3rd Meeting of Task Force 2 on “Advancement of ... · Power Market Outlook ... This was followed...

90

1 icfi.com | Presentation on the progress and preliminary findings of the study on “Assessment of the Electricity Trading Potential in the South Asia region” 25 th February 2015 3 rd Meeting of Task Force 2 on “Advancement of Transmission Systems Interconnection”

Transcript of 3rd Meeting of Task Force 2 on “Advancement of ... · Power Market Outlook ... This was followed...

1icfi.com |

Presentation on the progress and preliminary findings of the study on “Assessment of the Electricity Trading Potential in the South Asia region”

25th February 2015

3rd Meeting of Task Force 2 on “Advancement of Transmission Systems Interconnection”

2icfi.com |

• Project objective and scope of work as per Terms of Reference

• Project approach and methodology

• Methodology for estimation of unrestricted electricity demand, electricity

supply and peak demand forecast for South Asian Nations

• Findings/analysis on Demand-Supply projections of the South Asian Nations

• Introduction to ICF’s Integrated Planning Model (IPM®)

• Model assumptions and model run results for India

• Data support needed from Task Force members

• Way Forward

• Appendices

Presentation Outline

3icfi.com |

Project Objective

To identify the electricity trading potential of the South Asian nations (India, Bangladesh,

Bhutan, Nepal, Sri Lanka, Pakistan, Maldives and Afghanistan) over a period of next 20 years

by reviewing the existing long term Demand-Supply projections of the participating

countries.

4icfi.com |

Project Scope of Work

1. The study to account all types of generating plants viz Hydro, Thermal, Nuclear and Renewable.

2. Collect, compile, review and analyze the existing/prevailing long term Demand-Supply (D-S)projections/data available in respect of each South Asian country. This shall include differentgeneration capacity addition scenarios.

3. Assess whether existing D-S projections have adequately been taken up and have explored theCross Border Electricity Trade (CBET) potentials of each South Asian country from the tradingperspectives and in the time horizon of 10-20 years.

4. If the data including the perspective generation capacity addition projections are not availablefrom various sources for the time horizon of 10-20 years, a proper methodology* to be adoptedto arrive at reasonable D-S projections to explore the CBET potential of each South Asian country.

5. The above D-S projections shall include the year wise trading opportunities that arise out ofseasonal variations, time zone difference, difference in load curve, different weekends andholidays being followed in each South Asian nation.

*Methodology to be adopted for arriving at these projections shall be finalized in consultation with the respective Task Force 2 countrymembers and shall include a ‘sensitivity analysis’ of the same. Based on the approved methodology, country wise projections shall be madein respect of the various seasonal scenarios (including peak/off-peak conditions) and in terms of both MW and MWhr for the specified timehorizon of next 10-20 years.

5icfi.com |

Project Deliverables

1. (a) Submit a Draft report on the Findings/Analysis on the existing Demand-Supply projections (MW, MWh) of each South Asian Nation.

(b) Wherever data projections are not available upto the specified time horizon, a separate draft report shall be submitted, identifying the shortcomings and the projections (including assumptions) made in respect of the Demand-Supply (MW, MWh) for a period of next 10-20 years covering plantwise breakup of generation and the fuel being used etc.

2. Make presentation(s) on the above Draft reports to the Task Force 2 members as and whenrequired

3. Submit an interim report, incorporating all suggestions/recommendations to the respectiveprovisions by the Task Force 2 members and IRADe.

4. Make presentation(s) before the Task Force 2 members, Project Steering Committee (PSC),IRADe and USAID on the interim report, as and when required.

5. Submit the Final report based on the feedback received from all stakeholders.

6icfi.com |

Project Approach & Methodology

The overall project approach has been divided into following three parts:

1. Power Sector Historical Analysis and Current Overview:a) Review of historical Demand-Supply trends. Collation of data on historical –

i. Peak load and energy demandii. Capacity addition and generationiii. Energy and peak deficits

b) Analysis of Existing and Future Transmission Capacity

2. Power Market Outlook (2014 to 2034 – 20 Years): Base case development using ICF’s IPM® (Integrated Planning Model). Towards populating the modeling framework, ICF will build develop assumptions on demand, supply, future generation and transmission builds, fuel supply and renewable forecasts besides other areas.

3. Scenario Analysis: Analysis around the base case to assess the impact of variables for same timeframe as base case

IPM® is a long-term capacity expansion and production costing model for electric power systems including generation and transmission. It is a multi-regional, deterministic, dynamic, linear programming model.

Deliverable 1 (a) + partly 1 (b)

7icfi.com |

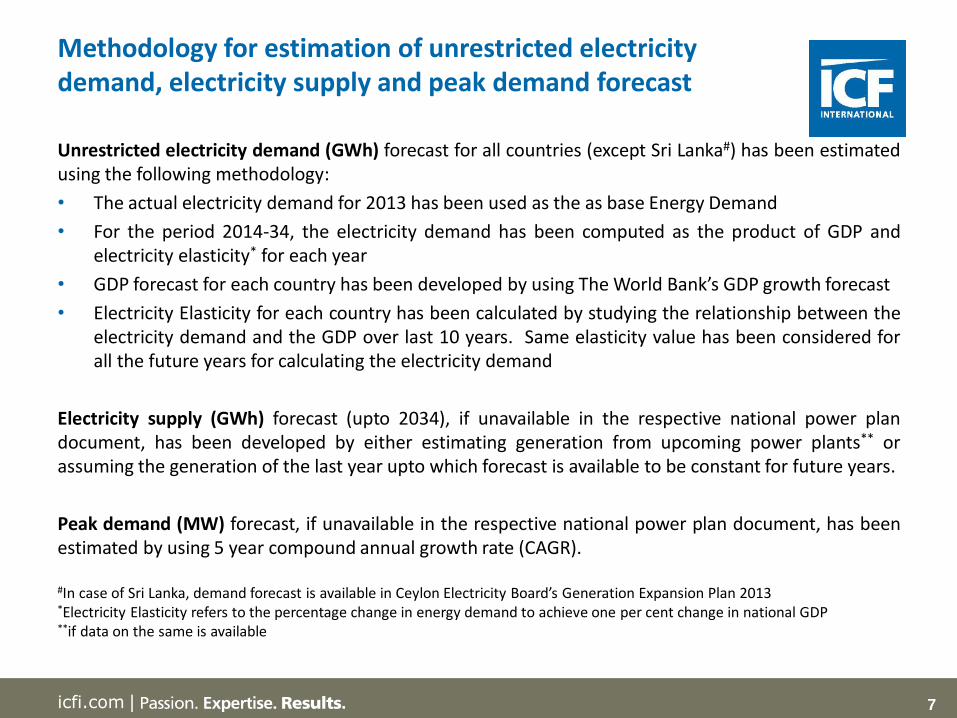

Methodology for estimation of unrestricted electricitydemand, electricity supply and peak demand forecast

Unrestricted electricity demand (GWh) forecast for all countries (except Sri Lanka#) has been estimatedusing the following methodology:

• The actual electricity demand for 2013 has been used as the as base Energy Demand

• For the period 2014-34, the electricity demand has been computed as the product of GDP andelectricity elasticity* for each year

• GDP forecast for each country has been developed by using The World Bank’s GDP growth forecast

• Electricity Elasticity for each country has been calculated by studying the relationship between theelectricity demand and the GDP over last 10 years. Same elasticity value has been considered forall the future years for calculating the electricity demand

Electricity supply (GWh) forecast (upto 2034), if unavailable in the respective national power plandocument, has been developed by either estimating generation from upcoming power plants** orassuming the generation of the last year upto which forecast is available to be constant for future years.

Peak demand (MW) forecast, if unavailable in the respective national power plan document, has beenestimated by using 5 year compound annual growth rate (CAGR).

#In case of Sri Lanka, demand forecast is available in Ceylon Electricity Board’s Generation Expansion Plan 2013*Electricity Elasticity refers to the percentage change in energy demand to achieve one per cent change in national GDP**if data on the same is available

8icfi.com |

Findings/Analysis on the existing Demand-Supply projections of the South Asian Nations

Deliverable 1 (a) + partly 1(b) as per Project Terms of Reference

9icfi.com |

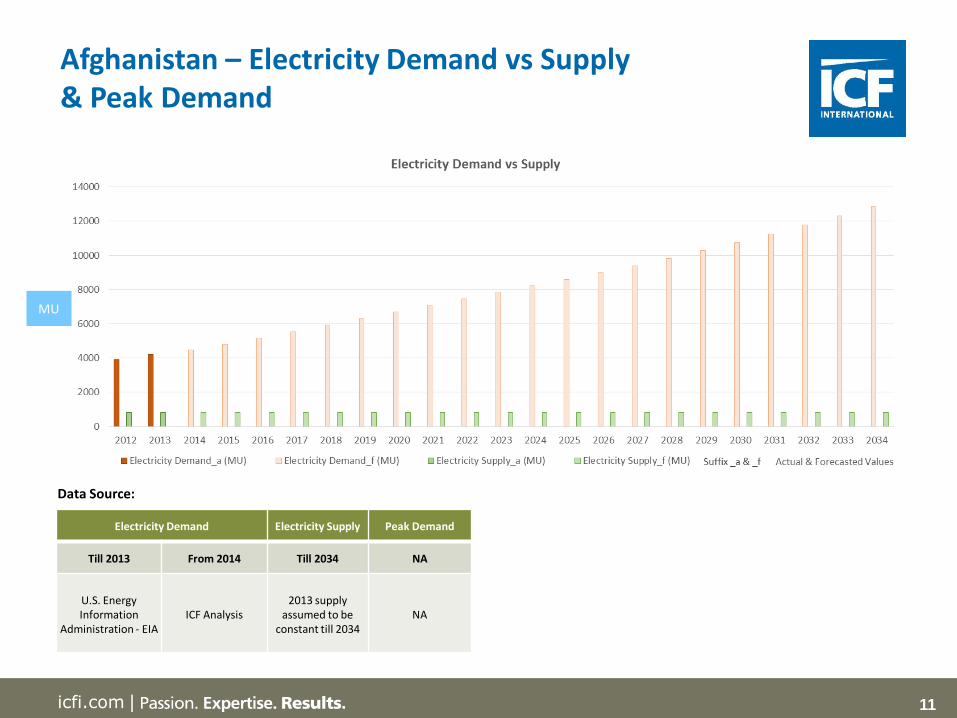

Afghanistan – Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

10icfi.com |

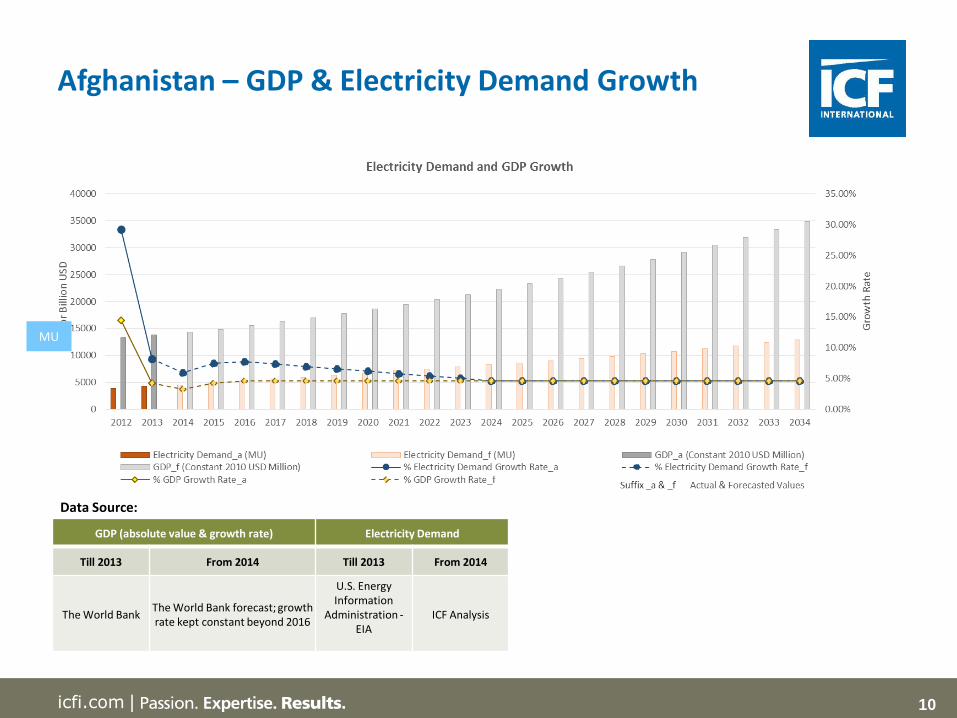

Afghanistan – GDP & Electricity Demand Growth

Data Source:

GDP (absolute value & growth rate) Electricity Demand

Till 2013 From 2014 Till 2013 From 2014

The World BankThe World Bank forecast; growth rate kept constant beyond 2016

U.S. Energy Information

Administration -EIA

ICF Analysis

MU

11icfi.com |

Afghanistan – Electricity Demand vs Supply & Peak Demand

Data Source:

Electricity Demand Electricity Supply Peak Demand

Till 2013 From 2014 Till 2034 NA

U.S. Energy Information

Administration - EIAICF Analysis

2013 supply assumed to be

constant till 2034NA

MU

12icfi.com |

Afghanistan – Load Profile 2013

Data for Afghanistan Load Profile (8760 hours) is Not Available

13icfi.com |

Bangladesh – Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

14icfi.com |

Bangladesh – GDP & Electricity Demand Growth

Data Source:

BPDP - Bangladesh Power Development Board

GDP (absolute value & growth rate) Electricity Demand

Till 2013 From 2014 Till 2013 From 2014

The World Bank The World Bank forecast; growth rate kept constant

2016 onwardsBPDP ICF Analysis

15icfi.com |

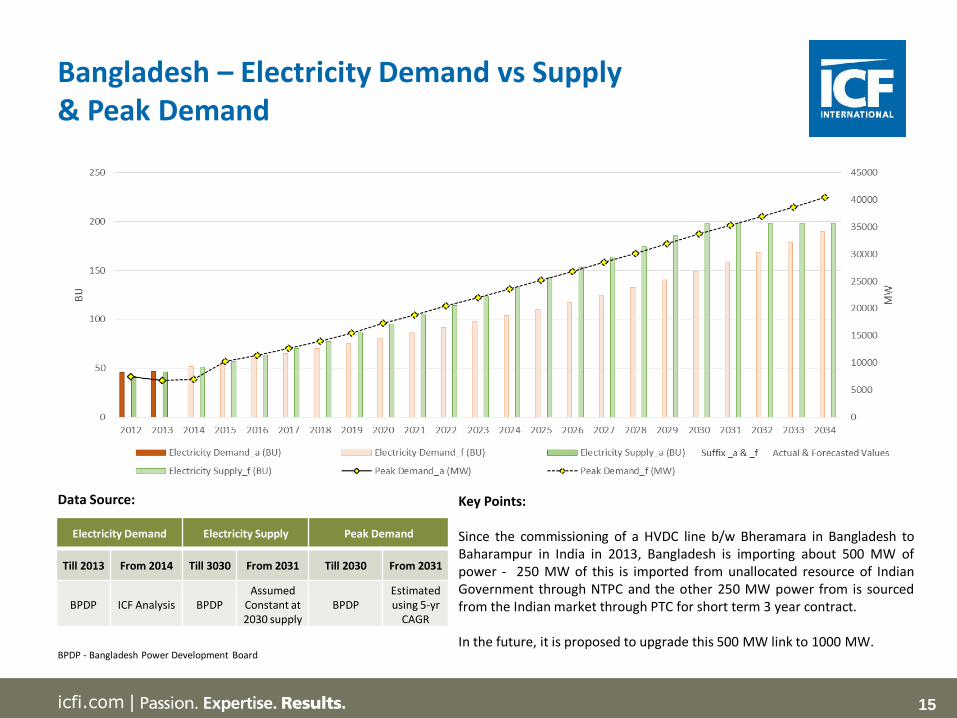

Bangladesh – Electricity Demand vs Supply & Peak Demand

Data Source:

BPDP - Bangladesh Power Development Board

Electricity Demand Electricity Supply Peak Demand

Till 2013 From 2014 Till 3030 From 2031 Till 2030 From 2031

BPDP ICF Analysis BPDPAssumed

Constant at 2030 supply

BPDPEstimated using 5-yr

CAGR

Key Points:

Since the commissioning of a HVDC line b/w Bheramara in Bangladesh toBaharampur in India in 2013, Bangladesh is importing about 500 MW ofpower - 250 MW of this is imported from unallocated resource of IndianGovernment through NTPC and the other 250 MW power from is sourcedfrom the Indian market through PTC for short term 3 year contract.

In the future, it is proposed to upgrade this 500 MW link to 1000 MW.

16icfi.com |

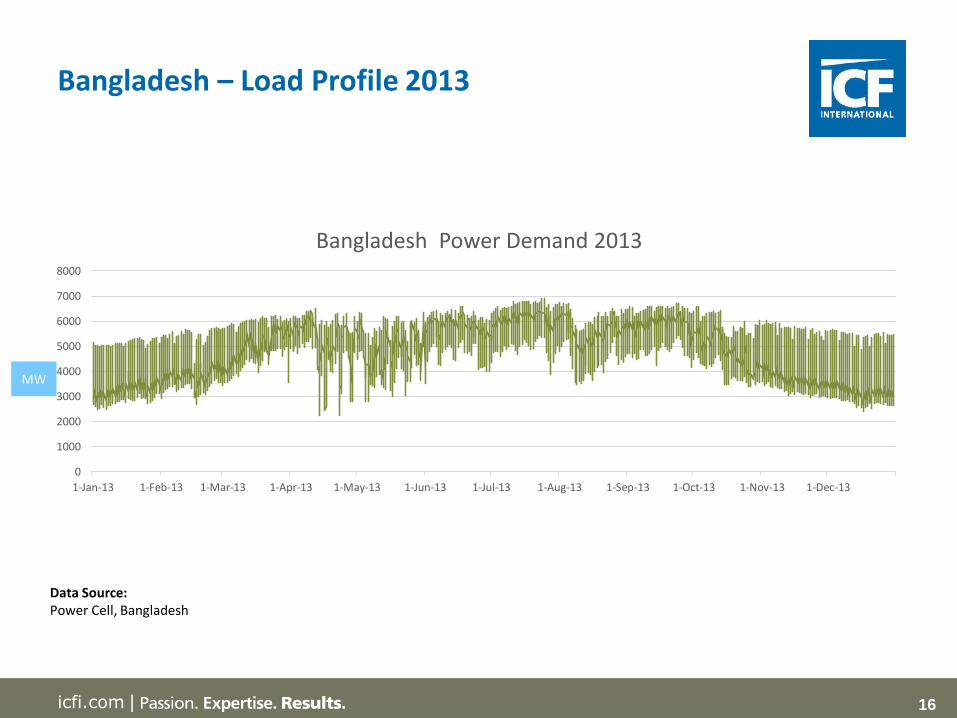

Bangladesh – Load Profile 2013

Data Source:Power Cell, Bangladesh

0

1000

2000

3000

4000

5000

6000

7000

8000

1-Jan-13 1-Feb-13 1-Mar-13 1-Apr-13 1-May-13 1-Jun-13 1-Jul-13 1-Aug-13 1-Sep-13 1-Oct-13 1-Nov-13 1-Dec-13

Bangladesh Power Demand 2013

MW

17icfi.com |

Bhutan – Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

18icfi.com |

Bhutan – GDP & Electricity Demand Growth

Data Source:

GDP (absolute value & growth rate) Electricity Demand

Till 2013 From 2014 Till 2013 From 2014

The World BankThe World Bank forecast; growth rate kept constant

2016 onwards

Bhutan AnnualStatistical Yearbook

ICF Analysis

MU

19icfi.com |

Bhutan – Electricity Demand vs Supply & Peak Demand

Data Source:

NTGMP – National Transmission Grid Master Plan for BhutanCEA – Central Electricity Authority

Electricity Demand Electricity Supply Peak Demand

Till 2013 From 2014 Till 2013 From 2014 Till 2030 From 2031

Bhutan Annual

Statistical Yearbook

ICF Analysis

Bhutan Annual

Statistical Yearbook

NTGMP by CEA, India

NTGMP by CEA, India

Estimatedusing

5-yr CAGR

Key Points:

Electricity trade b/w India and Bhutan was initiated in 1961 when Bhutanstarted sourcing power from the Jaldhaka HPP set up in West Bengal, India.This was followed by construction of mini/micro hydel project in Bhutan withGrant Assistance from Government of India (GoI).

Currently Bhutan is exporting about 1300 MW power from Chhukha, Kurichhu,Tala, Basochhu – I&II Power Plants in the peak Monsoon season. The 126 MWDagachhu Power Plant (built under PPP mode) in Bhutan is now commissionedand will soon participate in the open Power Markets operational in India.

MU

20icfi.com |

Data for Bhutan Load Profile (8760 hours) is Not Available

However, Power Data Book 2013 published by Bhutan Power Corporation Limited (BPCL) provides Load Curve for a typical day in 2013 summer and winter for Thimpu and Phuntsholing, as shown in the following slides:

Bhutan – Load Profile 2013

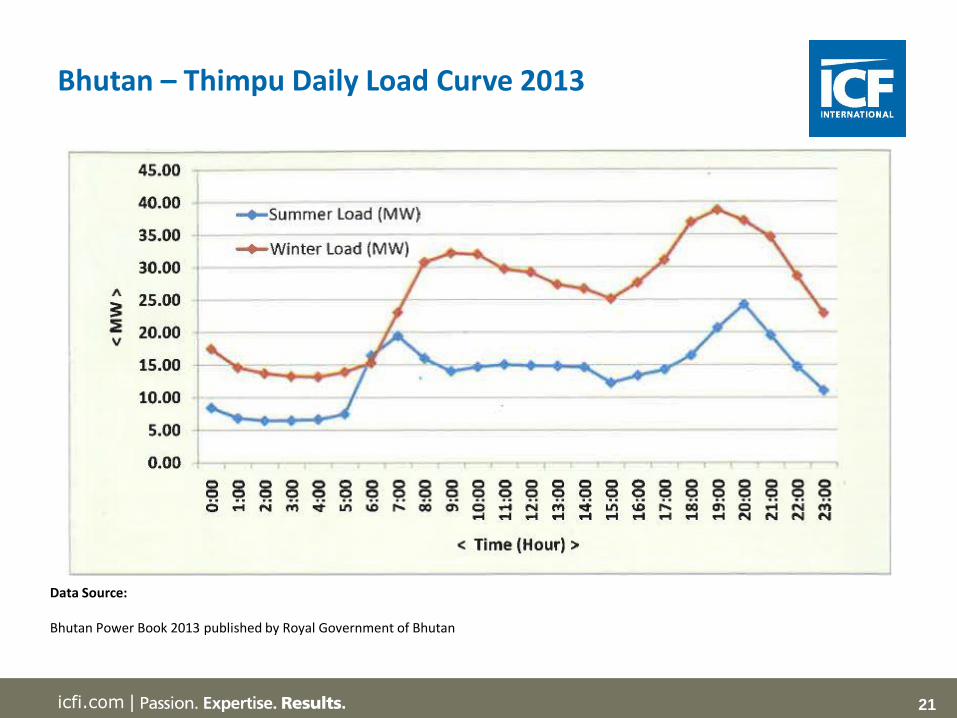

21icfi.com |

Bhutan – Thimpu Daily Load Curve 2013

Data Source:

Bhutan Power Book 2013 published by Royal Government of Bhutan

22icfi.com |

Bhutan – Phuntsholing Daily Load Curve 2013

Data Source:

Bhutan Power Book 2013 published by Royal Government of Bhutan

23icfi.com |

India - Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

24icfi.com |

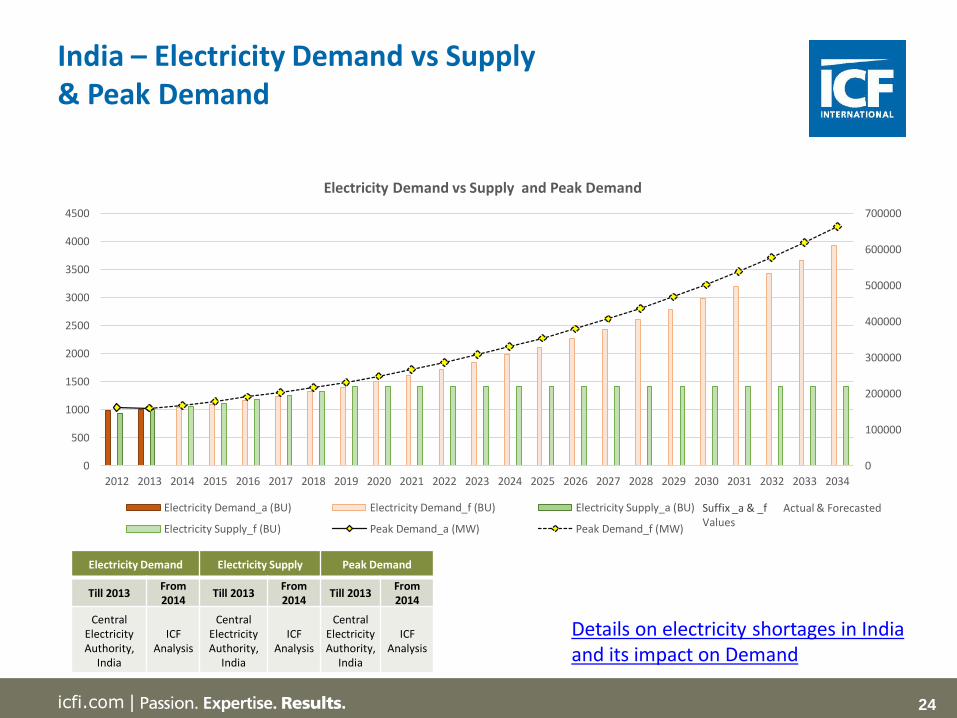

India – Electricity Demand vs Supply & Peak Demand

0

100000

200000

300000

400000

500000

600000

700000

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Electricity Demand vs Supply and Peak Demand

Electricity Demand_a (BU) Electricity Demand_f (BU) Electricity Supply_a (BU)

Electricity Supply_f (BU) Peak Demand_a (MW) Peak Demand_f (MW)

