ANNUAL INVESTOR CONFERENCE 2013 - RPG Life … INVESTOR CONFERENCE 2013 Presence in key sectors of...

30

21st May 2013, Mumbai ANNUAL INVESTOR CONFERENCE 2013

Transcript of ANNUAL INVESTOR CONFERENCE 2013 - RPG Life … INVESTOR CONFERENCE 2013 Presence in key sectors of...

21st May 2013, Mumbai

ANNUAL INVESTOR CONFERENCE 2013

Presence in key sectors of economy

TYRE

SPECIALITY

INFRASTRUCTURE

IT

$3 bn Global & diversified Indian business group

RPG Group

2

We shall be a leading Indian group with a focus on:

• Leadership in profitability and revenue growth in our chosen

business

• Being a customer - centric organization

• Being the most exciting workplace

Thus creating shareholder value

Group Vision…

3

• Auto penetration in semi-urban / rural area offers growth opportunities • India cost advantage can be taken to the world • Looking to grow in South Asia region

• Infrastructure - key to industrial and economic growth • Presence in developed as well as developing markets • Asset light model; proven execution track record

• Indian IT has remained a global powerhouse • Evolution from technology providers to strategic business partners to

drive future growth

Group - Long Term Strategy

4

Regional dominance in Tyre sector

Global ‘Power EPC’ to ‘Infrastructure EPC’ major

$1bn company by FY16 and profitable growth thereafter

• Building Scale profitably...

– Revenue grew by 20% while PAT grew by 17% CAGR in the last 4 years

– Group revenue doubled in last 4 years from Rs 8000cr to Rs 17000cr.

– Group operating profit at Rs 1200 cr

• Driven by...

– Investments... Over Rs 1,100 crs invested in capacity expansion in last 3 years.

– Strategic Acquisitions... Akibia & SAE Towers

– Partnerships... Set up strategic JVs in key markets such as Sri Lanka, Bangladesh to leverage local partner’s advantage, tie-up with tyre outsourcing partners in India

• Funding growth through internal accruals... Against a total investments & acquisitions of ~ Rs 1,900 Cr, outstanding debt against these investments of only ~ Rs 1,000 Crs as on date

• Global Player... ~42% revenues from global business.

• Attracting talent...with mix of skills, nationality and professional background

RPG Group: Journey so far

5

Trends and Opportunities

Export play:

• Asia becoming the manufacturing hub for Auto & Tyres; India Cost advantage

• Leverage global brand and distribution network in over 100 countries

Passenger segment play:

• Leadership in two-wheeler and UV segment

• Strong brand presence; high customer recall

Emerging markets play:

• Leader in Sri Lanka; replicate success in Bangladesh

Proven competitive advantages to lead higher growth & improve margins

CEAT

6

Overview and Strategy

Overview:

• 1.3 billion dollar enterprise with 55% plus business from international markets

• Footprints in 48 countries; 8 manufacturing facilities across India, Brazil and Mexico

• Global workforce; 23% non-Indians with diverse nationalities

Key strategic drivers:

• Maintain global leadership in Transmission business; expand construction activities in

Americas

• Build new businesses such as Power Systems, Railways and Water through partnerships;

expand internationally by leveraging transmission business global network

• SAE Towers acquisition is successful; generated $ 66mn EBITDA in 2.5 years against

acquisition value of $ 95 mn; plans to increase presence in poles segment

• Increase presence in EHV cables through new facility at Vadodara

• Entry into Wind and Solar EPC

• Opportunistic acquisitions

KEC

7

IT Sector – Highlights • The $ 100+ Bn industry is projected to grow at 13% for the

year as against the Global IT Industry growth of about 6%

• Strategic Imperatives for IT Service Providers

– End to End Solutions

– New trend areas including Cloud, Mobility, Social Media and Analytics

– Non-Linear Play

ZENSAR: Focus areas for FY11- Fy13 • Integrated ‘Application – Infrastructure management’ solution with acquisition of Akibia

• Structured the organization with focus on key Verticals

• Move from Time and Material to Managed Contracts

Way forward • Strong vertical propositions and arrowheads in focus verticals

• Focus on Larger Deals

• Focus on expanding ‘Fortune 1000’ Customer base

ZENSAR

8

IT Sector and Way forward

Speciality

9

Business Update

RPG Life sciences

• Biotech - Turnaround during the year- Growth in product yields & higher sales in

India & LATAM markets - 72% growth in top-line and a positive PBT

• Formulation Business (Domestic) - Focus brands to drive growth

• Business affected by certification issues. Now resolved.

