AMICA PROPERTY AND CASUALTY INSURANCE COMPANY P&… · Amica Property and Casualty Insurance...

26

Report on Examination of AMICA PROPERTY AND CASUALTY INSURANCE COMPANY Lincoln, Rhode Island as of December 31, 2014 State of Rhode Island and Providence Plantations Department of Business Regulation Insurance Division

Transcript of AMICA PROPERTY AND CASUALTY INSURANCE COMPANY P&… · Amica Property and Casualty Insurance...

Report on Examination

of

AMICA PROPERTY AND CASUALTY INSURANCE COMPANY

Lincoln, Rhode Island

as of

December 31, 2014

State of Rhode Island and Providence Plantations

Department of Business Regulation

Insurance Division

TABLE OF CONTENTS

Page

SALUTATION ………………………………………………………….…………… 1

SCOPE OF EXAMINATION ……………………………………………………….. 2

COMPANY HISTORY ……..…………………………………………….…………. 3

MANAGEMENT AND CONTROL ………………….……………..…………….… 4

Shareholders………………………………………………………….……..… 4

Board of Directors …………………………………………………………… 5

Committees ………………………………………………………….……….. 7

Officers …………………………………………………………….………… 7

Organizational Structure……………………………………………………… 8

Inter-Company Agreements..…………………………………………...……. 10

TERRITORY AND PLAN OF OPERATION ……………………………………… 12

REINSURANCE …………………………………………………………………….. 13

FINANCIAL STATEMENTS ……………………………………………………….. 14

Comparative Statement of Assets, Liabilities, Surplus and Other Funds……. 15

Statement of Income……………… ……………………………………….... 16

Capital and Surplus Account ……………………………………………….... 17

Reconciliation of Capital and Surplus ……………………………………….. 18

Analysis of Examination Adjustments ………………………………………. 19

ASSETS ……………………………………………………………………………… 20

Bonds ………………………………………………………………………… 20

LIABILITIES ………………………………………………………………………… 21

Losses ……….……………………………………………………………….. 21

Loss Adjustment Expenses …..………..……………………………………... 21

CAPITAL AND SURPLUS.……………………………………………………...…. 22

SUBSEQUENT EVENTS ……………………………….………………………….. 22

CONCLUSION ………………………………………………………………………. 23

1

February 25, 2016

Ms. Elizabeth Kelleher Dwyer

Deputy Director and Superintendent of Banking and Insurance

State of Rhode Island and Providence Plantations

Department of Business Regulation

1511 Pontiac Avenue, Bldg. 69-2

Cranston, Rhode Island 02920

Dear Superintendent Dwyer:

In accordance with your instructions and pursuant to Chapters 13.1 and 35 of Title 27 of the

General Laws of the State of Rhode Island, an examination has been made as of

December 31, 2014, of the financial condition and affairs of

AMICA PROPERTY AND CASUALTY INSURANCE COMPANY

at its home office located at 100 Amica Way, Lincoln, Rhode Island. The report of such

examination is herewith submitted.

Amica Property and Casualty Insurance Company, hereinafter referred to as “Amica P&C” or

the “Company” was previously examined as of December 31, 2010. Both the current and prior

examinations have been conducted by Insurance Division of the State of Rhode Island

(“Insurance Division”).

2

SCOPE OF EXAMINATION

The current examination covered the four-year period of January 1, 2011 through

December 31, 2014 and was performed in compliance with the above mentioned sections of

the General Laws of the State of Rhode Island, as amended. We conducted our examination

in accordance with the NAIC Financial Condition Examiners Handbook. The Handbook

requires that we plan and perform the examination to evaluate the financial condition, assess

corporate governance, identify current and prospective risks of the company and evaluate

system controls and procedures used to mitigate those risks. An examination also includes

identifying and evaluating significant risks that could cause an insurer’s surplus to be

materially misstated both currently and prospectively. All accounts and activities of the

company were considered in accordance with the risk-focused examination process. This may

include assessing significant estimates made by management and evaluating management’s

compliance with Statutory Accounting Principles. The examination does not attest to the fair

presentation of the financial statements included herein. If, during the course of the

examination an adjustment is identified, the impact of such adjustment will be documented

separately following the Company’s financial statements.

This examination report includes significant findings of fact and general information about the

insurer and its financial condition. There may be other items identified during the examination

that, due to their nature (e.g., subjective conclusions, proprietary information, etc.), are not

included within the examination report but separately communicated to other regulators and/or

the company.

3

The Company’s parent, Amica Mutual Insurance Company (“Amica Mutual”) owns 100% of

the capital stock of Amica P&C and Amica Life Insurance Company (“Amica Life”).

Concurrent examinations were also made of Amica Mutual and Amica Life, and reports

thereon are submitted under separate cover.

COMPANY HISTORY

Amica Property and Casualty Insurance Company was incorporated on May 11, 2005, through

the actions of its Incorporators, Robert A. DiMuccio and M. Stuart Towsey, Jr.

(“Incorporators”) and pursuant to the filing of its original Articles of Incorporation (“Charter”)

with the Secretary of State, as approved by the Director of the Department of Business

Regulation.

The Articles of Incorporation give the Company the authority to insure any and all risks except

life, annuity, title, and financial guaranty insurance and further provides that the authorized

capital stock of the Company shall be in one class of stock consisting of ten-thousand (10,000)

shares of common stock with a fifty-dollar ($50) par value. Subsequently, on June 8, 2005,

the Articles of Incorporation were amended to increase the par value to three hundred and fifty

dollars ($350).

4

On June 10, 2005, the Company issued ($3,500,000) of capital stock to Amica Mutual

Insurance Company consisting of ten-thousand (10,000) shares of common stock with a three

hundred and fifty dollar ($350) par value. Subsequently, on June 15, 2005, Amica Mutual

made a surplus contribution in the amount of eleven million dollars ($11,000,000). On January

1, 2013, Amica Mutual made a non-cash investment in the Company totaling $19.1 million

($19,120,193). This was done to facilitate the January 1, 2013 change in the quota share rate

of the reinsurance contract between the Company and Amica Mutual from 80% to 100% and

was for settlement of the Company’s December 31, 2012 reserve balances for losses, loss

adjustment expenses, and unearned premiums net of ceding commission.

The principal office of the Company is located within the home office building of its parent,

Amica Mutual Insurance Company, in the Town of Lincoln, Rhode Island.

MANAGEMENT AND CONTROL

Shareholders

The bylaws provide that the annual meeting of the shareholders shall be held at the principal

office of the Company in Lincoln, Rhode Island on the second Thursday in March in each year,

for the election of directors, and for the transaction of such other business as may be brought

before the meeting. Special meetings of the shareholders may be called in any manner

prescribed or permitted by law.

5

At all meetings of the shareholders, a majority of the shares entitled to vote, represented in

person or by proxy, shall constitute a quorum. Any corporate action may be decided by a

majority vote of those present in person or by proxy.

Board of Directors

The bylaws provide that the Board of Directors (“Board”) shall, except as limited by law, the

charter and the bylaws, have the power to direct the affairs, business, and property of the

Company.