Suffix _a & _f Actual & Forecasted Values

Details on electricity shortages in India and its impact on Demand

Electricity Demand Electricity Supply Peak Demand

Till 2013From 2014

Till 2013From2014

Till 2013From 2014

Central ElectricityAuthority,

India

ICF Analysis

Central ElectricityAuthority,

India

ICF Analysis

Central ElectricityAuthority,

India

ICF Analysis

25icfi.com |

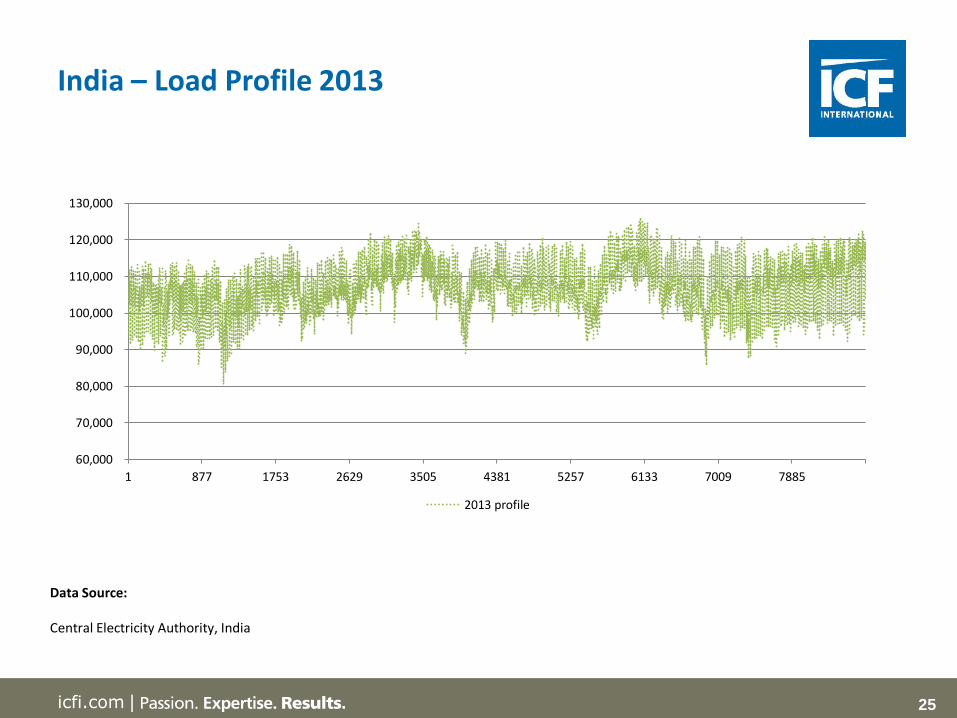

India – Load Profile 2013

Data Source:

Central Electricity Authority, India

60,000

70,000

80,000

90,000

100,000

110,000

120,000

130,000

1 877 1753 2629 3505 4381 5257 6133 7009 7885

2013 profile

26icfi.com |

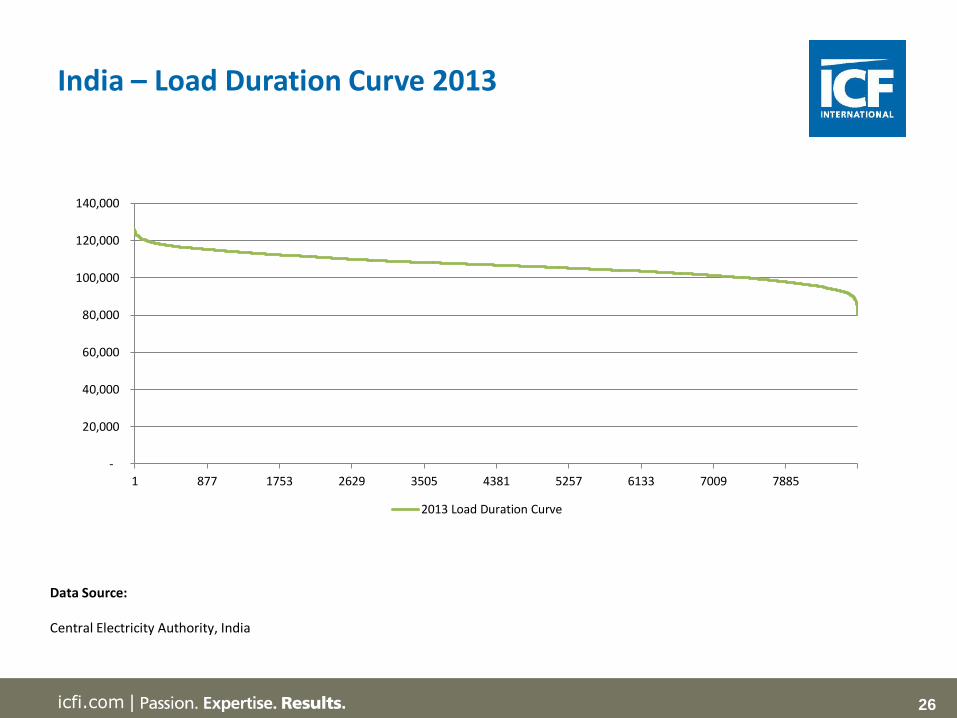

India – Load Duration Curve 2013

Data Source:

Central Electricity Authority, India

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1 877 1753 2629 3505 4381 5257 6133 7009 7885

2013 Load Duration Curve

27icfi.com |

Maldives – Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

28icfi.com |

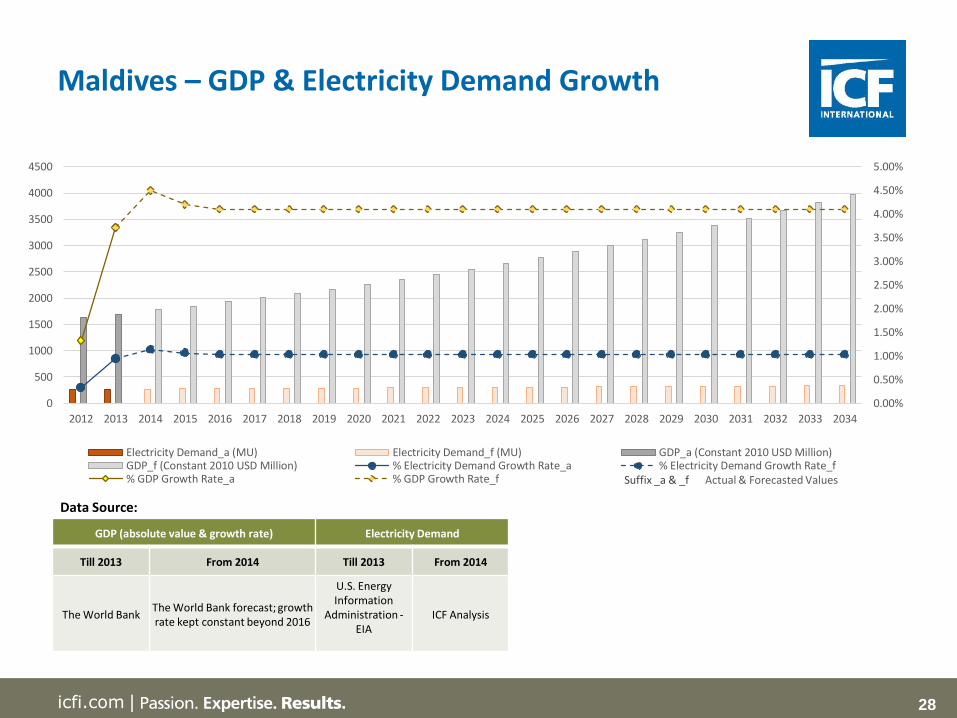

Maldives – GDP & Electricity Demand Growth

Data Source:

GDP (absolute value & growth rate) Electricity Demand

Till 2013 From 2014 Till 2013 From 2014

The World BankThe World Bank forecast; growth rate kept constant beyond 2016

U.S. Energy Information

Administration -EIA

ICF Analysis

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Electricity Demand_a (MU) Electricity Demand_f (MU) GDP_a (Constant 2010 USD Million)GDP_f (Constant 2010 USD Million) % Electricity Demand Growth Rate_a % Electricity Demand Growth Rate_f% GDP Growth Rate_a % GDP Growth Rate_f Suffix _a & _f Actual & Forecasted Values

29icfi.com |

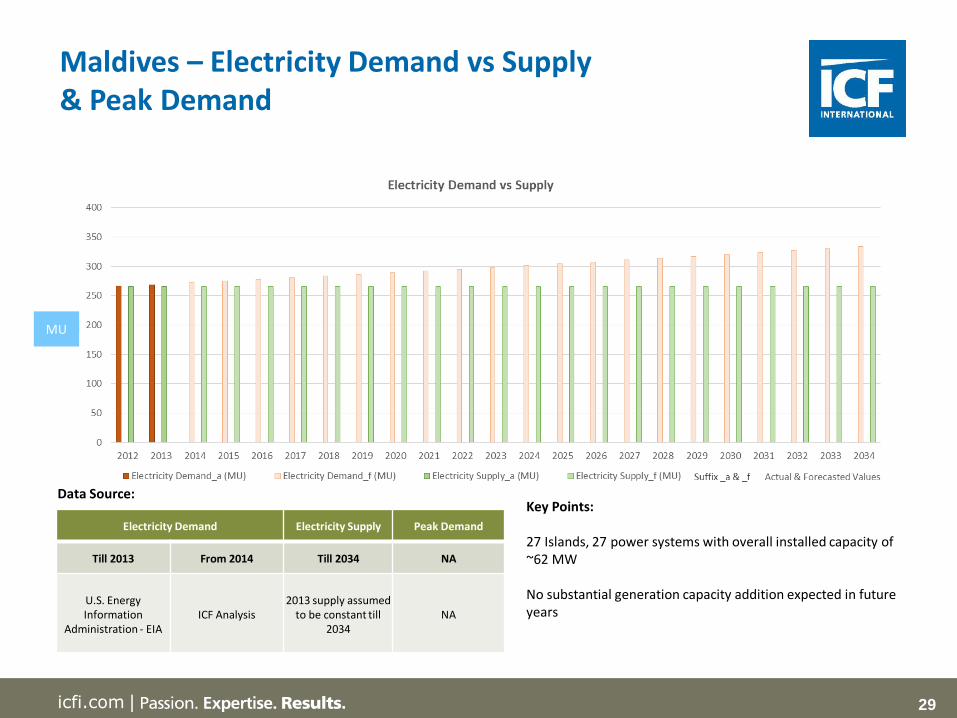

Maldives – Electricity Demand vs Supply & Peak Demand

Data Source:

LTGEP – Long Term Generation Expansion Plan

Electricity Demand Electricity Supply Peak Demand

Till 2013 From 2014 Till 2034 NA

U.S. Energy Information

Administration - EIAICF Analysis

2013 supply assumed to be constant till

2034NA

Key Points:

27 Islands, 27 power systems with overall installed capacity of ~62 MW

No substantial generation capacity addition expected in future years

MU

30icfi.com |

Maldives – Load Profile 2013

Data for Maldives Load Profile (8760 hours) is Not Available

31icfi.com |

Nepal – Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

32icfi.com |

Nepal – GDP & Electricity Demand Growth

Data Source:

GDP (absolute value & growth rate) Electricity Demand

Till 2013 From 2014 Till 2033 2034

The World BankThe World Bank forecast; growth rate kept constant

2016 onwards

Nepal ElectricityAuthority

Annual Report 2014

ICF Analysis

Key Points:

• Nepal has very high electricity shortages • Unrestricted Demand data for past 3 years has been used to

forecast future demand

MU

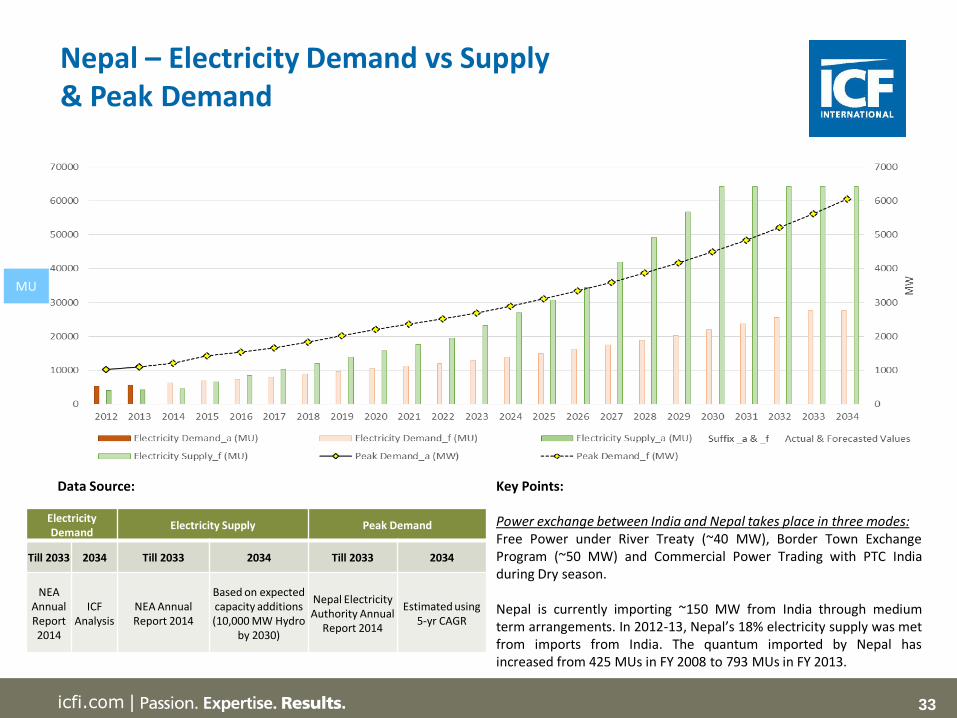

33icfi.com |

Nepal – Electricity Demand vs Supply & Peak Demand

Data Source:

Electricity Demand

Electricity Supply Peak Demand

Till 2033 2034 Till 2033 2034 Till 2033 2034

NEA Annual Report 2014

ICF Analysis

NEA Annual Report 2014

Based on expected capacity additions(10,000 MW Hydro

by 2030)

Nepal ElectricityAuthority Annual

Report 2014

Estimated using 5-yr CAGR

Key Points:

Power exchange between India and Nepal takes place in three modes:Free Power under River Treaty (~40 MW), Border Town ExchangeProgram (~50 MW) and Commercial Power Trading with PTC Indiaduring Dry season.