Harrisons Malayalam Limited

• Tea - Modernisation of factories to exploit both export and domestic demand; re-

plantation to improve yield per hectare

• Rubber - Extensive re-plantation with most modern clones of high yielding

potential; plan to produce ‘value added rubber’ using captive latex production

Raychem RPG (Unlisted)

• 50:50 JV of TE Connectivity (formerly Tyco Electronics), USA and RPG Group, India

• A multi-product & solutions company catering to Energy (T&D), Telecom, Oil & Gas

• Investing in R&D to create a pipeline of high-tech products

• Turnover of over Rs 600cr in FY13

• Core values: Respect and value people; ‘Empowerment’ key to unleash individual potential

• Forward looking and quick to adopt cutting edge people practices:

– Balanced score card to promote performance oriented culture

– 360o feedback for self development

– Elaborate career and succession planning

– Young executive board as a shadow board in all companies

– Self managed teams at all new factories

• Amongst the best employee satisfaction scores

People practices as a differentiating strategy

Able to attract talent…with diverse skills & nationalities

10

PROFITABLE GROWTH IN UNCERTAIN TIMES

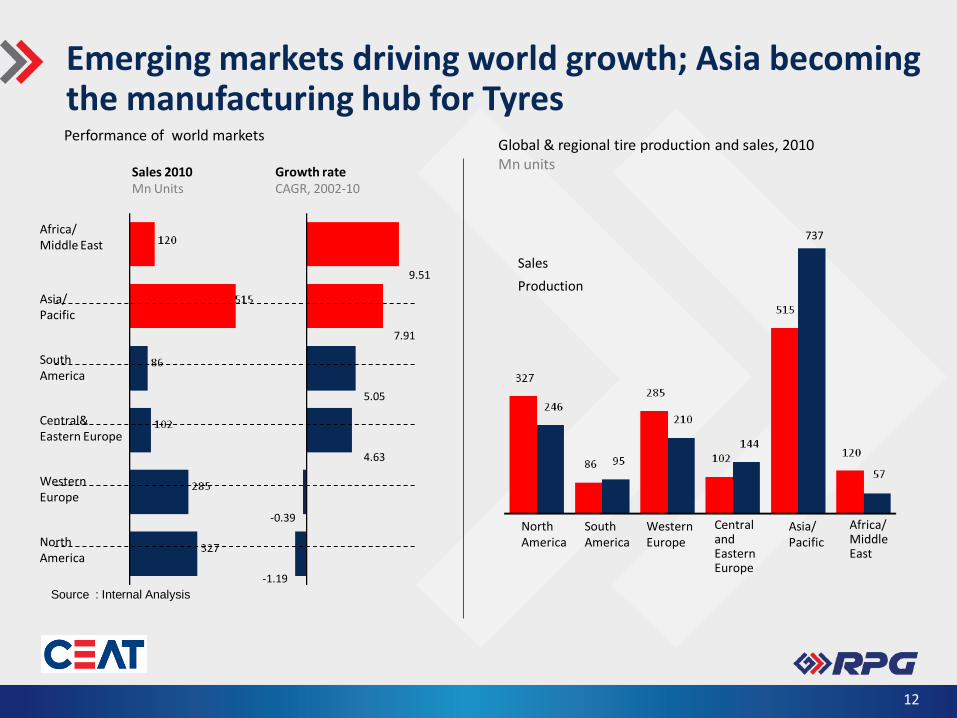

Emerging markets driving world growth; Asia becoming the manufacturing hub for Tyres Performance of world markets

-1.19

-0.39

4.63

5.05

7.91

9.51

North America

Western Europe

Central& Eastern Europe

South America

Asia/ Pacific

Africa/ Middle East

Sales 2010 Mn Units

Growth rate CAGR, 2002-10

Africa/ Middle East

Asia/ Pacific

Central and Eastern Europe

Western Europe

South America

North America

Production

Sales

Global & regional tire production and sales, 2010 Mn units

737

12

Source : Internal Analysis

India: Product mix is slowly changing with a clear shift towards non-truck segments; however T&B still ~50% of the market