The charter stipulates that the number of directors of the Company shall be fixed from time to

time by the bylaws but the number shall not be less than ten (10). The bylaws further stipulate

that the Board shall consist of twelve (12) members, a majority of whom are neither officers

nor employees of the Company and shall be elected as prescribed by the charter of the

Company. There is no term of office for directors specified in the bylaws; however, a review

of the minutes of the meetings of the shareholders revealed that directors were elected for the

term of one (1) year. The Company’s bylaws stipulate that directors shall retire no later than

the annual meeting following their 72nd birthday.

The bylaws provide that the Board of Directors shall hold a meeting within ten (10) days after

each annual meeting of the shareholders for the election of officers and committees and for the

transaction of any other business that may come before the meeting. The directors shall hold

as many meetings during the year as they shall prescribe. Special meetings of the directors

6

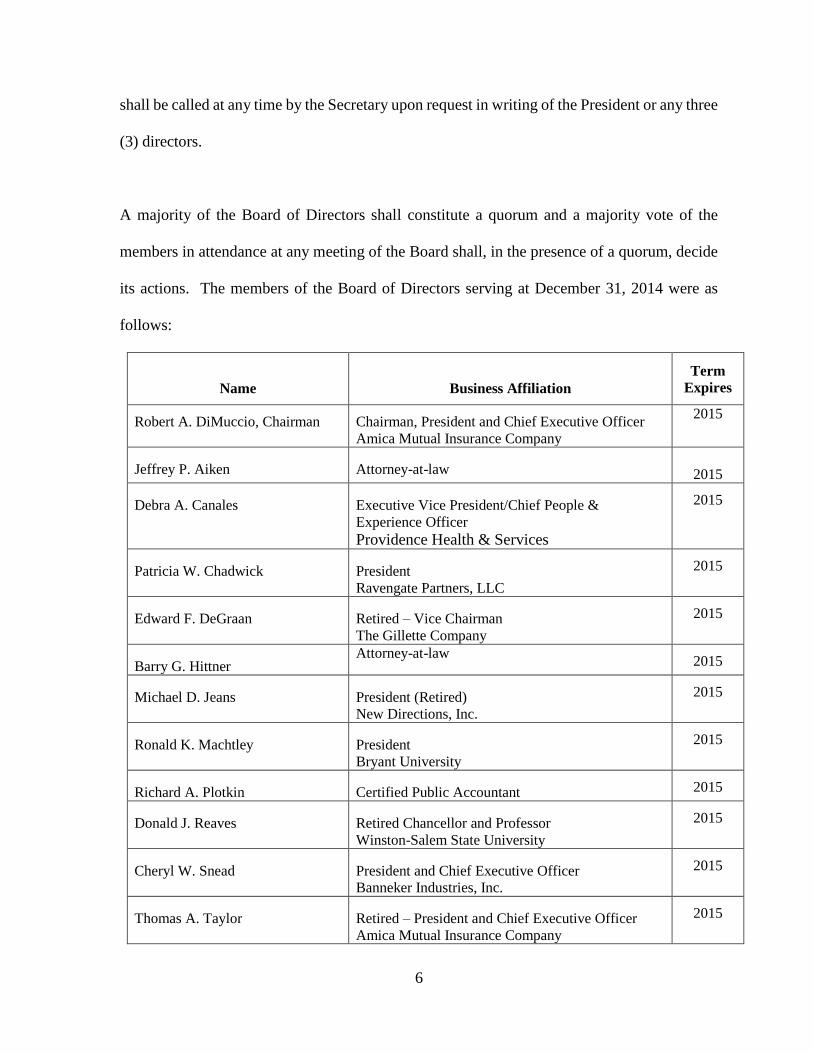

shall be called at any time by the Secretary upon request in writing of the President or any three

(3) directors.

A majority of the Board of Directors shall constitute a quorum and a majority vote of the

members in attendance at any meeting of the Board shall, in the presence of a quorum, decide

its actions. The members of the Board of Directors serving at December 31, 2014 were as

follows:

Name

Business Affiliation

Term

Expires

Robert A. DiMuccio, Chairman Chairman, President and Chief Executive Officer Amica Mutual Insurance Company

2015

Jeffrey P. Aiken Attorney-at-law

2015

Debra A. Canales Executive Vice President/Chief People &

Experience Officer

Providence Health & Services

2015

Patricia W. Chadwick President Ravengate Partners, LLC

2015

Edward F. DeGraan Retired – Vice Chairman The Gillette Company

2015

Barry G. Hittner Attorney-at-law

2015

Michael D. Jeans President (Retired) New Directions, Inc.

2015

Ronald K. Machtley President Bryant University

2015

Richard A. Plotkin Certified Public Accountant 2015

Donald J. Reaves Retired Chancellor and Professor Winston-Salem State University

2015

Cheryl W. Snead President and Chief Executive Officer Banneker Industries, Inc.

2015

Thomas A. Taylor Retired – President and Chief Executive Officer

Amica Mutual Insurance Company

2015

7

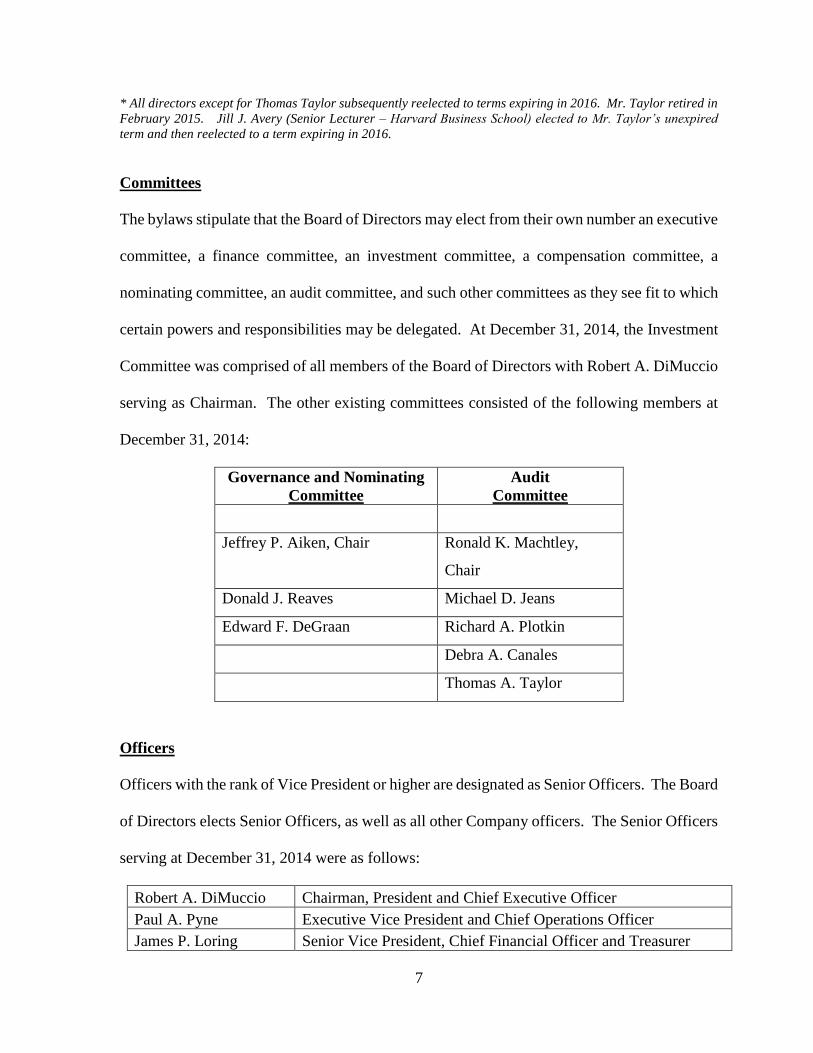

* All directors except for Thomas Taylor subsequently reelected to terms expiring in 2016. Mr. Taylor retired in

February 2015. Jill J. Avery (Senior Lecturer – Harvard Business School) elected to Mr. Taylor’s unexpired

term and then reelected to a term expiring in 2016.