Nepal is currently importing ~150 MW from India through mediumterm arrangements. In 2012-13, Nepal’s 18% electricity supply was metfrom imports from India. The quantum imported by Nepal hasincreased from 425 MUs in FY 2008 to 793 MUs in FY 2013.

MU

34icfi.com |

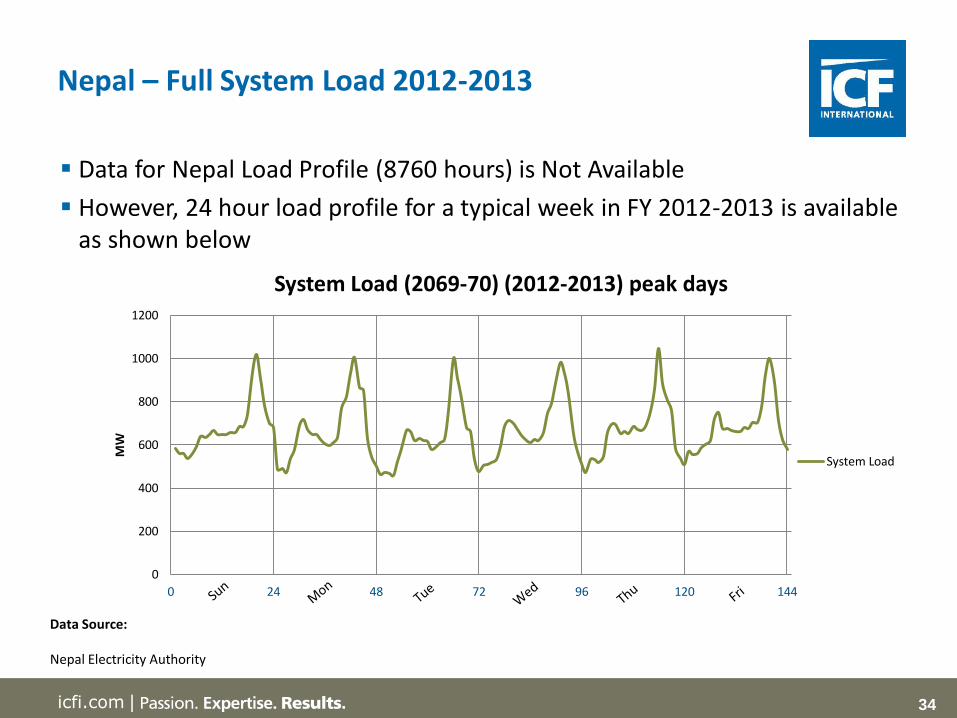

Nepal – Full System Load 2012-2013

Data Source:

Nepal Electricity Authority

0

200

400

600

800

1000

1200

0 24 48 72 96 120 144

MW

System Load (2069-70) (2012-2013) peak days

System Load

Data for Nepal Load Profile (8760 hours) is Not Available

However, 24 hour load profile for a typical week in FY 2012-2013 is available as shown below

35icfi.com |

Pakistan – Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

36icfi.com |

Pakistan – GDP & Electricity Demand Growth

Data Source:

GDP (absolute value & growth rate) Electricity Demand

Till 2013 From 2014 Till 2034

The World Bank

The World Bank forecast; growth rate kept constant 2016

onwards

ICF Analysis using Electricity Demand Data from National Power

System Expansion Plan prepared by the National Transmission and

Despatch Company, Pakistan

Key Points:

Electricity demand in Pakistan follows an asymmetric pattern. The demand has strongly been influenced by GDP during high growth period 1999-2006

37icfi.com |

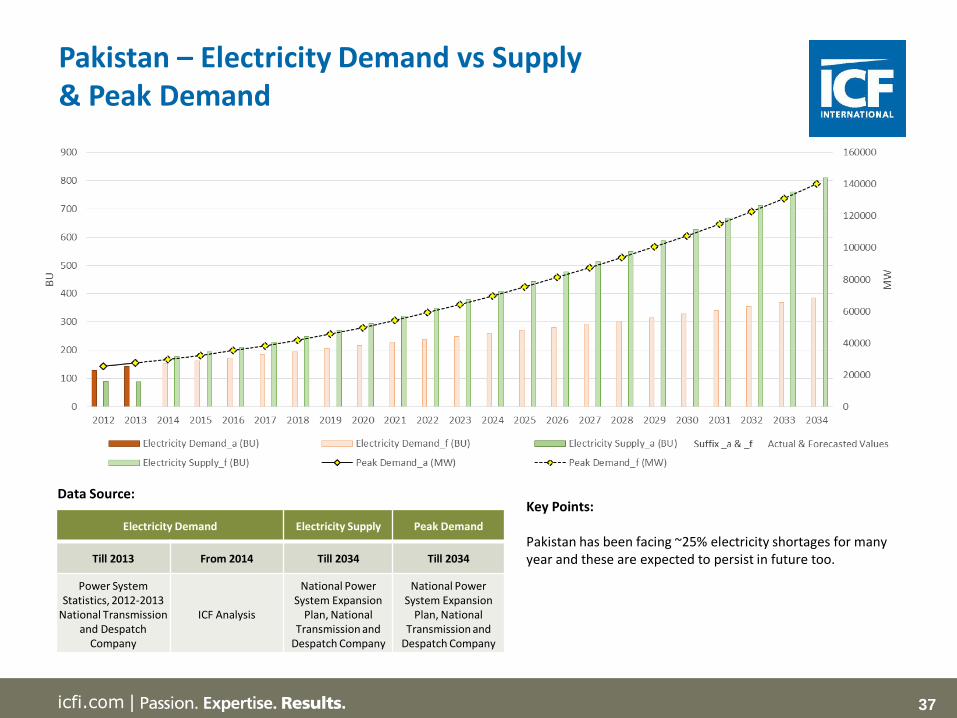

Pakistan – Electricity Demand vs Supply & Peak Demand

Data Source:

LTGEP – Long Term Generation Expansion Plan

Electricity Demand Electricity Supply Peak Demand

Till 2013 From 2014 Till 2034 Till 2034

Power System Statistics, 2012-2013

National Transmission and Despatch

Company

ICF Analysis

National Power System Expansion

Plan, National Transmission and

Despatch Company

National Power System Expansion

Plan, National Transmission and

Despatch Company

Key Points:

Pakistan has been facing ~25% electricity shortages for many year and these are expected to persist in future too.

38icfi.com |

Pakistan – Load Profile 2013

Data for Pakistan Load Profile (8760 hours) is Not Available

39icfi.com |

Sri Lanka – Findings & Analysis on Electricity Demand, Electricity Supply and Peak Demand

40icfi.com |

Sri Lanka – Electricity Demand vs Supply & Peak Demand

Data Source:

LTGEP – Long Term Generation Expansion Plan

Electricity Demand Electricity Supply Peak Demand

Till 2034 Till 2034 Till 2034

LTGEP,Ceylon Electricity Board

LTGEP,Ceylon Electricity Board

LTGEP,Ceylon Electricity Board

0

1000

2000

3000

4000

5000

6000

7000

8000

0

5

10

15

20

25

30

35

40

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Electricity Demand_a (BU) Electricity Demand_f (BU) Electricity Supply_a (BU)

Electricity Supply_f (BU) Peak Demand_a (MW) Peak Demand_f (MW)

Suffix _a & _f Actual & Forecasted Values

41icfi.com |

Sri Lanka – Full System Load 2012-2013

Data Source:

Sri Lanka Sustainable Energy Authority

Data for Sri Lanka Load Profile (8760 hours) is Not Available

However, 24 hour load profile for a system maximum night peak in 2013 is available as shown below

42icfi.com |

Conclusion: Demand-Supply Scenario for South Asian Nations

43icfi.com |

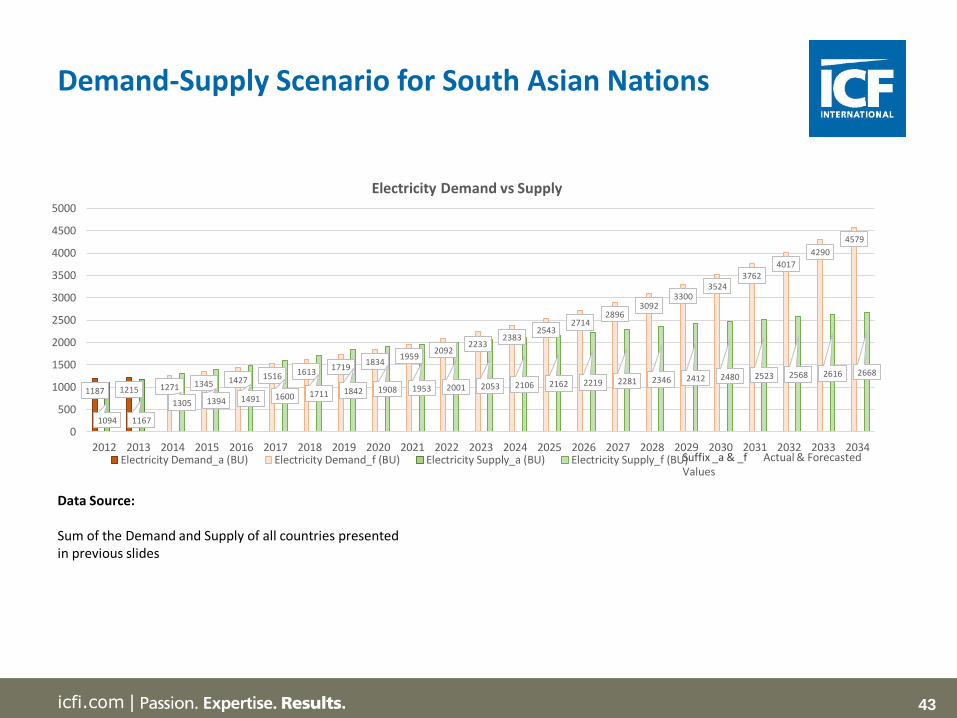

Demand-Supply Scenario for South Asian Nations

Data Source:

Sum of the Demand and Supply of all countries presented in previous slides

1187 1215 1271 1345 1427 1516 16131719

18341959

20922233

23832543

27142896

30923300

35243762

4017

4290

4579

1094 1167

1305 1394 1491 1600 1711 1842 1908 1953 2001 2053 2106 2162 2219 2281 2346 2412 2480 2523 2568 2616 2668

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Electricity Demand vs Supply

Electricity Demand_a (BU) Electricity Demand_f (BU) Electricity Supply_a (BU) Electricity Supply_f (BU)Suffix _a & _f Actual & Forecasted Values

44icfi.com |

ICF’s Integrated Planning Model (IPM®)

45icfi.com |

ICF provides Modeling tools across a range of sectors

Fuels Power, EE Environment

Integrated Planning Model ®Gas Market Model ®

Energy Asset Decision Support

System®

Gas Market Clearing

Engine Building Energy Analysis

Console (Beacon™)

Energy Efficiency Potential

Models

Carbon Planning Model

(CPM™)

Greenhouse Gas

Emissions Management

System®

GHG Portfolio™

International Carbon

Pricing Tool (InCaP™)

Kyoto Project Risk

Management System®

Rating and Evaluation

System for Prioritizing

Investments in Reducing

Emissions®

Coal Asset Depletion

Optimization Model ®

Aviation

46icfi.com |

IPM® is an excellent and versatile long range

planning model

IPM® is a long-term capacity expansion and production costing model forelectric power systems including generation, transmission, andprocess/district heat production from co-generation and stand-aloneboilers

It is a multi-regional, deterministic, dynamic, linear programming model

Utilizes Dynamic Optimization Framework with an Objective Function ofMinimizing the Present Value of Total System Cost subject to:

• Electricity & Steam Demand Constraints

• Reserve Margin Constraints

• Environmental Constraints

• Transmission Constraints

• Fuel Constraints

• Other Operational Constraints

Simulates rational expectations for perfect foresight providing theframework for inter-temporal decision making

46

47icfi.com |

Integrated Planning Model (IPM®)