4

11

6

1

8

56

6

1

11

50

FY11

36,900

2 4

11

6 1

11

51

FY10

33,705

2 4

11

6

4 2

28,580

FY08

54

9

1

7

10

4 2

28,615

FY09

55

9

1

57

11

FY07

26,730

1

8

2

6

10

OTR

Industrial

7 LCV

Jeep

Passenger Cars

2/3 wheelers

Truck Bus

FY12

38,520

4

1

9

2

55

2

25,110

4

11

FY06

Tractor overall

12%

4%

7%

5%

14%

9%

10%

7%

Sales growth and split of tyres – All India ` crore, %

Historical CAGR

13

Source : Internal Analysis

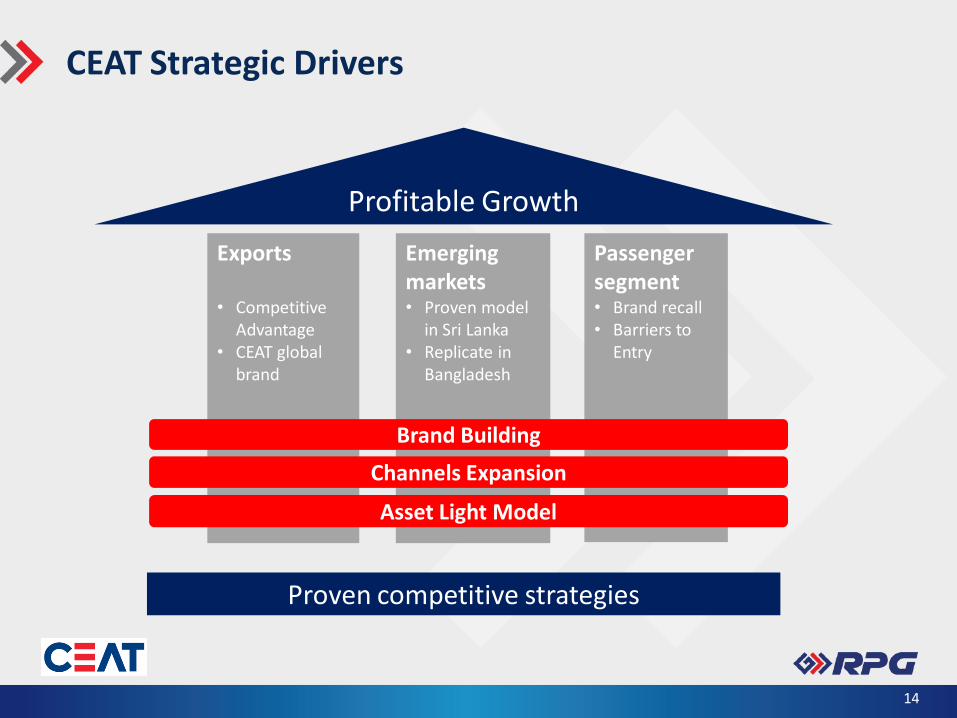

CEAT Strategic Drivers

Profitable Growth

Exports • Competitive

Advantage • CEAT global

brand

Emerging markets • Proven model

in Sri Lanka • Replicate in

Bangladesh

Passenger segment • Brand recall • Barriers to

Entry

Asset Light Model

Channels Expansion

Brand Building

Proven competitive strategies

14

A BILLION DOLLAR GLOBAL INFRASTRUCTURE EPC MAJOR

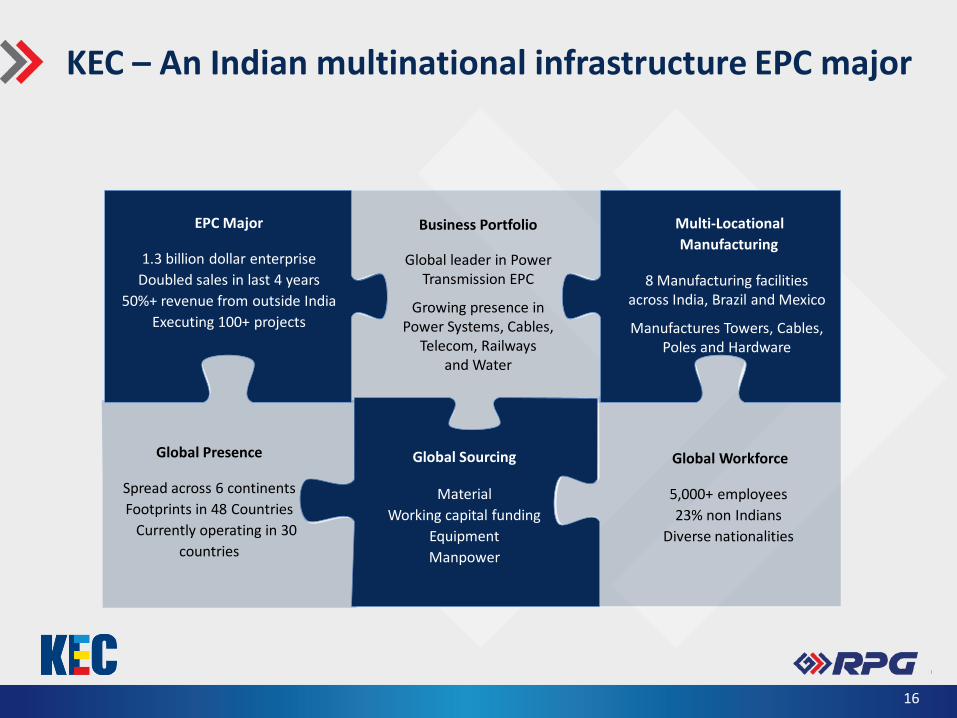

KEC – An Indian multinational infrastructure EPC major

Multi-Locational

Manufacturing

8 Manufacturing facilities across India, Brazil and Mexico

Manufactures Towers, Cables, Poles and Hardware

EPC Major

1.3 billion dollar enterprise

Doubled sales in last 4 years

50%+ revenue from outside India

Executing 100+ projects