Committees

The bylaws stipulate that the Board of Directors may elect from their own number an executive

committee, a finance committee, an investment committee, a compensation committee, a

nominating committee, an audit committee, and such other committees as they see fit to which

certain powers and responsibilities may be delegated. At December 31, 2014, the Investment

Committee was comprised of all members of the Board of Directors with Robert A. DiMuccio

serving as Chairman. The other existing committees consisted of the following members at

December 31, 2014:

Governance and Nominating

Committee

Audit

Committee

Jeffrey P. Aiken, Chair Ronald K. Machtley,

Chair

Donald J. Reaves Michael D. Jeans

Edward F. DeGraan Richard A. Plotkin

Debra A. Canales

Thomas A. Taylor

Officers

Officers with the rank of Vice President or higher are designated as Senior Officers. The Board

of Directors elects Senior Officers, as well as all other Company officers. The Senior Officers

serving at December 31, 2014 were as follows:

Robert A. DiMuccio Chairman, President and Chief Executive Officer

Paul A. Pyne Executive Vice President and Chief Operations Officer

James P. Loring Senior Vice President, Chief Financial Officer and Treasurer

8

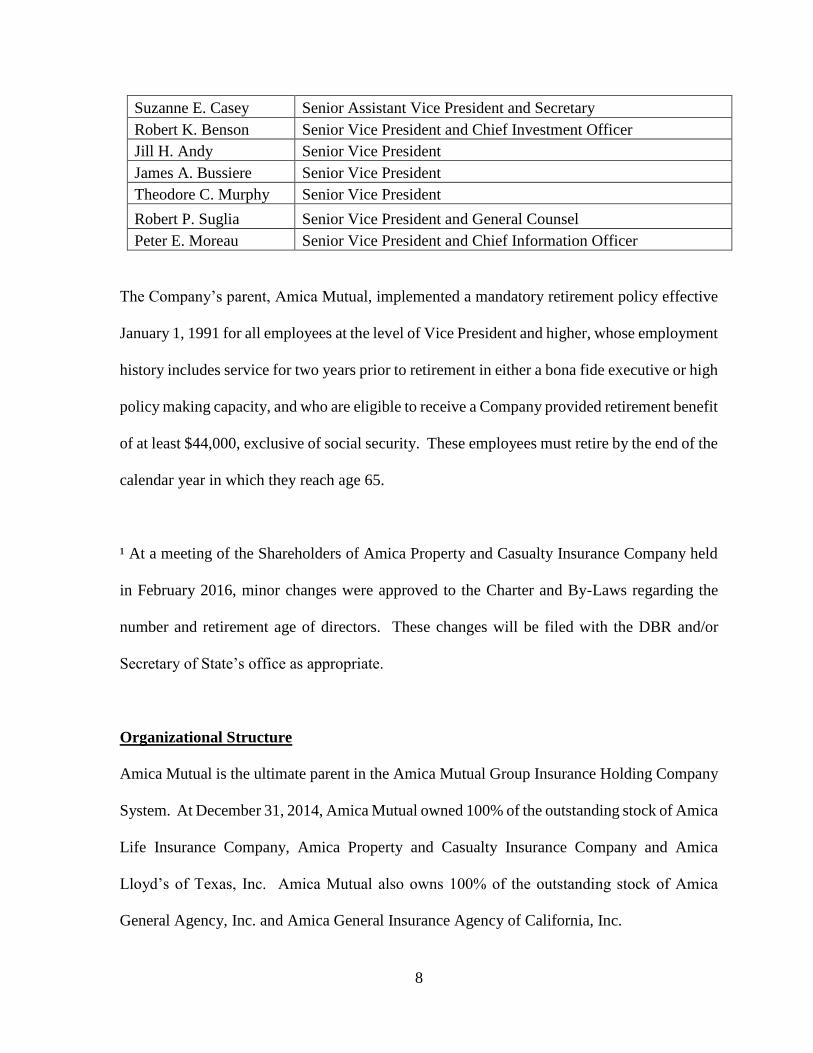

Suzanne E. Casey Senior Assistant Vice President and Secretary

Robert K. Benson Senior Vice President and Chief Investment Officer

Jill H. Andy Senior Vice President

James A. Bussiere Senior Vice President

Theodore C. Murphy Senior Vice President

Robert P. Suglia Senior Vice President and General Counsel

Peter E. Moreau Senior Vice President and Chief Information Officer

The Company’s parent, Amica Mutual, implemented a mandatory retirement policy effective

January 1, 1991 for all employees at the level of Vice President and higher, whose employment

history includes service for two years prior to retirement in either a bona fide executive or high

policy making capacity, and who are eligible to receive a Company provided retirement benefit

of at least $44,000, exclusive of social security. These employees must retire by the end of the

calendar year in which they reach age 65.

¹ At a meeting of the Shareholders of Amica Property and Casualty Insurance Company held

in February 2016, minor changes were approved to the Charter and By-Laws regarding the

number and retirement age of directors. These changes will be filed with the DBR and/or

Secretary of State’s office as appropriate.