47

More details on IPM in Appendix

48icfi.com |

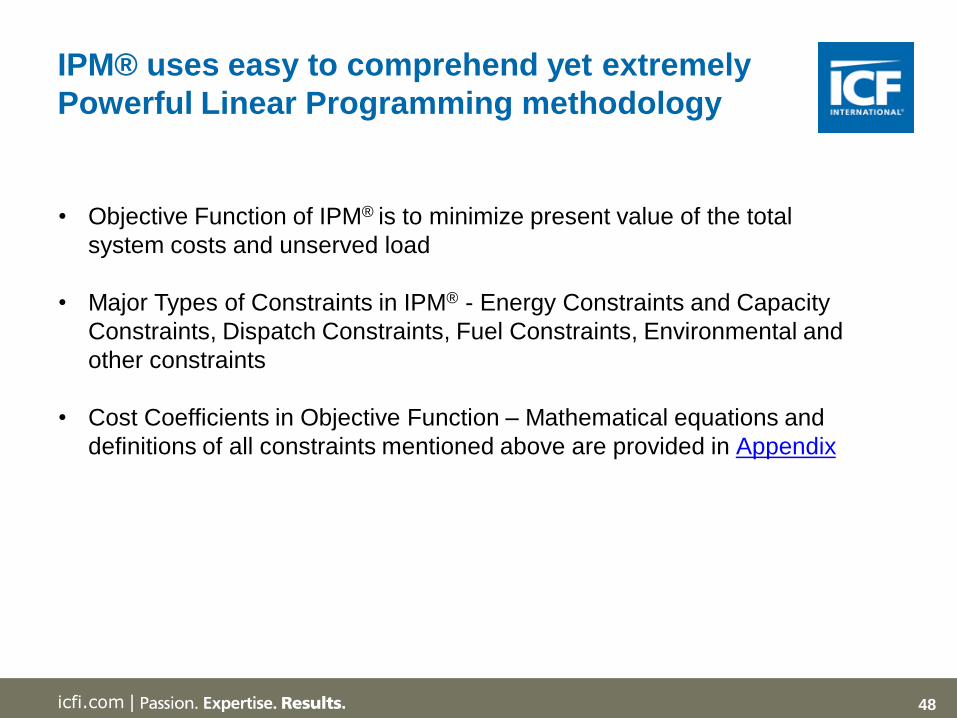

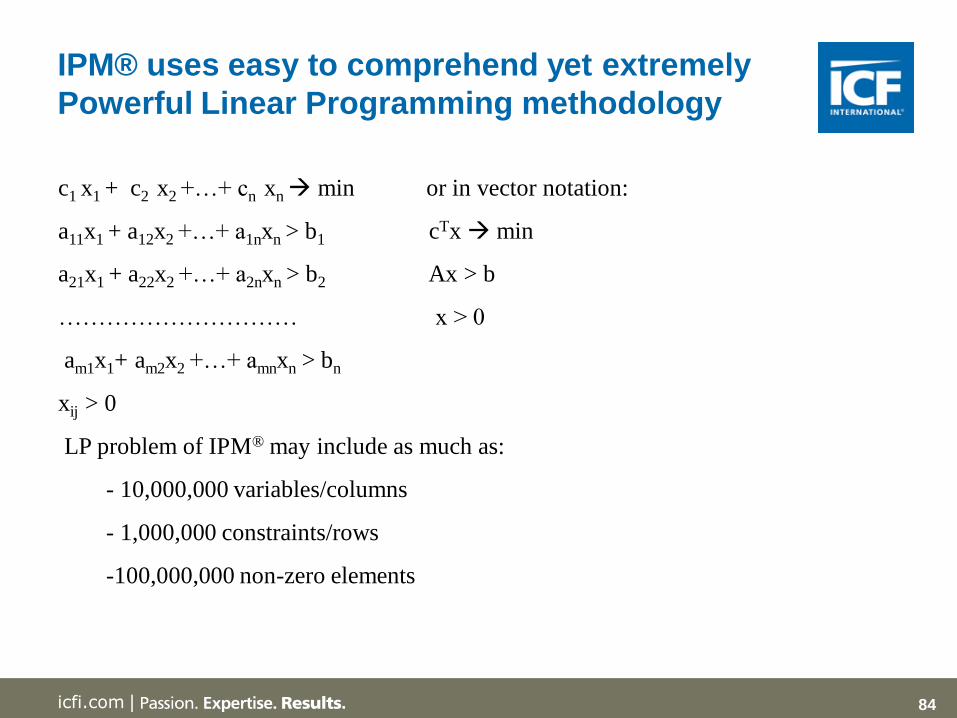

IPM® uses easy to comprehend yet extremely

Powerful Linear Programming methodology

• Objective Function of IPM® is to minimize present value of the total

system costs and unserved load

• Major Types of Constraints in IPM® - Energy Constraints and Capacity

Constraints, Dispatch Constraints, Fuel Constraints, Environmental and

other constraints

• Cost Coefficients in Objective Function – Mathematical equations and

definitions of all constraints mentioned above are provided in Appendix

49icfi.com |

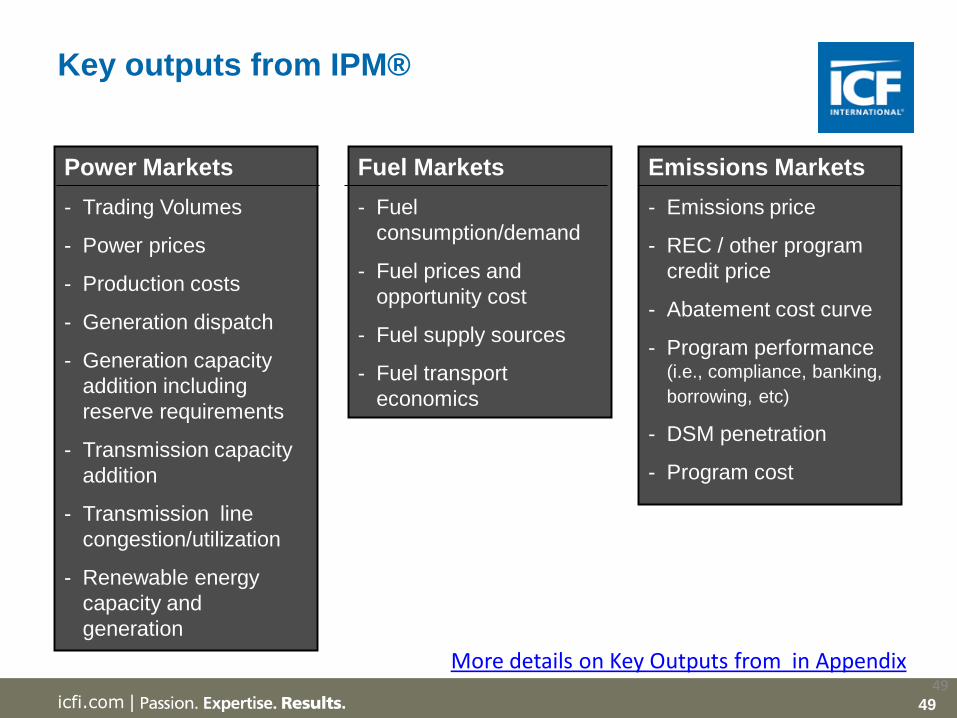

Power Markets

- Trading Volumes

- Power prices

- Production costs

- Generation dispatch

- Generation capacity

addition including

reserve requirements

- Transmission capacity

addition

- Transmission line

congestion/utilization

- Renewable energy

capacity and

generation

Fuel Markets

- Fuel

consumption/demand

- Fuel prices and

opportunity cost

- Fuel supply sources

- Fuel transport

economics

Emissions Markets

- Emissions price

- REC / other program

credit price

- Abatement cost curve

- Program performance (i.e., compliance, banking,

borrowing, etc)

- DSM penetration

- Program cost

Key outputs from IPM®

49

More details on Key Outputs from in Appendix

50icfi.com |

India - Key assumptions for IPM modeling

51icfi.com |

Indian economy expected to show strong recovery

YearICF

assumption

2014 5.50%

2015 6.30%

2016 6.60%

2017 6.88%

2018 7.16%

2019 7.44%

2020 7.72%

2021 onwards 8.00%

Average (2014-2031) 7.53%

Indian economy expected to recover in next fewyears on the back of strong reform agenda of thecurrent Government.

A high growth of ~8% is being targeted by Indiangovernment with the objective of reducing thepoverty levels significantly by 2050

In the long-term, the Planning Commission ofIndia targets Indian economy to reach andstabilize at a GDP growth rate of ~8%. The WorldBank has also estimated the long term GDPgrowth of India to remain ~8%.

India was able to sustain high GDP growth ratesin past on the back of strong reform measurestaken by the Government during that period.Same measures are expected from the currentGovernment.

52icfi.com |

Electricity Demand growth of 6.65% is expected during 2014-31 period

2014 to 2031 – average demand growth rate of 6.65% against average GDP growth of 7.53% assuming a constant energy elasticity of 0.89

By 2031, per capita consumption reaches 2,200 kWh/person which is similar to that of Eastern European countries

53icfi.com |

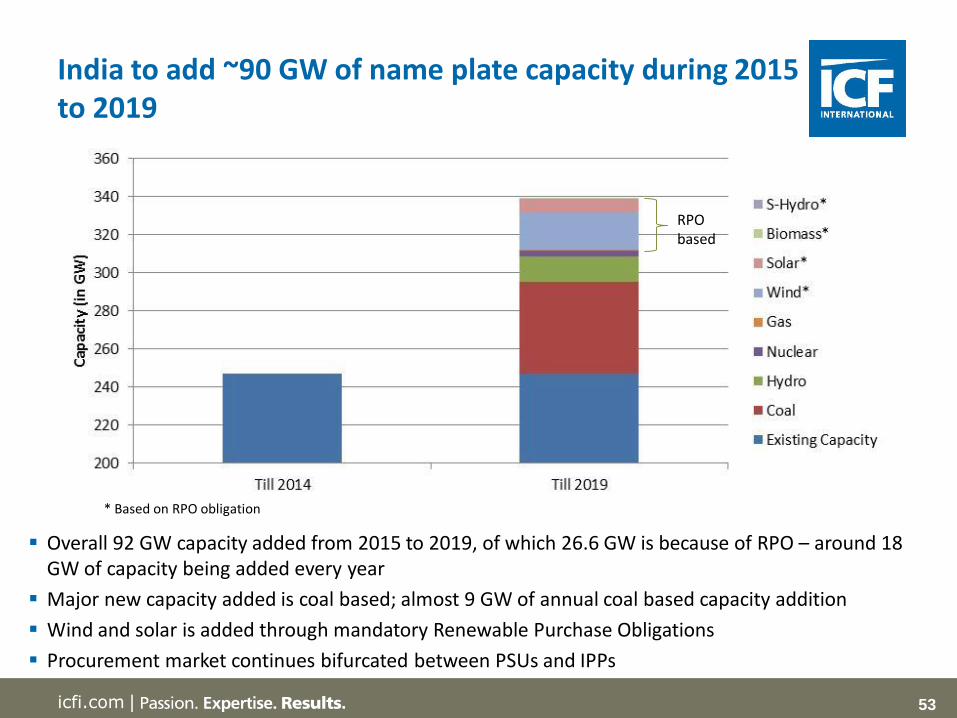

India to add ~90 GW of name plate capacity during 2015 to 2019

RPO based

* Based on RPO obligation

Overall 92 GW capacity added from 2015 to 2019, of which 26.6 GW is because of RPO – around 18 GW of capacity being added every year

Major new capacity added is coal based; almost 9 GW of annual coal based capacity addition

Wind and solar is added through mandatory Renewable Purchase Obligations

Procurement market continues bifurcated between PSUs and IPPs

54icfi.com |

Firm hydro capacity additions (2015 to 2019)

State Capacity

NR 5.7

SR 0.6

WR 0.6

NER 2.6

ER 3.1

Total 12.7

800 MW (RoR: 5 (800 MW))

2,500 MW (RoR: 10 (1,800 MW); Storage: 3 (700 MW))

2,400 MW (RoR: 11 (2000 MW); Storage: 2 (400 MW))

55icfi.com |

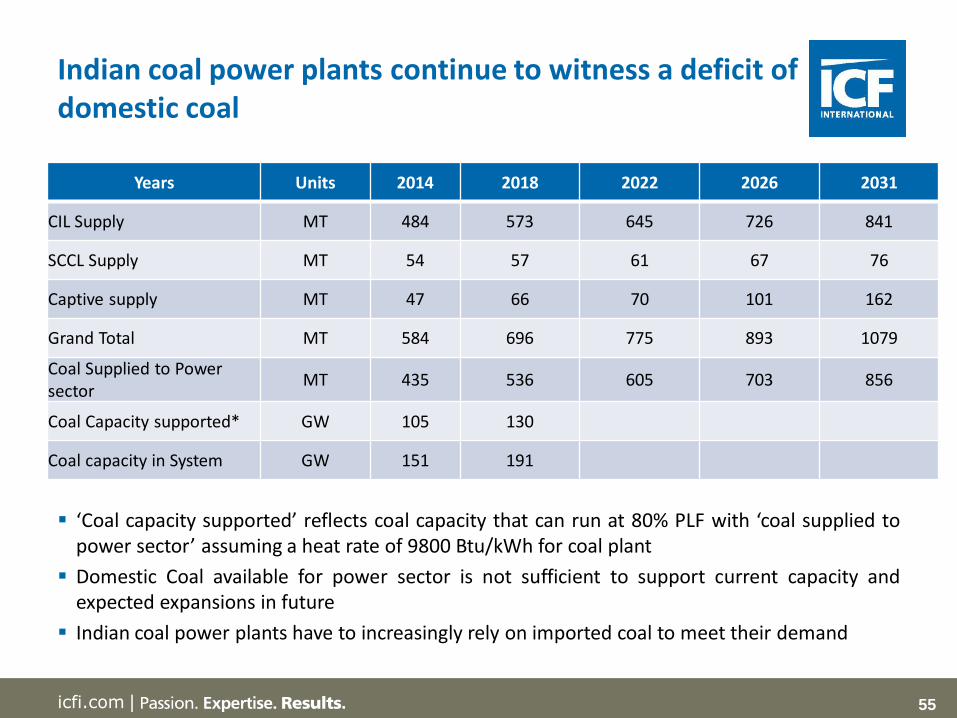

Indian coal power plants continue to witness a deficit of domestic coal

Years Units 2014 2018 2022 2026 2031

CIL Supply MT 484 573 645 726 841

SCCL Supply MT 54 57 61 67 76

Captive supply MT 47 66 70 101 162

Grand Total MT 584 696 775 893 1079

Coal Supplied to Power sector

MT 435 536 605 703 856

Coal Capacity supported* GW 105 130

Coal capacity in System GW 151 191

‘Coal capacity supported’ reflects coal capacity that can run at 80% PLF with ‘coal supplied topower sector’ assuming a heat rate of 9800 Btu/kWh for coal plant