Global Presence

Spread across 6 continents

Footprints in 48 Countries

Currently operating in 30

countries

Global Workforce

5,000+ employees

23% non Indians

Diverse nationalities

Business Portfolio

Global leader in Power Transmission EPC

Growing presence in Power Systems, Cables,

Telecom, Railways and Water

Global Sourcing

Material

Working capital funding

Equipment

Manpower

16

Growth Enablers - Infrastructure sector

Ability of citizens to pay

Funding availability

Multilateral agencies funding (JICA, AfDB, EBRD, World Bank, ADB etc.)

Increasing private sector participation

FDI

Cost of capital

Government Policies

Land acquisition and Right of Way

Environmental clearances

Payment security of PPP projects

Financial health of distribution companies

Stable tax policies

Infrastructure planning

Growing middle class population

Focus on better quality of life

Growth Enablers -

Infrastructure Sector

17

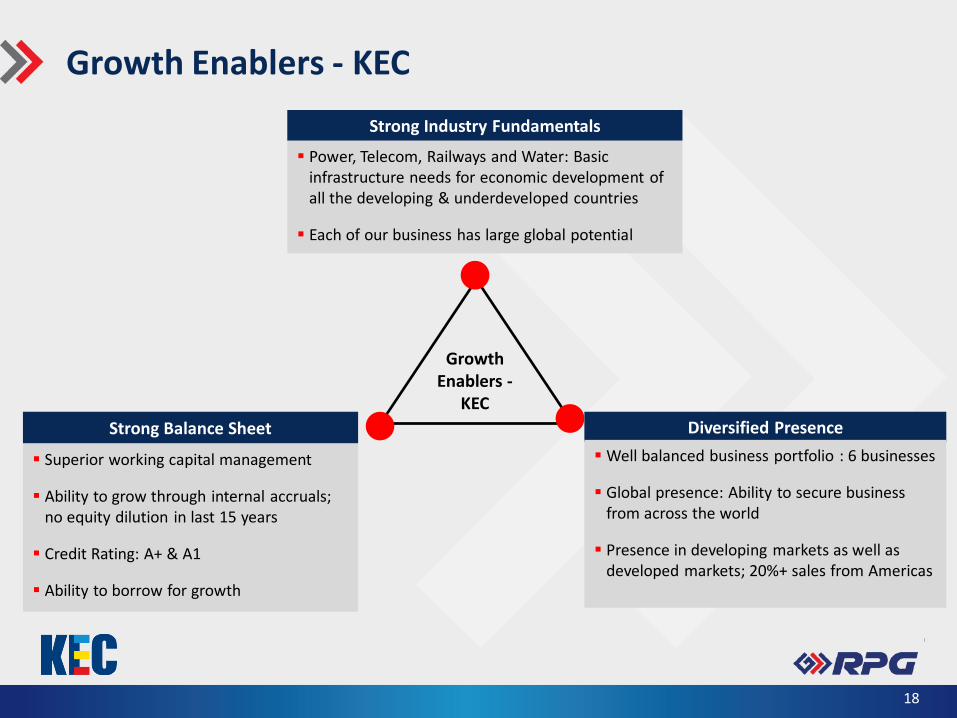

Growth Enablers - KEC

Strong Industry Fundamentals

Diversified Presence

Well balanced business portfolio : 6 businesses

Global presence: Ability to secure business from across the world

Presence in developing markets as well as developed markets; 20%+ sales from Americas

