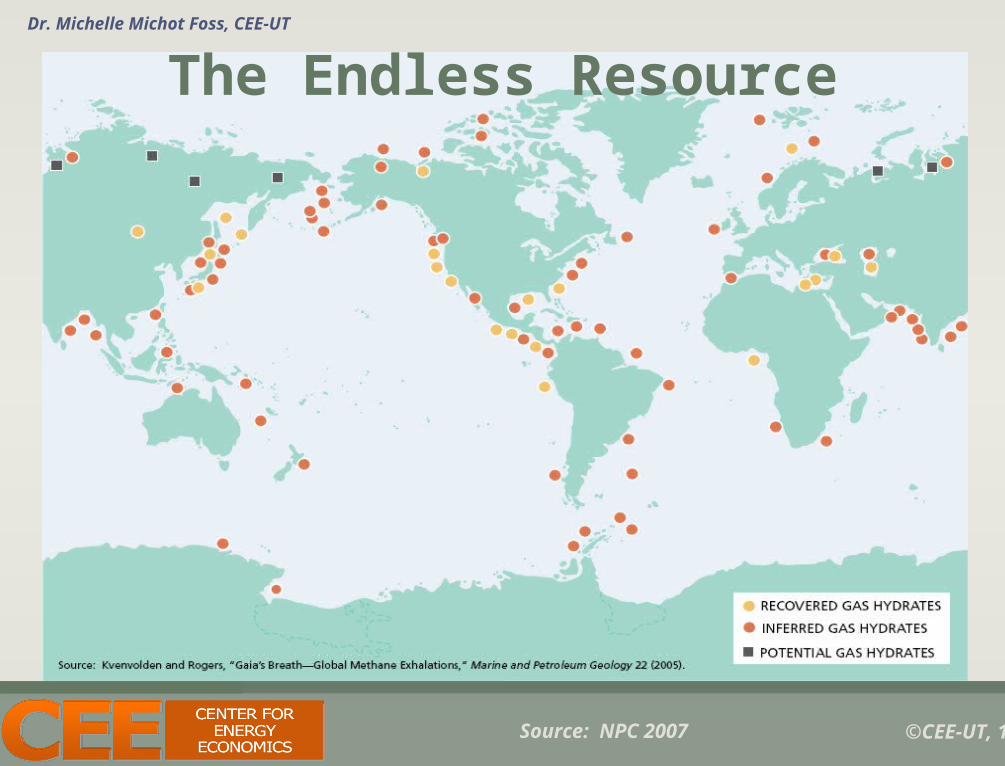

Source: NPC 2007

The Endless Resource

©CEE-UT, 13

Dr. Michelle Michot Foss, CEE-UT

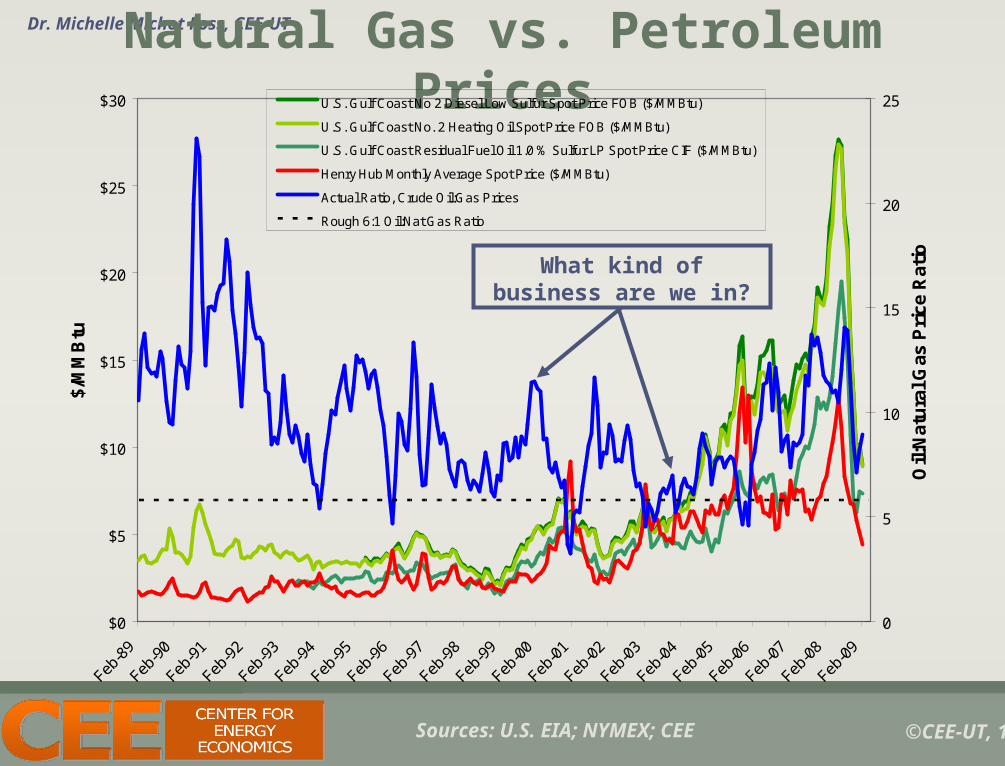

Natural Gas vs. Petroleum Prices

Sources: U.S. EIA; NYMEX; CEE

$0

$5

$10

$15

$20

$25

$30

$/M

MB

tu

0

5

10

15

20

25

Oil:

Nat

ura

l Gas

Pri

ce R

atio

U.S. Gulf Coast No 2 Diesel Low Sulfur Spot Price FOB ($/MMBtu)

U.S. Gulf Coast No. 2 Heating Oil Spot Price FOB ($/MMBtu)

U.S. Gulf Coast Residual Fuel Oil 1.0 % Sulfur LP Spot Price CIF ($/MMBtu)

Henry Hub Monthly Average Spot Price ($/MMBtu)

Actual Ratio, Crude Oil:Gas Prices

Rough 6:1 Oil:Nat Gas Ratio

What kind of business are we in?

©CEE-UT, 14

Dr. Michelle Michot Foss, CEE-UT

Public Acceptance: Sample LNG Projects in Same Region

1

2

3

4

5Safety/Security

Wetlands

Fisheries

Energy Costs

Roads

Taxes

Employment

Air Emissions

Property Value

Other/Intangibles

Immediate Site Community Waterway Community Local Community (City)

Greater Community (State) National Community (Federal) External Interest Group

1 - Perceived Benefit

3 - Indifferent

5 - Perceived Cost

1

2

3

4

5Safety/Security

Wetlands

Fisheries

Energy Costs

Roads

Taxes

Employment

Air Emissions

Property Value

Other/Intangibles

Immediate Site Community Waterway Community Local Community (City)

Greater Community (State) National Community (Federal) External Interest Group

1 - Perceived Benefit

3 - Indifferent

5 - Perceived Cost

What caused the differences?Onshore vs. Offshore?

Developer posture? Early dialogue?

Unlicensed Onshore Project

Licensed Offshore Project

Sources: CEE, Community and Economic Benefits of LNG, 2008

©CEE-UT, 15

Dr. Michelle Michot Foss, CEE-UT

Sample Projects in Different Regions

1

2

3

4

5Safety/Security

Wetlands

Fisheries

Energy Costs

Roads

Taxes

Employment

Air Emissions

Property Value

Other/Intangibles

Immediate Site Community Waterway Community Local Community (City)

Greater Community (State) National Community (Federal) External Interest Group

1 - Perceived Benefit3 - Indifferent5 - Perceived Cost

1

2

3

4

5Safety/Security

Wetlands

Fisheries

Energy Costs

Roads

Taxes

Employment

Air Emissions

Property Value

Other/Intangibles

Immediate Site Community Waterway Community Local Community (City)

Greater Community (State) National Community (Federal) External Interest Group

1 - Perceived Benefit

3 - Indifferent

5 - Perceived Cost

What caused the differences?Onshore vs. Offshore?

Developer posture? Early dialogue?

Unlicensed OnshoreProject

Licensed Onshore Project

Sources: CEE, Community and Economic Benefits of LNG, 2008

©CEE-UT, 16

Dr. Michelle Michot Foss, CEE-UT

Math Whiz

• Total annual CO2 emitted is 188 bn ton• 8bn is derived from human activity

– US produces 2 bn

• Net generation from US coal plants is ~170mm MWh– CO2 production is ~2,250 lbs/MWh, or 191mm tons

• The total atmosphere is 5 quadrillion tons– We would be removing 0.00000382% if all CO2 from US

coal-fired power gen was captured– We would be removing 0.00016% if all CO2 attributed