Domestic Coal available for power sector is not sufficient to support current capacity andexpected expansions in future

Indian coal power plants have to increasingly rely on imported coal to meet their demand

56icfi.com |

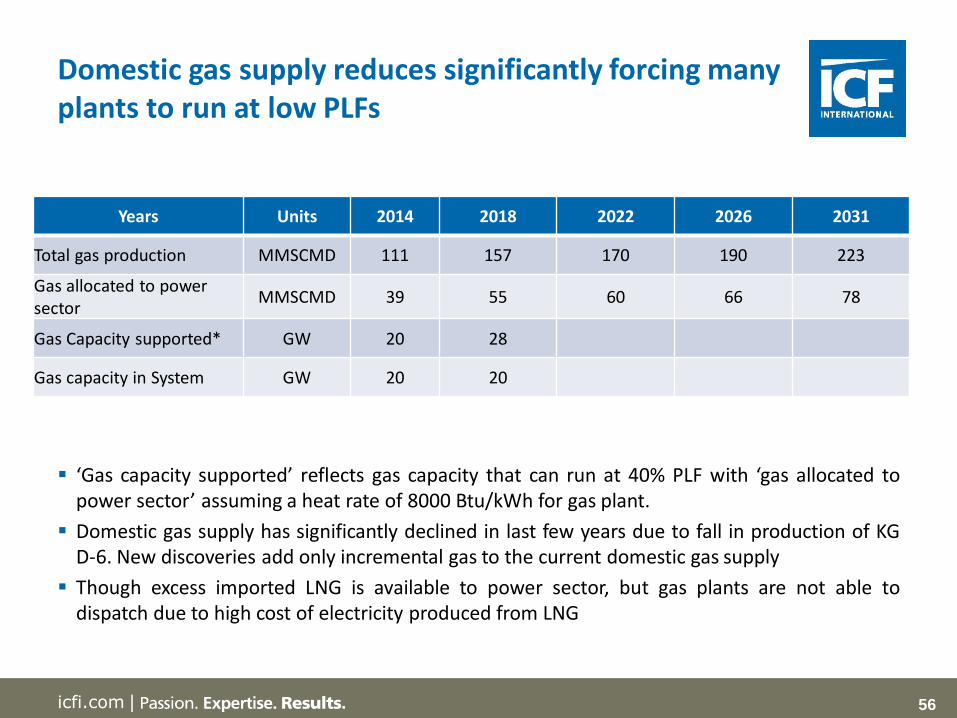

Domestic gas supply reduces significantly forcing many plants to run at low PLFs

Years Units 2014 2018 2022 2026 2031

Total gas production MMSCMD 111 157 170 190 223

Gas allocated to power sector

MMSCMD 39 55 60 66 78

Gas Capacity supported* GW 20 28

Gas capacity in System GW 20 20

‘Gas capacity supported’ reflects gas capacity that can run at 40% PLF with ‘gas allocated topower sector’ assuming a heat rate of 8000 Btu/kWh for gas plant.

Domestic gas supply has significantly declined in last few years due to fall in production of KGD-6. New discoveries add only incremental gas to the current domestic gas supply

Though excess imported LNG is available to power sector, but gas plants are not able todispatch due to high cost of electricity produced from LNG

57icfi.com |

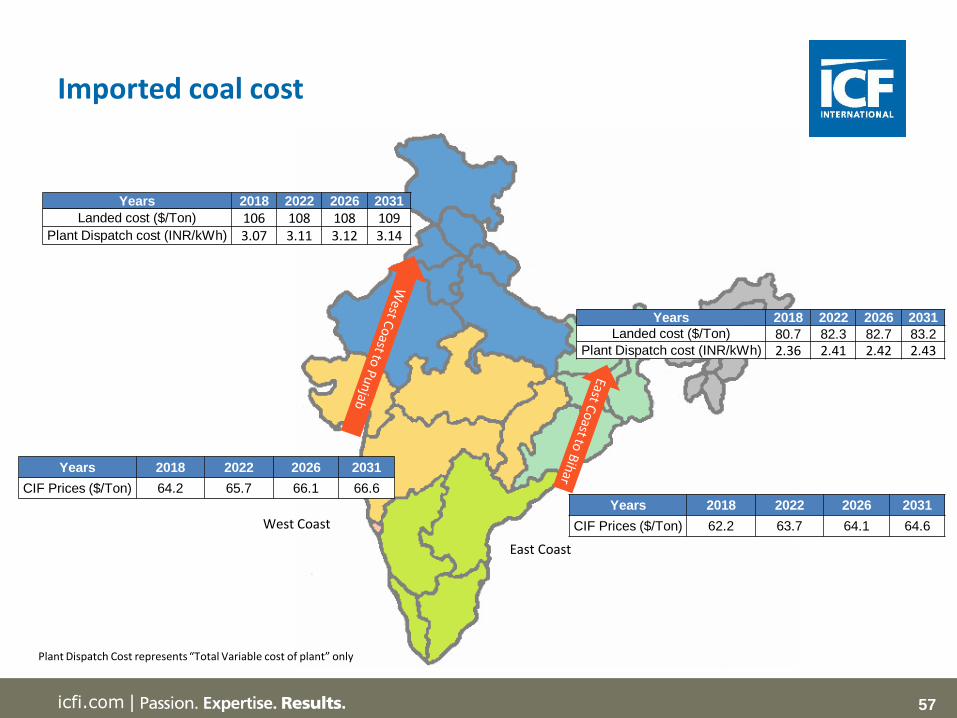

Imported coal cost

Years 2018 2022 2026 2031

CIF Prices ($/Ton) 62.2 63.7 64.1 64.6

Years 2018 2022 2026 2031

Landed cost ($/Ton) 80.7 82.3 82.7 83.2

Plant Dispatch cost (INR/kWh) 2.36 2.41 2.42 2.43

Years 2018 2022 2026 2031

CIF Prices ($/Ton) 64.2 65.7 66.1 66.6

Years 2018 2022 2026 2031

Landed cost ($/Ton) 106 108 108 109Plant Dispatch cost (INR/kWh) 3.07 3.11 3.12 3.14

East Coast

West Coast

Plant Dispatch Cost represents “Total Variable cost of plant” only

58icfi.com |

Domestic gas prices ($/MMBtu)

Tamil Nadu 2018 2022 2026 2031

Delivered cost (USD/MMBtu) 6.66 9.19 12.44 16.50Plant Dispatch cost (INR/kWh) 3.24 4.41 5.92 7.81

Delhi 2018 2022 2026 2031

Delivered cost (USD/MMBtu) 6.84 9.37 12.62 16.68Plant Dispatch cost (INR/kWh) 3.32 4.50 6.00 7.89Gujarat 2018 2022 2026 2031

Delivered cost (USD/MMBtu) 6.28 8.80 12.05 16.11Plant Dispatch cost (INR/kWh) 3.06 4.23 5.74 7.63

Maharashtra 2018 2022 2026 2031

Delivered cost (USD/MMBtu) 6.24 8.77 12.02 16.08Plant Dispatch cost (INR/kWh) 3.05 4.22 5.73 7.61

Andhra Pradesh 2018 2022 2026 2031

Delivered cost (USD/MMBtu) 6.15 8.68 11.93 15.99Plant Dispatch cost (INR/kWh) 3.00 4.18 5.68 7.57

Plant Dispatch Cost represents “Total Variable cost of plant” only

59icfi.com |

India – IPM Modeling Results

60icfi.com |

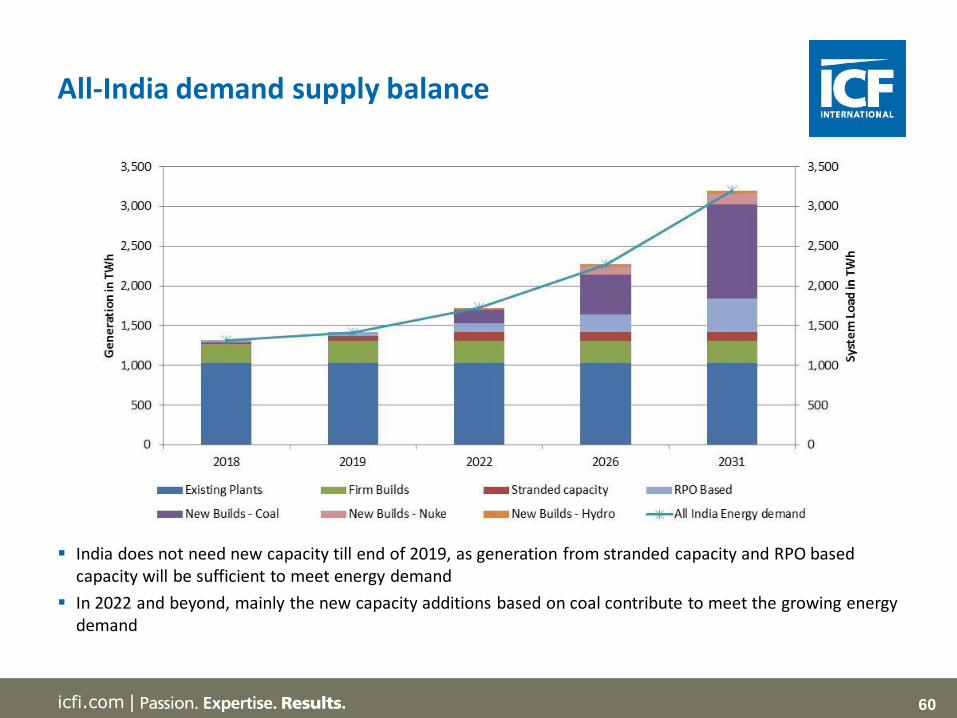

All-India demand supply balance

India does not need new capacity till end of 2019, as generation from stranded capacity and RPO based capacity will be sufficient to meet energy demand

In 2022 and beyond, mainly the new capacity additions based on coal contribute to meet the growing energy demand

61icfi.com |

Share of Imported coal based generation reaches ~36% in 2031

In long-term, generation from imported coal is expected to play an important role in meeting increasing demand of system

Of the total coal generation in the system, generation from imported coal contributes ~36% by 2031

Generation from RE sources (Wind, Solar, Small-Hydro and biomass) are primarily driven by RPO

62icfi.com |

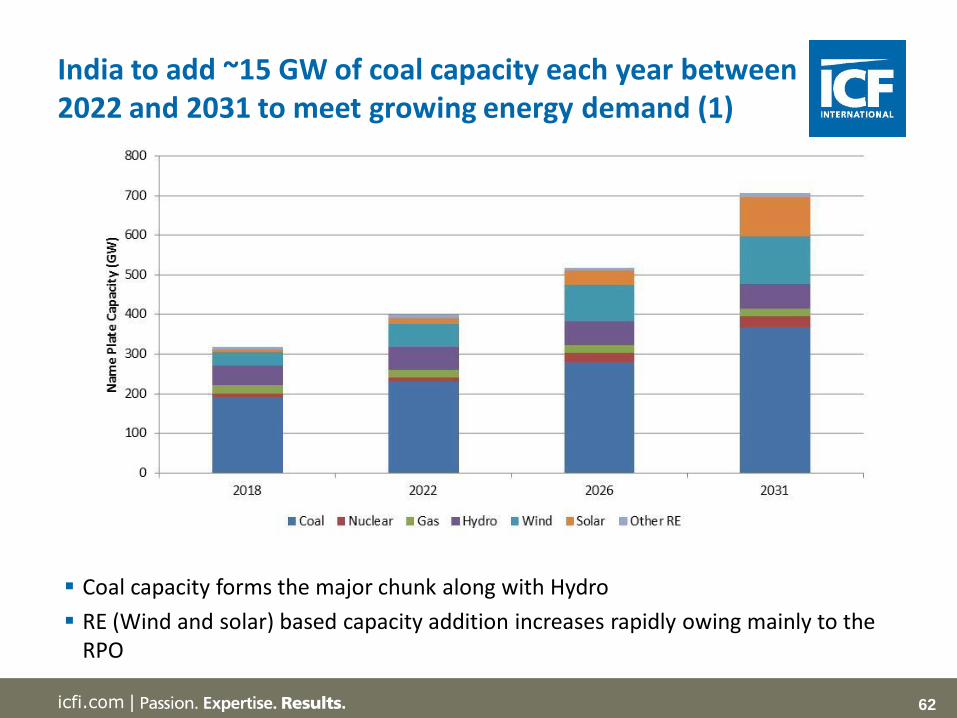

India to add ~15 GW of coal capacity each year between 2022 and 2031 to meet growing energy demand (1)

Coal capacity forms the major chunk along with Hydro

RE (Wind and solar) based capacity addition increases rapidly owing mainly to the RPO