Strong Balance Sheet

Superior working capital management

Ability to grow through internal accruals; no equity dilution in last 15 years

Credit Rating: A+ & A1

Ability to borrow for growth

Power, Telecom, Railways and Water: Basic infrastructure needs for economic development of all the developing & underdeveloped countries

Each of our business has large global potential

Growth Enablers -

KEC

18

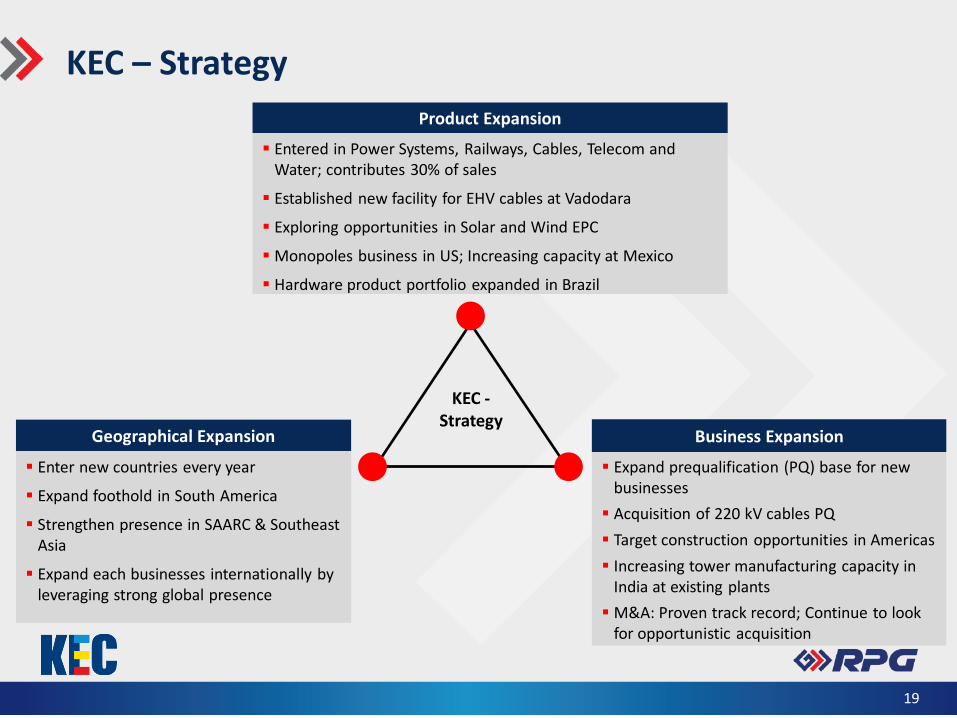

KEC – Strategy

Expand prequalification (PQ) base for new businesses

Acquisition of 220 kV cables PQ

Target construction opportunities in Americas

Increasing tower manufacturing capacity in India at existing plants

M&A: Proven track record; Continue to look for opportunistic acquisition

Product Expansion

Business Expansion Geographical Expansion

Enter new countries every year

Expand foothold in South America

Strengthen presence in SAARC & Southeast Asia

Expand each businesses internationally by leveraging strong global presence

Entered in Power Systems, Railways, Cables, Telecom and Water; contributes 30% of sales

Established new facility for EHV cables at Vadodara

Exploring opportunities in Solar and Wind EPC

Monopoles business in US; Increasing capacity at Mexico

Hardware product portfolio expanded in Brazil

KEC - Strategy

19

To sum up..