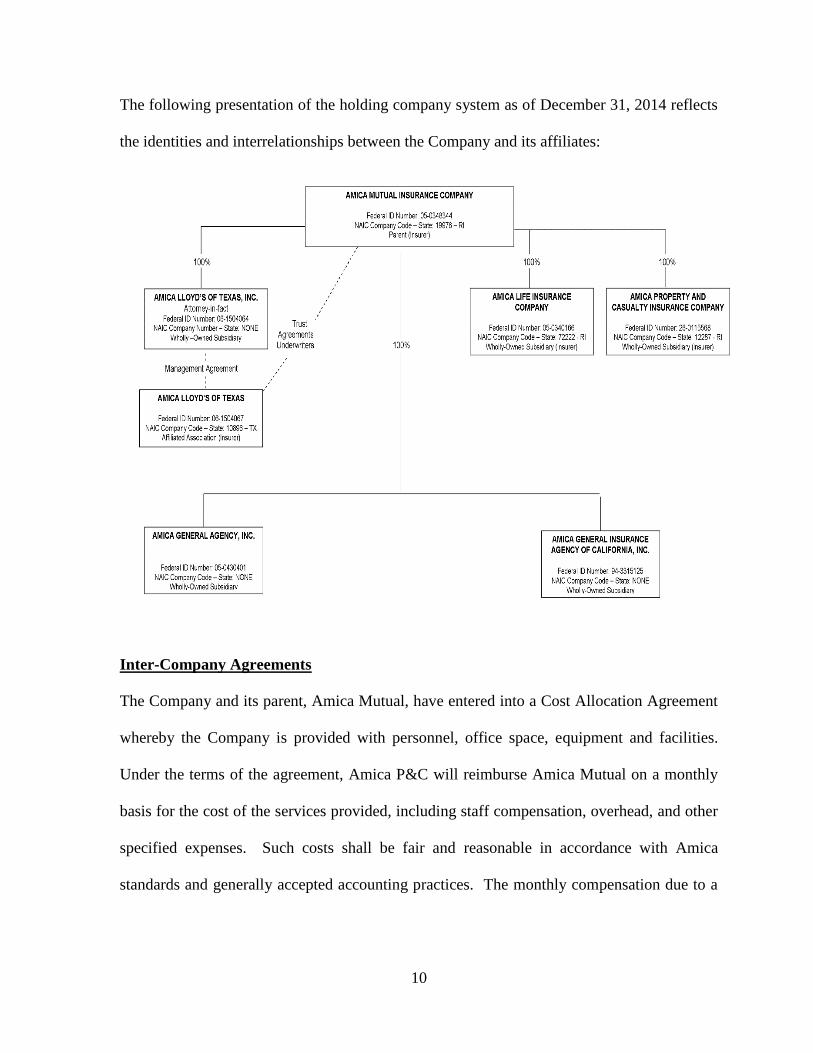

Organizational Structure

Amica Mutual is the ultimate parent in the Amica Mutual Group Insurance Holding Company

System. At December 31, 2014, Amica Mutual owned 100% of the outstanding stock of Amica

Life Insurance Company, Amica Property and Casualty Insurance Company and Amica

Lloyd’s of Texas, Inc. Amica Mutual also owns 100% of the outstanding stock of Amica

General Agency, Inc. and Amica General Insurance Agency of California, Inc.

9

Amica Lloyd’s of Texas, Inc. was organized as an attorney-in-fact to manage Amica Lloyd’s

of Texas, a Texas-domiciled insurer formed in 1998 to leverage the group’s competitive

position in the Texas insurance market. Through its ownership in Amica Lloyd’s of Texas,

Inc., Amica Mutual is the ultimate controlling entity of Amica Lloyd’s of Texas. Effective

January 1, 2014, business previously written by Amica Lloyd’s of Texas was written by Amica

Mutual upon renewal. Amica Lloyd’s operations will continue in 2015 to settle outstanding

losses and other liabilities. Management is evaluating the future plans of Amica Lloyd’s as it

continues to run off, with a final decision expected in 2015. (See Subsequent Events section

regarding 2015 merger with Amica Lloyds).

On January 1, 2013, Amica Mutual made a non-cash investment in the Company totaling $19.1

million. This was done to facilitate the January 1, 2013 change in the quota share rate of the

reinsurance contract between Amica P&C and the Company from 80% to 100% and was for

settlement of the Company’s December 31, 2012 reserve balances for losses, loss adjustment

expenses, and unearned premiums net of ceding commission.

10

The following presentation of the holding company system as of December 31, 2014 reflects

the identities and interrelationships between the Company and its affiliates:

Inter-Company Agreements

The Company and its parent, Amica Mutual, have entered into a Cost Allocation Agreement

whereby the Company is provided with personnel, office space, equipment and facilities.

Under the terms of the agreement, Amica P&C will reimburse Amica Mutual on a monthly

basis for the cost of the services provided, including staff compensation, overhead, and other

specified expenses. Such costs shall be fair and reasonable in accordance with Amica

standards and generally accepted accounting practices. The monthly compensation due to a

11

party shall be paid by the owing party within fifty-five (55) days of the end of the month to

which it applies.

The Company has entered into a Consolidated Federal Income Tax Agreement (“Tax

Agreement”) with Amica Mutual and its other affiliates, excluding Amica Life. Under the

terms of the Tax Agreement, allocation is made in accordance with Section 1552(a)(2) of the

Internal Revenue Code, and is based upon separate return calculations with current credit for

losses. The inter-company estimated tax balances are settled at least quarterly during the tax

year with a final settlement during the month following the filing of the consolidated income

tax return.

Prior to January 1, 2014, the Company was party to a Capital Maintenance Agreement with its

ultimate parent, Amica Mutual Insurance Company. The terms of the agreement stated that

when the ratio of net premiums written to surplus for the Company is above an agreed upon

ratio, Amica Mutual will infuse capital to restore surplus. As the Company no longer has net

written premiums due to the change in the quota share agreement discussed above,

management elected not to renew the Capital Maintenance Agreement for 2014.

An inter-company reinsurance agreement is in effect between the Company and Amica Mutual.

Refer to the ‘Reinsurance’ section of this report for details on this agreement.

12

TERRITORY AND PLAN OF OPERATION

A review of the certificates of authority in effect at December 31, 2014, and the Company’s

compliance with these, the examiners confirmed that the Company was licensed to transact

business in the states of Rhode Island, New Jersey and New York, and that the Company

appears to be operating in compliance with its certificates of authority.

The Articles of Incorporation and Rhode Island Certificate of Authority grant the Company

the authority to insure any and all risks except life, annuities, title, and mortgage and financial

guarantee insurance. Currently, the Company’s writings are confined to automobile liability

and automobile physical damage in the states of New Jersey and New York.

The Company has no policy-writing agents and business is acquired primarily through the

mail, telephone and internet. Company employees are appointed as agents to write property

and casualty insurance. The Company primarily services policyholders through two offices in

New Jersey and three offices in New York, which handle sales, claims, underwriting and other

service related matters for client accounts. In addition to its service offices, the Company

maintains three call centers for after hour customer service. The call centers are located in

Lincoln, Rhode Island., Carmel, Indiana, and Spokane, Washington. The processing of

premiums and the payment of all large losses are handled at the Company’s Corporate Office.

The Company began writing new policies by renewing Amica Mutual’s New Jersey auto

policies with effective dates of March 1, 2006 and later. Effective January 1, 2014 and upon

policy renewal, approximately 65% of the business previously written by the Company was

13

written by Amica Mutual. In addition, effective July 1, 2014, the Company began writing New

York auto policies. New auto business in New York will be written by either Amica Mutual or

the Company based on set underwriting criteria.

REINSURANCE

Intercompany Reinsurance

The Company participates in a Quota Share Reinsurance Agreement with its parent, Amica

Mutual Insurance Company. Under the terms of the Quota Share Reinsurance Agreement, the

Company shall cede and Amica Mutual shall accept a 100% quota share participation of the

Company’s net liability on risks under all binders, policies, contracts, certificates and other

obligations of insurance or reinsurance. From the Company’s inception of business to

December 31, 2012, the quota share participation rate was 80%; however, the rate was

amended to 100% effective January 1, 2013.

The Company also participates in pools where it is necessary to meet statutory obligations.