63icfi.com |

India to add ~15 GW of coal capacity each year between 2022 and 2031 to meet growing energy demand (2)

India needs to add just 15 GW of coal capacity every year which should be fairly achievable given that India is already adding similar coal capacities every year

As such there may not be any capacity constraints going forward in the system as witnessed in 2007-2010 period

in GW 2018 2022 2026 2031

Coal 191 230 279 367

Nuclear 9.2 9.9 23 28

Gas 20 20 20 20

Hydro 50 57 60 62

Wind 34 58 91 119

Solar 6.5 16.5 37 100

Other RE 7.2 7.2 7.3 10

Total 318 399 518 706

64icfi.com |

Year 2022Capacity

FactorHeat Rate

Non-Fuel Variable cost

Fuel Cost

Total Variable cost

Fixed costTotal Fixed

costTotal Cost

(Variable &Fixed)

Units % Btu /kWh INR/ kWhINR/ kWh

INR/ kWh INR/ kW-yr INR/ kWh INR/ kWh

Existing Coal Plant -Domestic

80% 9,500 0.13 0.97 1.10 2800 0.40 1.50

New Coal Plant -Domestic

80% 9,200 0.13 0.94 1.07 8224 1.17 2.24

Existing Coal Plant -Imported

80% 9,500 0.13 2.78 2.91 2800 0.40 3.31

New Coal Plant -Imported

80% 9,200 0.13 2.69 2.82 8224 1.17 3.99

Existing Gas Plant -Domestic

40% 8,000 0.11 5.06 5.17 2550 0.73 5.90

New Gas Plant -Domestic

40% 7,500 0.11 4.75 4.86 7940 2.27 7.12

New Wind 25% 0 0.01 0.00 0.01 7651 3.49 3.50

New Solar 24% 0 0.01 0.00 0.01 8763 4.25 4.26

New Hydro - RoR 40% 0 0.01 0.00 0.01 13775 3.93 3.94

New Hydro - Storage 45% 0 0.01 0.00 0.01 16530 4.19 4.20

All in generation cost of new imported coal based plant to drive overall market prices

In 2022, the new coal based plant running on imported coal will be at margin with an all inclusive cost of generation of ~ Rs 4.0 per kWh

65icfi.com |

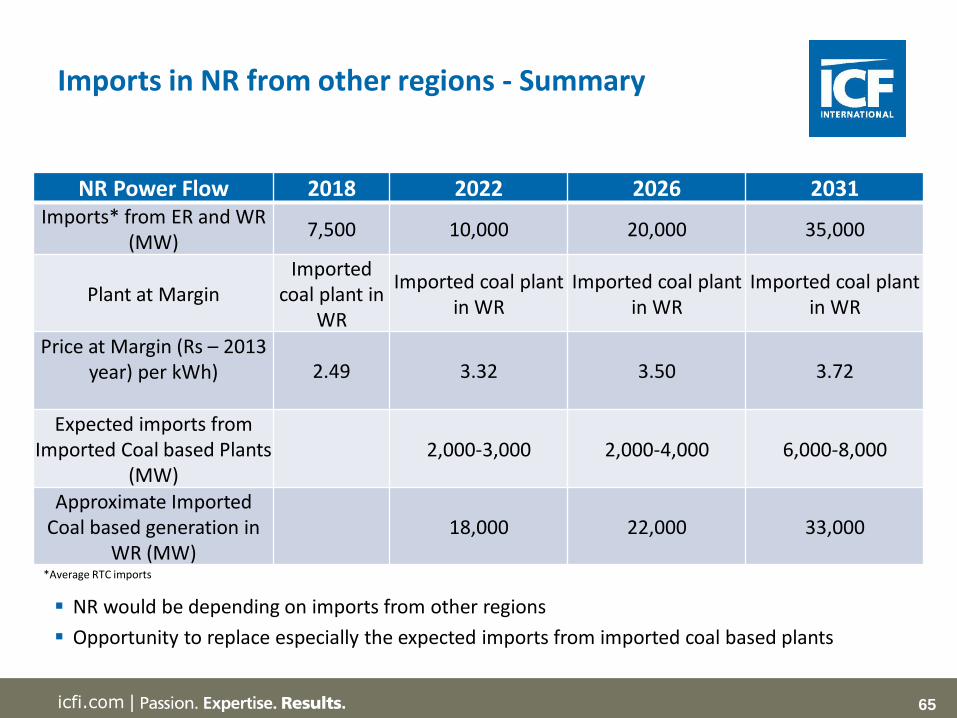

NR would be depending on imports from other regions

Opportunity to replace especially the expected imports from imported coal based plants

Imports in NR from other regions - Summary

NR Power Flow 2018 2022 2026 2031Imports* from ER and WR

(MW)7,500 10,000 20,000 35,000

Plant at MarginImported

coal plant in WR

Imported coal plant in WR

Imported coal plant in WR

Imported coal plant in WR

Price at Margin (Rs – 2013 year) per kWh) 2.49 3.32 3.50 3.72

Expected imports from Imported Coal based Plants

(MW)2,000-3,000 2,000-4,000 6,000-8,000

Approximate Imported Coal based generation in

WR (MW)18,000 22,000 33,000

*Average RTC imports

66icfi.com |

Northern Region is a major importer from the Eastern and Western region

The prices in NR will be in the range of INR 3.25-3.50 per KWh in year 2022 with the possibilityof additional benefit due to congestion charges in later years

Assumptions suggest that it is economical to generate at pithead and transmit electricity ratherthan transporting coal to the load centre. This indicates heavy reliance on timely constructionof transmission capacities – both planned and unplanned

• Development of transmission links is key

Imported Coal remains the marginal fuel and with large capacity additions, it removes anyseasonality caused by hydro supply

• Coal based capacity addition is unlikely to be a constraint

There is hardly any difference in the seasonal pricing due to (i) flattening load profile, and (ii)coal capacity additions based on imported coal

It appears unlikely that there will be any peaking power market in India in the near future

• Prices are unlikely to change unless the nature of the demand curve changes

Key Insights

67icfi.com |

In the short term, the Trading potential exists between India-Nepal, India-Bhutan and

India-Bangladesh based on the seasonality of demand. ICF is in the process of

collecting load profile data from all the countries which would form the basis for

calculating short term trading potential.

In the longer term, the setting up of new capacities can be avoided by the countries if

there is a potential of buying power from other countries. However this would be

subject to constraints on transmission, resource availability and the power prices in

each market.

ICF is in the process of populating the integrated resource model for South Asia region

using its proprietary IPM® model for calculating the actual trading potential.

Way Forward

68icfi.com |

ICF has developed the data sheet for capturing information and assumptions from each

country. ICF along with IRADe team is following up to capture this information

IPM® database has been already populated with Indian power sector database. The

data from each of remaining South Asian nations would be populated to make the Base

case

For the Base case, the IPM® run would be set up to calculate the year wise trading

potential between each the South Asian countries. In this case, no transmission

constraint is considered between any countries. In fact, the required cross border

transmission required would be the output of the model

For the Changed case, actual transmission would be built in the base model. New runs

would be subsequently executed.

Way Forward (cntd.)

69icfi.com |

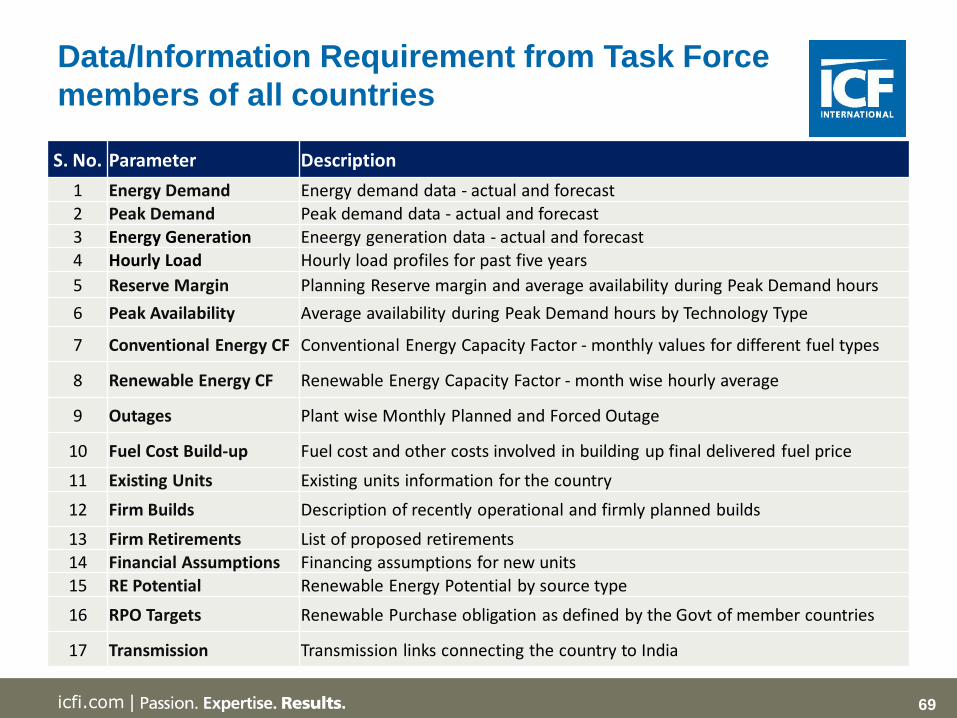

Data/Information Requirement from Task Force

members of all countries

S. No. Parameter Description

1 Energy Demand Energy demand data - actual and forecast

2 Peak Demand Peak demand data - actual and forecast

3 Energy Generation Eneergy generation data - actual and forecast

4 Hourly Load Hourly load profiles for past five years

5 Reserve Margin Planning Reserve margin and average availability during Peak Demand hours

6 Peak Availability Average availability during Peak Demand hours by Technology Type

7 Conventional Energy CF Conventional Energy Capacity Factor - monthly values for different fuel types

8 Renewable Energy CF Renewable Energy Capacity Factor - month wise hourly average

9 Outages Plant wise Monthly Planned and Forced Outage

10 Fuel Cost Build-up Fuel cost and other costs involved in building up final delivered fuel price

11 Existing Units Existing units information for the country

12 Firm Builds Description of recently operational and firmly planned builds

13 Firm Retirements List of proposed retirements

14 Financial Assumptions Financing assumptions for new units

15 RE Potential Renewable Energy Potential by source type

16 RPO Targets Renewable Purchase obligation as defined by the Govt of member countries

17 Transmission Transmission links connecting the country to India

70icfi.com |

Appendix

Electricity Shortages in India

Details on ICF’s Integrated Planning Model (IPM®)

Key outputs from IPMM®

Mathematical details on Modeling framework

71icfi.com |

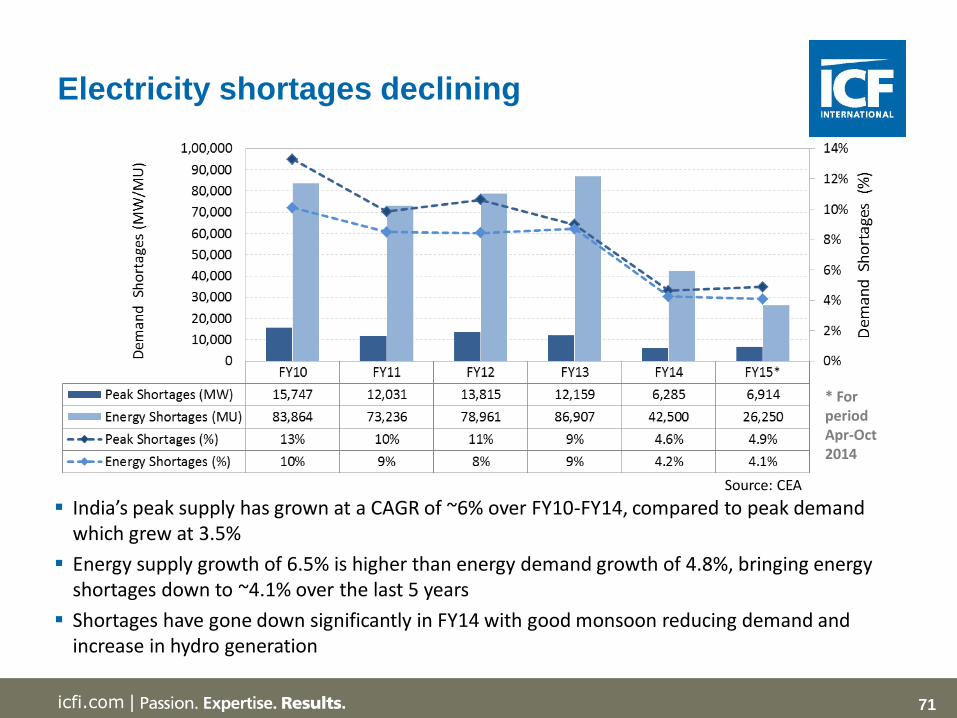

Electricity shortages declining

* For period Apr-Oct 2014

India’s peak supply has grown at a CAGR of ~6% over FY10-FY14, compared to peak demand which grew at 3.5%

Energy supply growth of 6.5% is higher than energy demand growth of 4.8%, bringing energy shortages down to ~4.1% over the last 5 years

Shortages have gone down significantly in FY14 with good monsoon reducing demand and increase in hydro generation

Source: CEA

72icfi.com |

Plant Load Factors Witnessed an Overall Decline

(Source: CEA)