KEC has all the key enablers and strategies in place,

To capture the growth opportunities

In a Multi – Billion Infrastructure Sector

20

STRONG FOCUS ON OUTCOME LED PROPOSITIONS

ZENSAR at a glance

22% CAGR for Revenue and PAT in the last 5 years

2115* crores FY13 Revenues

175* crores FY13 PAT

6500+ Employees

290+ Active Customers

20+ Global Locations

#13 in NASSCOM Top Indian IT Providers

2 Case Studies by HBS** on ZENSAR

22

* In INR

** Harvard Business School

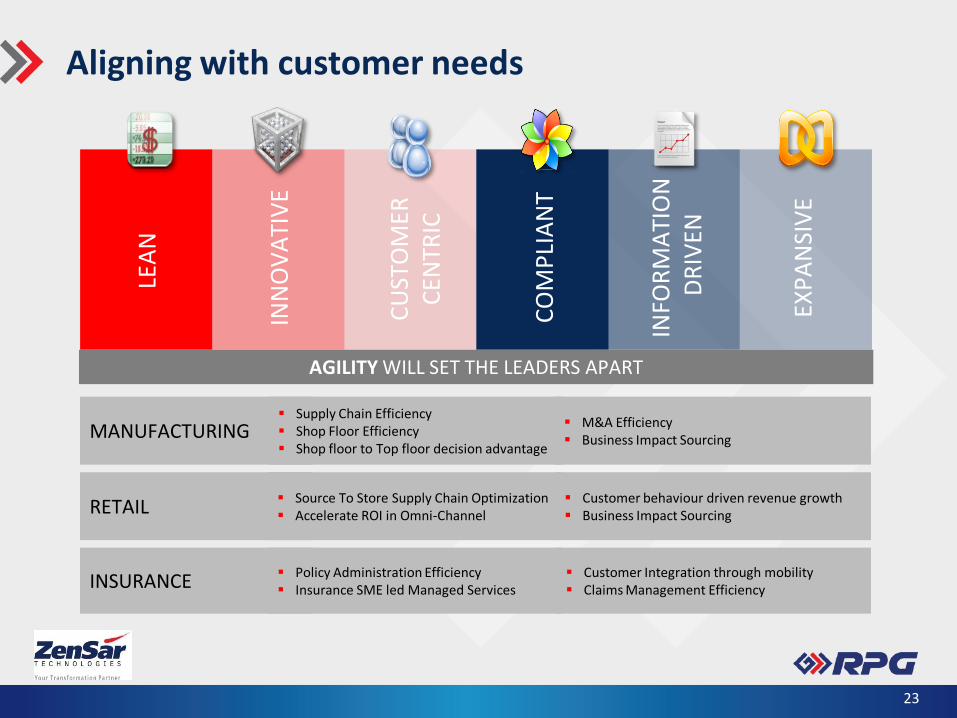

Aligning with customer needs

EX

PA

NSI

VE

LEA

N

C

UST

OM

ER

CEN

TRIC

IN

FOR

MA

TIO

N

DR

IVEN

C

OM

PLI

AN

T

IN

NO

VA

TIV

E

AGILITY WILL SET THE LEADERS APART

MANUFACTURING

RETAIL

INSURANCE

Supply Chain Efficiency Shop Floor Efficiency Shop floor to Top floor decision advantage