14

FINANCIAL STATEMENTS

The results of the examination are set forth in the following exhibits and schedules:

Comparative Statement of Assets, Liabilities, Surplus and Other Funds

December 31, 2014 and December 31, 2010

Statement of Income

Year ended December 31, 2014

Capital and Surplus Account

December 31, 2013 to December 31, 2014

Reconciliation of Surplus

December 31, 2010 to December 31, 2014

Analysis of Examination Adjustments

December 31, 2014

15

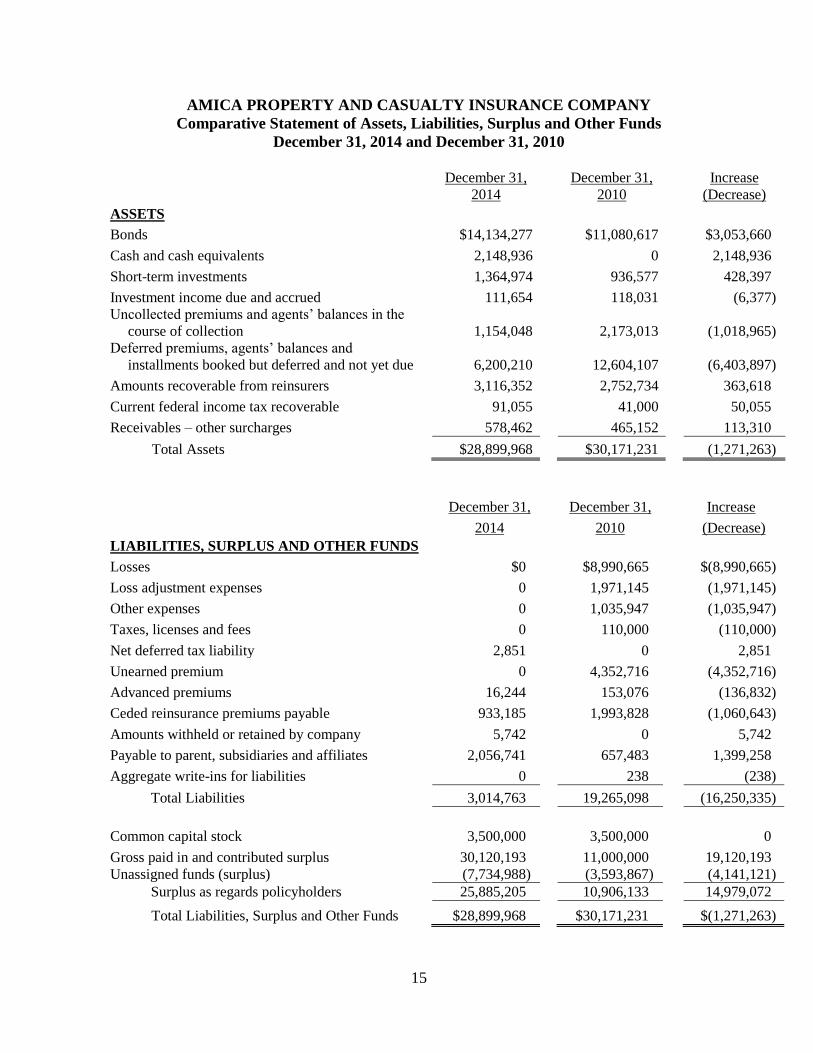

AMICA PROPERTY AND CASUALTY INSURANCE COMPANY

Comparative Statement of Assets, Liabilities, Surplus and Other Funds

December 31, 2014 and December 31, 2010

December 31, December 31, Increase

2014 2010 (Decrease)

ASSETS

Bonds $14,134,277 $11,080,617 $3,053,660

Cash and cash equivalents 2,148,936 0 2,148,936

Short-term investments 1,364,974 936,577 428,397

Investment income due and accrued 111,654 118,031 (6,377)

Uncollected premiums and agents’ balances in the

course of collection 1,154,048 2,173,013 (1,018,965)

Deferred premiums, agents’ balances and

installments booked but deferred and not yet due 6,200,210 12,604,107 (6,403,897)

Amounts recoverable from reinsurers 3,116,352 2,752,734 363,618

Current federal income tax recoverable 91,055 41,000 50,055

Receivables – other surcharges 578,462 465,152 113,310

Total Assets $28,899,968 $30,171,231 (1,271,263)

December 31, December 31, Increase

2014 2010 (Decrease)

LIABILITIES, SURPLUS AND OTHER FUNDS

Losses $0 $8,990,665 $(8,990,665)

Loss adjustment expenses 0 1,971,145 (1,971,145)

Other expenses 0 1,035,947 (1,035,947)

Taxes, licenses and fees 0 110,000 (110,000)

Net deferred tax liability 2,851 0 2,851

Unearned premium 0 4,352,716 (4,352,716)

Advanced premiums 16,244 153,076 (136,832)

Ceded reinsurance premiums payable 933,185 1,993,828 (1,060,643)

Amounts withheld or retained by company 5,742 0 5,742

Payable to parent, subsidiaries and affiliates 2,056,741 657,483 1,399,258

Aggregate write-ins for liabilities 0 238 (238)

Total Liabilities 3,014,763 19,265,098 (16,250,335)

Common capital stock 3,500,000 3,500,000 0

Gross paid in and contributed surplus 30,120,193 11,000,000 19,120,193

Unassigned funds (surplus) (7,734,988) (3,593,867) (4,141,121)

Surplus as regards policyholders 25,885,205 10,906,133 14,979,072

Total Liabilities, Surplus and Other Funds $28,899,968 $30,171,231 $(1,271,263)

16

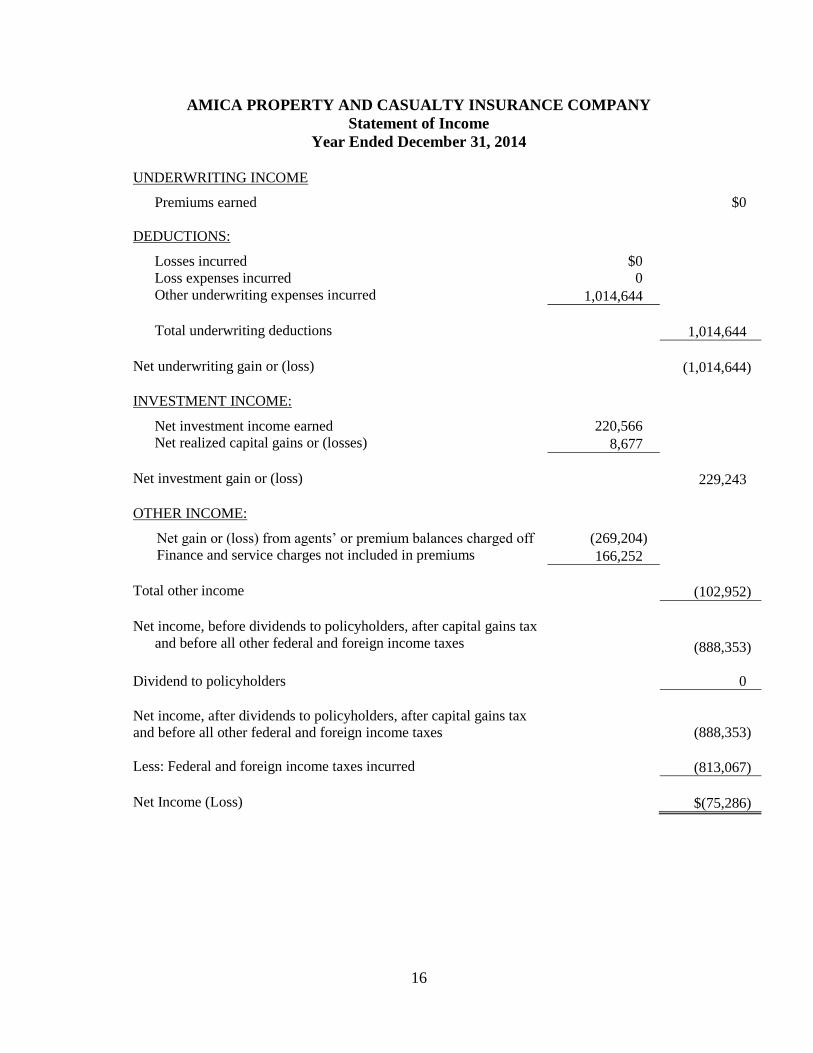

AMICA PROPERTY AND CASUALTY INSURANCE COMPANY

Statement of Income

Year Ended December 31, 2014

UNDERWRITING INCOME

Premiums earned $0

DEDUCTIONS:

Losses incurred $0

Loss expenses incurred 0

Other underwriting expenses incurred 1,014,644

Total underwriting deductions 1,014,644

Net underwriting gain or (loss) (1,014,644)

INVESTMENT INCOME:

Net investment income earned 220,566

Net realized capital gains or (losses) 8,677

Net investment gain or (loss) 229,243

OTHER INCOME:

Net gain or (loss) from agents’ or premium balances charged off (269,204)

Finance and service charges not included in premiums 166,252

Total other income (102,952)

Net income, before dividends to policyholders, after capital gains tax

and before all other federal and foreign income taxes (888,353)

Dividend to policyholders 0

Net income, after dividends to policyholders, after capital gains tax

and before all other federal and foreign income taxes (888,353)

Less: Federal and foreign income taxes incurred (813,067)

Net Income (Loss) $(75,286)

17

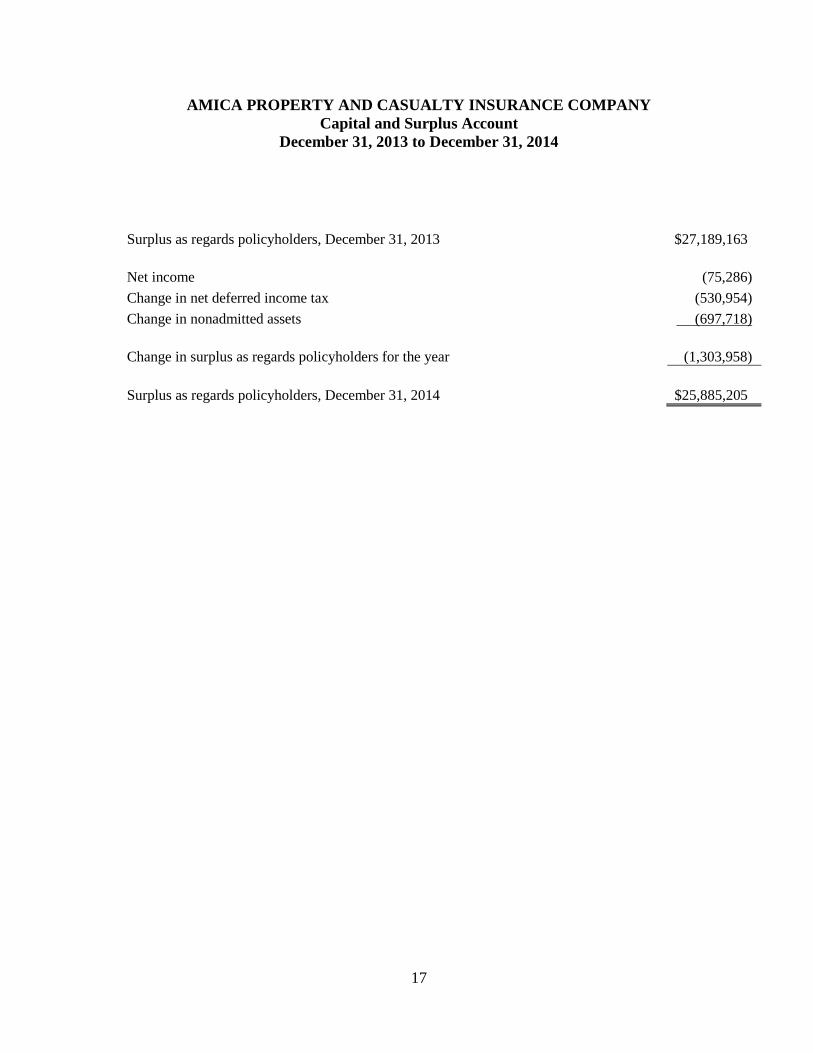

AMICA PROPERTY AND CASUALTY INSURANCE COMPANY

Capital and Surplus Account

December 31, 2013 to December 31, 2014

Surplus as regards policyholders, December 31, 2013 $27,189,163

Net income (75,286)

Change in net deferred income tax (530,954)

Change in nonadmitted assets (697,718)

Change in surplus as regards policyholders for the year (1,303,958)