with human activity were captured or eliminated

©CEE-UT, 17

Dr. Michelle Michot Foss, CEE-UT

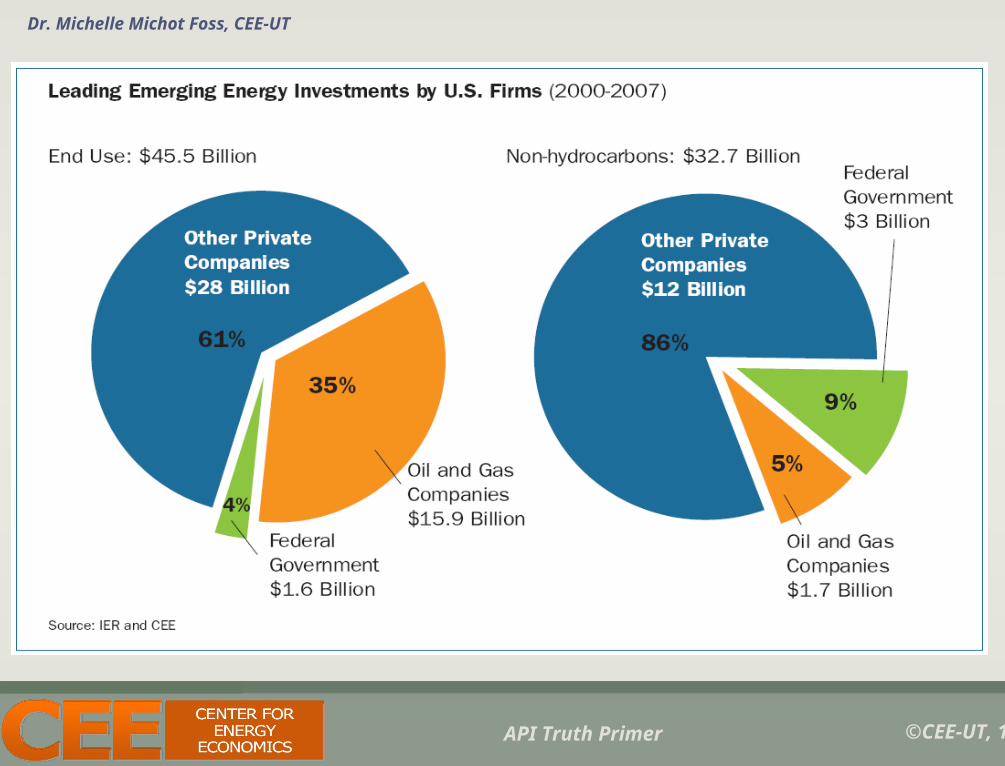

API Truth Primer

©CEE-UT, 18

Dr. Michelle Michot Foss, CEE-UT

API Truth Primer

©CEE-UT, 19

Dr. Michelle Michot Foss, CEE-UT

API Truth Primer

©CEE-UT, 20

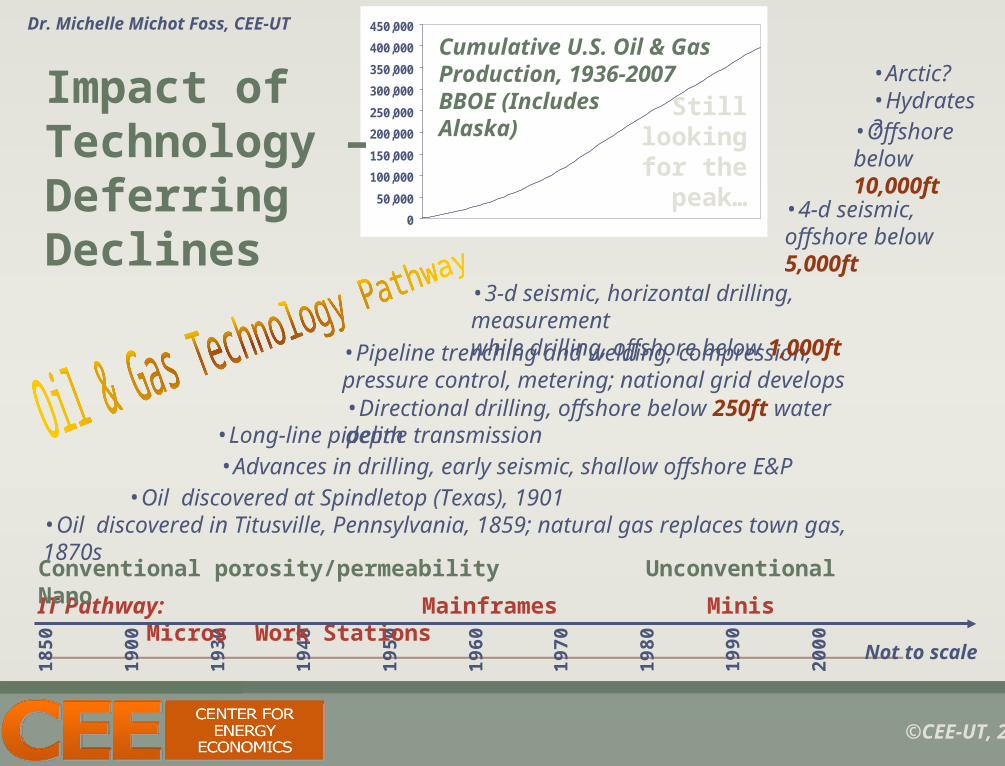

Dr. Michelle Michot Foss, CEE-UT18

50

190

0

193

0

194

0

195

0

196

0

197

0

198

0

199

0

200

0

•Oil discovered in Titusville, Pennsylvania, 1859; natural gas replaces town gas, 1870s

•Advances in drilling, early seismic, shallow offshore E&P

•Long-line pipeline transmission•Directional drilling, offshore below 250ft water depth

•Pipeline trenching and welding, compression,pressure control, metering; national grid develops

•3-d seismic, horizontal drilling, measurementwhile drilling, offshore below 1,000ft

IT Pathway: Mainframes Minis Micros Work Stations

•Offshore below10,000ft

•Oil discovered at Spindletop (Texas), 1901

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Impact of Technology – Deferring Declines

Cumulative U.S. Oil & GasProduction, 1936-2007BBOE (IncludesAlaska)

Not to scale

•Arctic?•Hydrates?

•4-d seismic, offshore below 5,000ft

Still looking for the peak…

Conventional porosity/permeability Unconventional Nano

©CEE-UT, 21

Dr. Michelle Michot Foss, CEE-UT

Center for Energy Economics

www.beg.utexas.edu/energyecon