M&A Efficiency Business Impact Sourcing

Source To Store Supply Chain Optimization Accelerate ROI in Omni-Channel

Customer behaviour driven revenue growth Business Impact Sourcing

Policy Administration Efficiency Insurance SME led Managed Services

Customer Integration through mobility Claims Management Efficiency

23

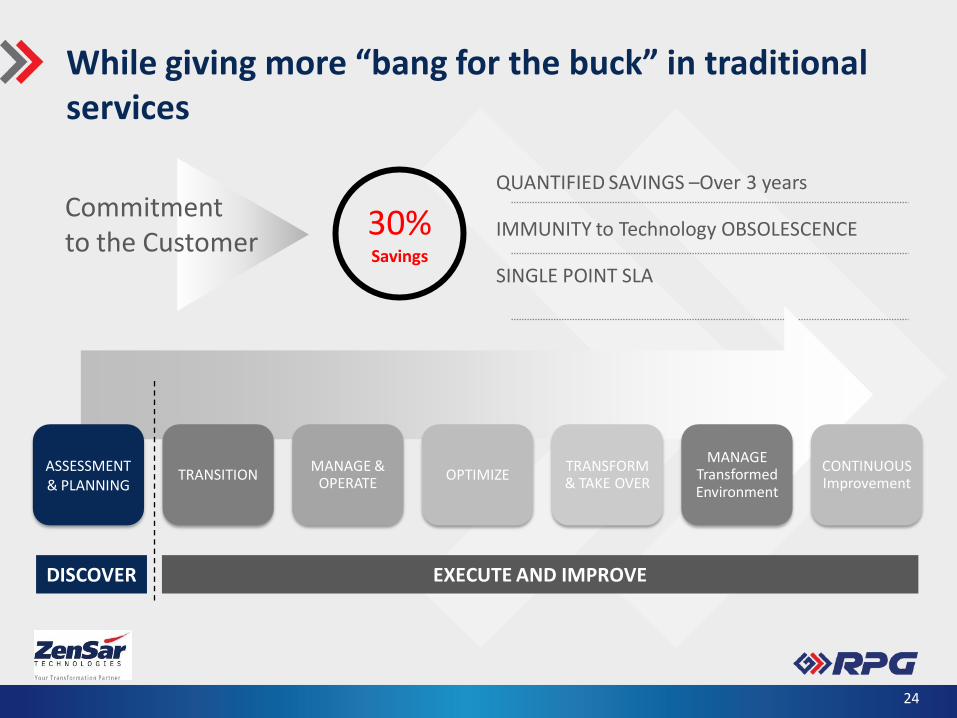

While giving more “bang for the buck” in traditional services

QUANTIFIED SAVINGS –Over 3 years

IMMUNITY to Technology OBSOLESCENCE

SINGLE POINT SLA

Commitment to the Customer

ASSESSMENT & PLANNING

TRANSITION MANAGE &

OPERATE OPTIMIZE

TRANSFORM & TAKE OVER

MANAGE Transformed Environment

CONTINUOUS Improvement

DISCOVER EXECUTE AND IMPROVE

30% Savings

24

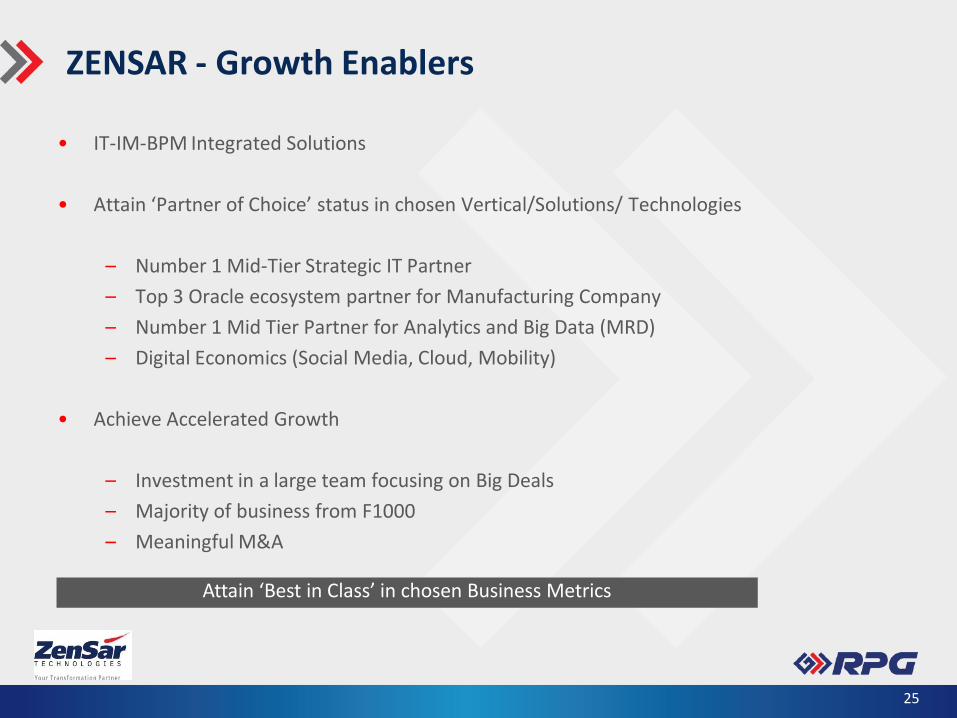

ZENSAR - Growth Enablers

• IT-IM-BPM Integrated Solutions

• Attain ‘Partner of Choice’ status in chosen Vertical/Solutions/ Technologies

– Number 1 Mid-Tier Strategic IT Partner

– Top 3 Oracle ecosystem partner for Manufacturing Company

– Number 1 Mid Tier Partner for Analytics and Big Data (MRD)