Surplus as regards policyholders, December 31, 2014 $25,885,205

18

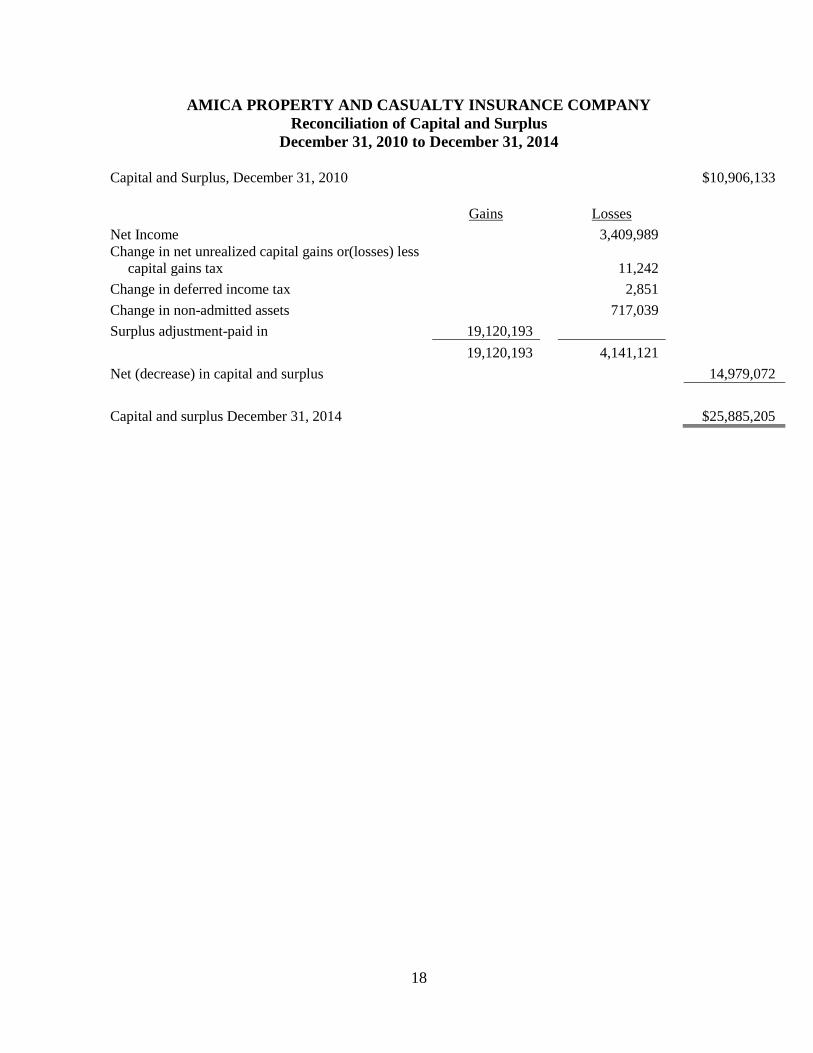

AMICA PROPERTY AND CASUALTY INSURANCE COMPANY

Reconciliation of Capital and Surplus

December 31, 2010 to December 31, 2014

Capital and Surplus, December 31, 2010 $10,906,133

Gains Losses

Net Income 3,409,989

Change in net unrealized capital gains or(losses) less

capital gains tax 11,242

Change in deferred income tax 2,851

Change in non-admitted assets 717,039

Surplus adjustment-paid in 19,120,193

19,120,193 4,141,121

Net (decrease) in capital and surplus 14,979,072

Capital and surplus December 31, 2014 $25,885,205

19

AMICA PROPERTY AND CASUALTY INSURANCE COMPANY

Analysis of Examination Adjustments

December 31, 2014

The examination of the Company performed as of December 31, 2014, did not disclose any

material misstatements to the financial statements contained in its 2014 Annual Statement

filing. Accordingly, the amounts reported by the Company have been accepted for purposes

of this report.

20

ASSETS

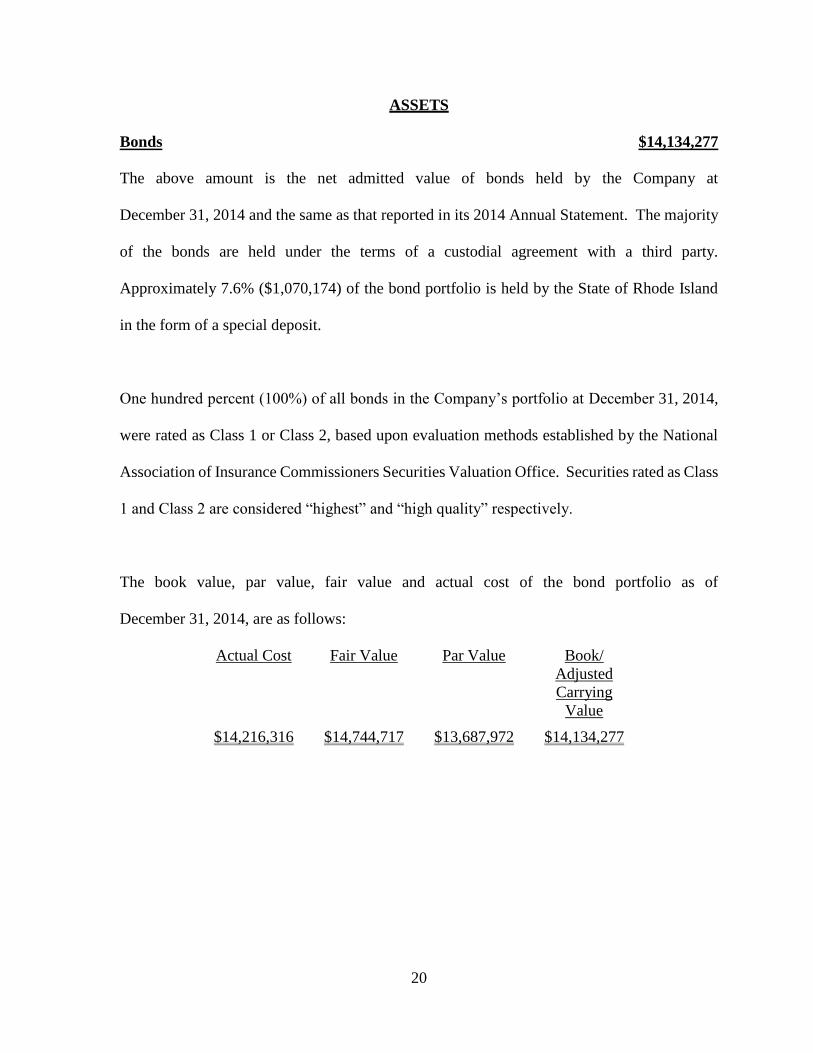

Bonds $14,134,277

The above amount is the net admitted value of bonds held by the Company at

December 31, 2014 and the same as that reported in its 2014 Annual Statement. The majority

of the bonds are held under the terms of a custodial agreement with a third party.

Approximately 7.6% ($1,070,174) of the bond portfolio is held by the State of Rhode Island

in the form of a special deposit.

One hundred percent (100%) of all bonds in the Company’s portfolio at December 31, 2014,

were rated as Class 1 or Class 2, based upon evaluation methods established by the National

Association of Insurance Commissioners Securities Valuation Office. Securities rated as Class

1 and Class 2 are considered “highest” and “high quality” respectively.

The book value, par value, fair value and actual cost of the bond portfolio as of

December 31, 2014, are as follows:

Actual Cost Fair Value Par Value Book/

Adjusted

Carrying

Value

$14,216,316 $14,744,717 $13,687,972 $14,134,277

21

LIABILITIES

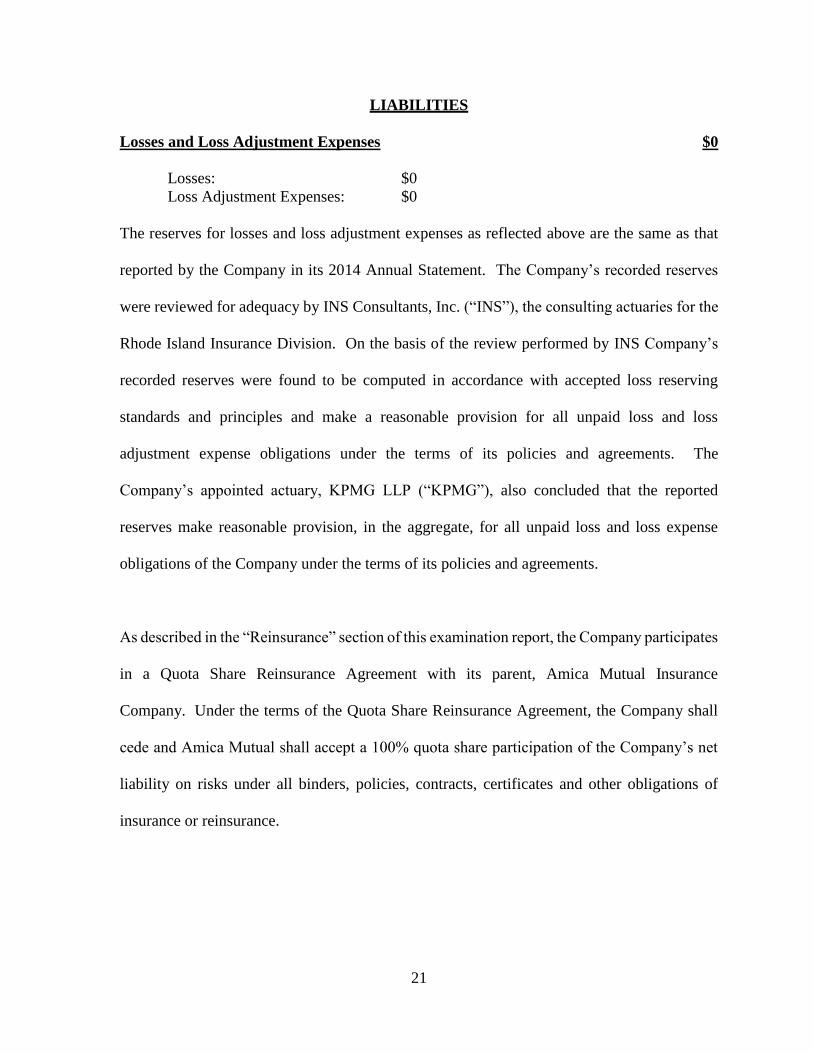

Losses and Loss Adjustment Expenses $0

Losses: $0

Loss Adjustment Expenses: $0

The reserves for losses and loss adjustment expenses as reflected above are the same as that

reported by the Company in its 2014 Annual Statement. The Company’s recorded reserves

were reviewed for adequacy by INS Consultants, Inc. (“INS”), the consulting actuaries for the

Rhode Island Insurance Division. On the basis of the review performed by INS Company’s

recorded reserves were found to be computed in accordance with accepted loss reserving

standards and principles and make a reasonable provision for all unpaid loss and loss

adjustment expense obligations under the terms of its policies and agreements. The

Company’s appointed actuary, KPMG LLP (“KPMG”), also concluded that the reported

reserves make reasonable provision, in the aggregate, for all unpaid loss and loss expense

obligations of the Company under the terms of its policies and agreements.

As described in the “Reinsurance” section of this examination report, the Company participates

in a Quota Share Reinsurance Agreement with its parent, Amica Mutual Insurance

Company. Under the terms of the Quota Share Reinsurance Agreement, the Company shall

cede and Amica Mutual shall accept a 100% quota share participation of the Company’s net

liability on risks under all binders, policies, contracts, certificates and other obligations of

insurance or reinsurance.

22

CAPITAL AND SURPLUS

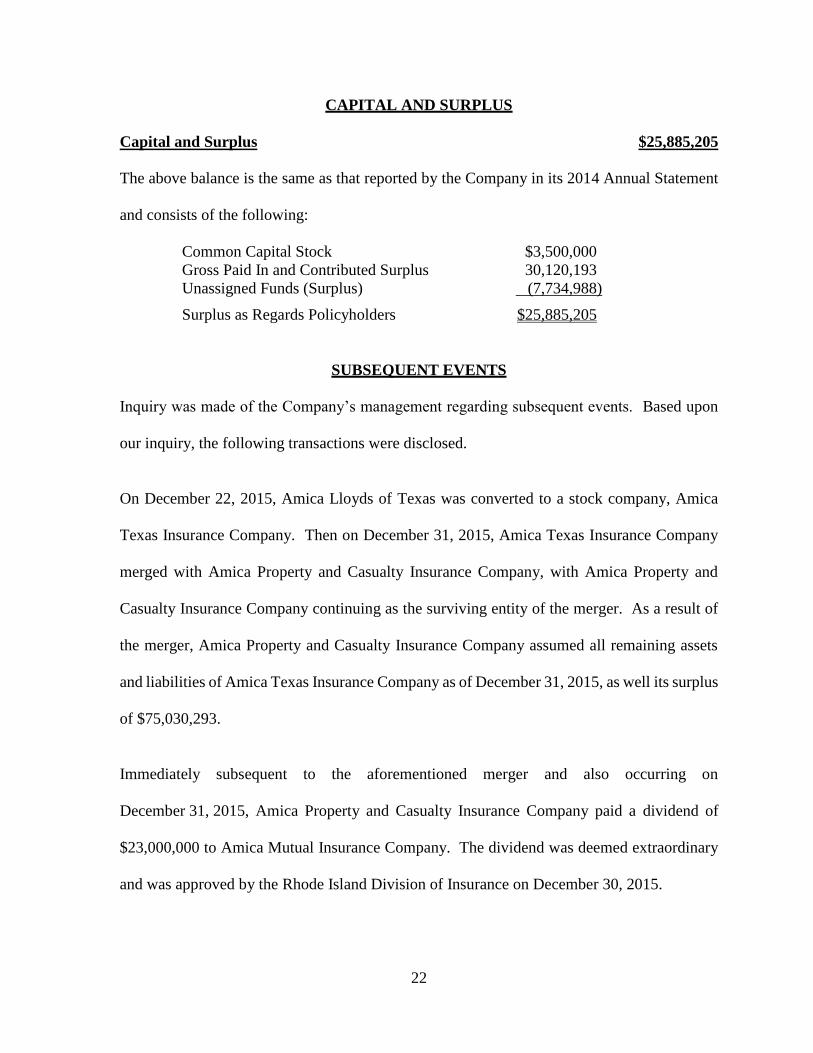

Capital and Surplus $25,885,205

The above balance is the same as that reported by the Company in its 2014 Annual Statement

and consists of the following:

Common Capital Stock $3,500,000

Gross Paid In and Contributed Surplus 30,120,193

Unassigned Funds (Surplus) (7,734,988)

Surplus as Regards Policyholders $25,885,205

SUBSEQUENT EVENTS

Inquiry was made of the Company’s management regarding subsequent events. Based upon

our inquiry, the following transactions were disclosed.

On December 22, 2015, Amica Lloyds of Texas was converted to a stock company, Amica

Texas Insurance Company. Then on December 31, 2015, Amica Texas Insurance Company

merged with Amica Property and Casualty Insurance Company, with Amica Property and

Casualty Insurance Company continuing as the surviving entity of the merger. As a result of

the merger, Amica Property and Casualty Insurance Company assumed all remaining assets

and liabilities of Amica Texas Insurance Company as of December 31, 2015, as well its surplus

of $75,030,293.

Immediately subsequent to the aforementioned merger and also occurring on

December 31, 2015, Amica Property and Casualty Insurance Company paid a dividend of

$23,000,000 to Amica Mutual Insurance Company. The dividend was deemed extraordinary

and was approved by the Rhode Island Division of Insurance on December 30, 2015.

23

Effective December 31, 2015, Amica Lloyd’s of Texas, Inc., an attorney-in-fact and a wholly-

owned subsidiary of Amica Mutual Insurance Company, was dissolved.

CONCLUSION

We have applied verification procedures to the data and information contained in this report

using sampling techniques and other examination procedures as deemed appropriate. While

sampling and other examination procedures do not give complete assurance that all errors and

irregularities will be detected, had any been detected during the course of this examination,

such errors and/or irregularities would have been disclosed in this report. Other than what has

been noted in the body of this report, we were not informed of, and did not become aware of

any errors or irregularities that could have a material effect on the financial condition of the

Company as presented in this report.

Acknowledgment is made of the services rendered by INS Consultants, Inc., the Rhode Island

Insurance Division’s consulting actuaries.

Assisting in the examination with the undersigned were John Tudino Jr., CFE, CIE, CFSA,

Insurance Examiner-In-Charge, Theodore J. Hurley, CPA, CFE, Insurance Examiner-In-

Charge, Debra Almeida, CFE, Senior Insurance Examiner, and Anthony Humphrey, Insurance

Examiner.

Respectfully submitted,

Louis A. Gabriele, CPA, CFE

Insurance Examiner-In-Charge

Rhode Island Insurance Division