– Digital Economics (Social Media, Cloud, Mobility)

• Achieve Accelerated Growth

– Investment in a large team focusing on Big Deals

– Majority of business from F1000

– Meaningful M&A

25

Attain ‘Best in Class’ in chosen Business Metrics

ZENSAR - Solution Portfolıo

CONSULTING

MA

NU

FAC

TUR

ING

RET

AIL

BA

NK

ING

AN

D

FIN

AN

CIA

L SE

RV

ICES

INSU

RA

NC

E

HEA

LTH

CA

RE

INFRASTRUCTURE MANAGEMENT

BUSINESS PROCESS MANAGEMENT

APPLICATION MANAGEMENT

MANAGED SOURCING

Strong presence across services Acquisitions in white spaces SAP,

Cloud, PES, IM Focus on Business Outcomes

Focus on domain capabilities and outcome led models for business

Process and Business Consulting Solutions

26

RPG LIFE SCIENCES LIMITED

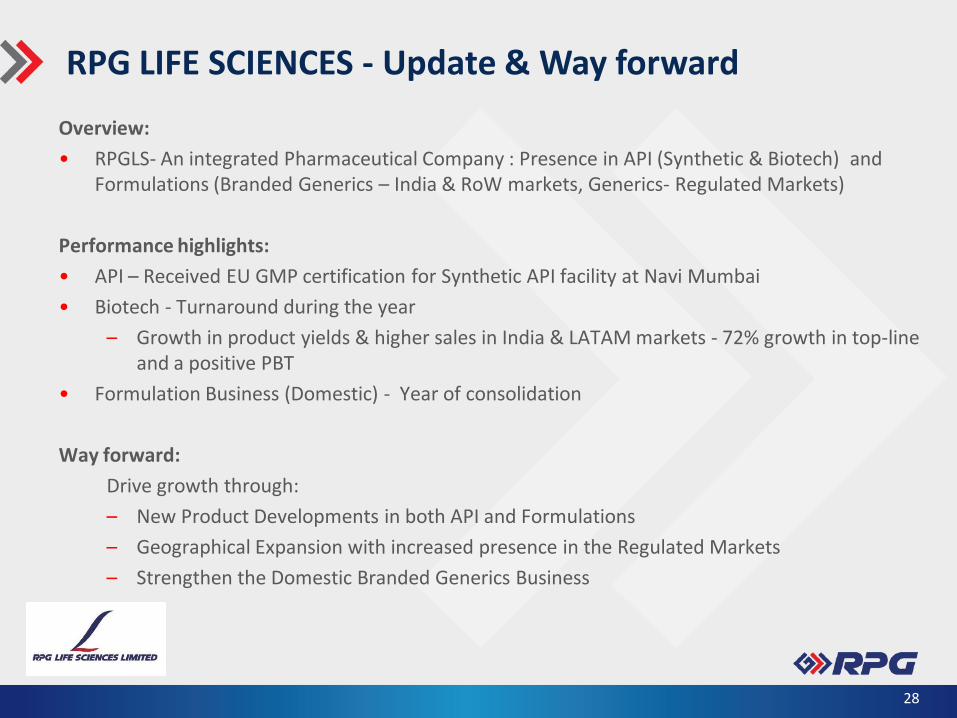

RPG LIFE SCIENCES - Update & Way forward

Overview:

• RPGLS- An integrated Pharmaceutical Company : Presence in API (Synthetic & Biotech) and Formulations (Branded Generics – India & RoW markets, Generics- Regulated Markets)

Performance highlights:

• API – Received EU GMP certification for Synthetic API facility at Navi Mumbai

• Biotech - Turnaround during the year

– Growth in product yields & higher sales in India & LATAM markets - 72% growth in top-line and a positive PBT

• Formulation Business (Domestic) - Year of consolidation

Way forward:

Drive growth through:

– New Product Developments in both API and Formulations

– Geographical Expansion with increased presence in the Regulated Markets

– Strengthen the Domestic Branded Generics Business

28

Q

29

& A

Y O U

30

T H A N K

![2012.06 Credit Suisse Investor Conference(中文版) [相容模式]](https://static.fdocument.pub/doc/165x107/619c21a39caf01761d051eb3/201206-credit-suisse-investor-conference.jpg)