All India PLF* FY13 FY14 FY15

April 75.24 69.97 69.38

May 74.45 71.55 68.15

June 72.24 63.4 68.01

July 66.96 60.86 64.87

August 61.58 55.94 60.83

September 61.41 64.65 60.86

October 71.04 61.85 65.93

November 71.02 65.44

December 72.41 69.05

January 74.33 69.82

February 70.67 68.44

March 71.96 66.58

Annual 70.28 65.63 65.35

* For Coal and Lignite Based Plants

Aggregate PLF for the gas based plants declined primarily due gas supply shortage

PLFs of coal based power plants declined due to

Accelerated capacity addition coupled with lower demand growth

lower coal availability for each MW in system

transmission constraints in W3 region which made dispatch of coal plants difficult

Despite the decline, generation overall increase in generation was enough to reduce shortages

73icfi.com |

Overall short term market is around 7% - 8% of the total supply

Share of bilaterally bought power has increased from ~2.6% to ~5.5% over the last few years

Share of exchange traded power has increased from ~0.4% to ~3% in the same period

Remaining energy has been met through long term PPAs and the UI balancing market

Depth of short term market (Bilateral and

Exchange Markets) is increasing

Share of Bilateral, Exchange and Long Term + UI in Energy Met

* FY15 Data till September 2014 Source: CERC

8% only

Back to India Electricity D-S

74icfi.com |

IPM® has evolved over 30 years of helping evaluate

complex energy, fuel and environmental markets

1970s: Started as Coal Electric Utility Model (CEUM) to support US Clean Air Act (CAA) regulations

1980s: Expanded to IPM® after complete power sector integrated to support US Environmental Protection Agency (EPA) in CAA rule making

1990s: Model used in building several utilities with integrated resource planning, including DSM

1990s: Model used to support EPA with CAA Amendments, cap-and-trade program for NOx, SOx and later mercury regulation; main modeling framework used by EPA in environmental planning for power sector

1990s: Used by US Federal Regulatory Electricity Commission for rule making

2000s: Widely used by states and regional agencies in power, environmental and renewable energy program development (e.g., western states renewable energy portfolio, regional haze, western climate initiative; midwest regional greenhouse gas initiative)

2000s: Widely used for power market forecasting, correctly used in forecast California power market crash and mid-west over build price crash

2000s: Widely used to support GHG analyses of power and non power sectors

2004: ICF launched the India Integrated Planning Model (I-IPM®); supported clients in evaluating Indian power sector fundamentals

75icfi.com |

Licensed by leading power companies for

power market analysis

MidAmerican Energy

Pacificorp

Exelon

Nyserda

International Power

BP

Polish Power and Generation Company

76icfi.com |76

ICF India Engagements in Asia-Pacific and

international fuel market

India:

• Power Market Study

• Power Sale Strategy

• Renewable market study and

analysis

• Technical Due Diligence for Coal Plant

• Asset Valuation

• Coal Mine Valuation

• Transmission & Evacuation

Strategy

• Gas Market Analysis

• Natural Gas Grid Design

Sri Lanka

• Power & Gas Market Assessment

Nepal:

• Transmission & Evacuation

Strategy

China:

• Power Market Analysis

Singapore:

• Asset Valuation

• Power Market Analysis

Vietnam:

• Power & Gas Market Analysis

South Korea:

• Power Market Analysis

• GHG Mitigation Strategy

Australia:

• Power Sale Strategies for Wind

• REC Price forecast and sales

strategy

• Carbon Price Forecast

• Asset Valuation

• Power Market Analysis

Bangladesh:

• Energy Efficiency and

Management

Philippines:

• Asset Valuation

• Power Market Analysis

Indonesia:

• Power Market Analysis

• Marginal Abatement Cost Curves

(MACC) for Power Sector

Japan:

• Power Market Analysis

ICF has helped support over $40 billion of power plant financing around the world

77icfi.com |

Model Components

Optimization/Simulation ENGINE

Data Base

Other Tools and

Data Bases

Transmission Flow Model

Demand Forecasting

Tool

Analyst 1

Output –Excel and text files

Analyst 2

Graphical Interface Front

End

78icfi.com |

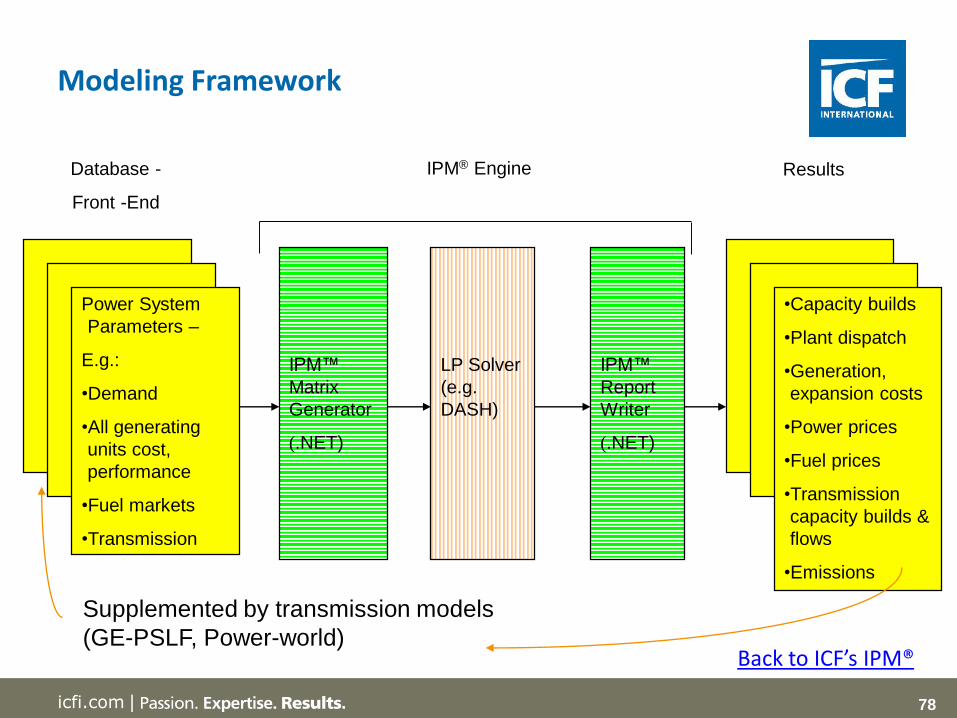

Modeling Framework

Power System

Parameters –

E.g.:

•Demand

•All generating

units cost,

performance

•Fuel markets

•Transmission

Database -

Front -End

IPM™

Matrix

Generator

(.NET)

LP Solver

(e.g.

DASH)

IPM™

Report

Writer

(.NET)

IPM® Engine

•Capacity builds

•Plant dispatch

•Generation,

expansion costs

•Power prices

•Fuel prices

•Transmission

capacity builds &

flows

•Emissions

Results

Supplemented by transmission models

(GE-PSLF, Power-world)Back to ICF’s IPM®

79icfi.com |

Power Price forecast reflects operational considerations, system dynamics and market fundamentals

Prices based on marginal cost with merit order dispatch

Simultaneously available for all states regions and at regional and national level

Available for all hours and years of the planning horizon

Plant specific generation costs can be used to derive “cost plus” regulated price

Segmental prices mapped to chronological hourly prices

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020P

ow

er

Pri

ces

(No

min

al R

s./k

Wh

)

Round The Clock Peak Prices Off-Peak Price

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Pow

er P

rice

s (N

omin

al R

s./k

Wh)

Round The Clock Peak Prices Off-Peak Price

Illustrative wholesale forward power price curves – National Level

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

-

5,000

10,000

15,000

20,000

25,000

1 201 401 601 801 1001 1201 1401 1601 1801 2001

Pri

ce (R

s./k

Wh

)

Load

(MW

)

Hour

Illustrative Load Duration and Price Duration Curve for Winter –Maharashtra (2013)

Detailed power price forecast

80icfi.com |

Detailed results on dispatch, merit order and marginal prices

0

1

2

3

4

5

6

7

8

0 50 100 150 200 250

Dis

pa

tch

Co

st (R

s./k

Wh

)

Cumulative Capacity (GW)

System - 2010

CC

Potential Build CC-F

CT

Potential Build CT-LM

Potential Build Hydro

Hydro

PS

Potential Build Diesel

Oil

Potential Build Nuclear

Nuclear

Potential Build Small Hydro

Small Hydro

Potential Build Wind

Wind

Retierment

Potential Build Biomass

Biomass

Potential Build Coal

Coal

Retrofit Coal0

1

2

3

4

5

6

7

8

9

0 50 100 150 200 250 300

Dis

pa

tch

Co

st (R

s./k

Wh

)

Cumulative Capacity (GW)

System - 2015

CC

Potential Build CC-F

CT

Potential Build CT-LM

Potential Build Hydro

Hydro

PS

Potential Build Diesel

Oil

Potential Build Nuclear

Nuclear

Potential Build Small Hydro

Small Hydro

Potential Build Wind

Wind

Retierment

Potential Build Biomass

Biomass

Potential Build Coal

Coal

Retrofit Coal

All India Dispatch Stack - Illustrative for Year 2010 All India Dispatch Stack - Illustrative for Year 2015

Oil

CC & CT

Coal

Hydro, Renewables and Nuclear

Oil

CC & CT

Coal

Hydro, Renewables and Nuclear

Shortages,Shortages,

81icfi.com |

Transmission flows and Energy transfers available

for all lines and years of planning horizon

Forecast based on I-IPM®. India Wholesale Power Outlook 2005

82icfi.com |

Transmission congestion can be forecasted for

all the years of planning horizon

1

8760

Hours

BI

WB

OR

AP

MH

MP

CH

UP

JH

91

Illustrative Line Congestion in Peak

segments (2011)

Illustrative transmission line

utilization under various

seasons – OR to AP (2011)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43

Tran

smis

sio

n C

orr

ido

r U

tiliz

atio

n (

%)

Forecast based on I-IPM. India Wholesale Power Outlook 2005

1

2008 2010 2013 2016 2020

Weighted Average % of Hours Congested

WESTERN EASTERN

SOUTHERN

NORTHERN

55.28 61.48 56.64 77.79 80.29

21.83 21.09 18.82 19.37 27.90

52.31 65.15 67.43 47.69 86.06

WESTERN EASTERN

SOUTHERN

NORTHERN

55.28 61.48 56.64 77.79 80.2955.28 61.48 56.64 77.79 80.29

21.83 21.09 18.82 19.37 27.9021.83 21.09 18.82 19.37 27.90

52.31 65.15 67.43 47.69 86.0652.31 65.15 67.43 47.69 86.06

83icfi.com |

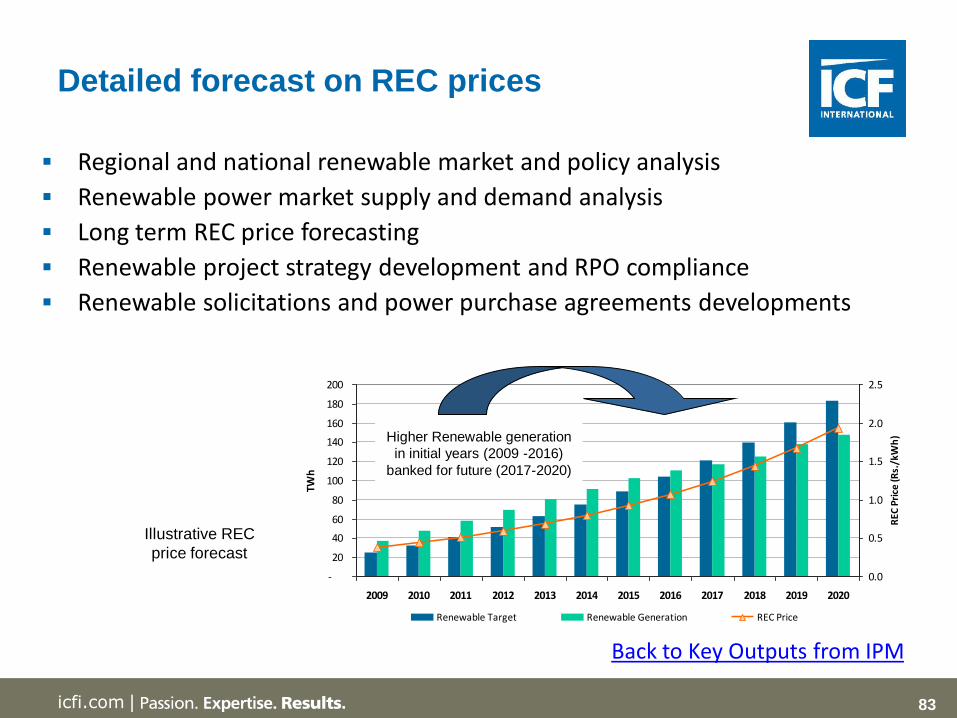

Detailed forecast on REC prices

-

20

40

60

80

100

120

140

160

180

200

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

TWh

0.0

0.5

1.0

1.5

2.0

2.5

REC

Pri

ce (R

s./k

Wh

)

Renewable Target Renewable Generation REC Price

Illustrative REC

price forecast

Regional and national renewable market and policy analysis

Renewable power market supply and demand analysis

Long term REC price forecasting

Renewable project strategy development and RPO compliance

Renewable solicitations and power purchase agreements developments

Higher Renewable generation

in initial years (2009 -2016)

banked for future (2017-2020)

Back to Key Outputs from IPM

84icfi.com |

IPM® uses easy to comprehend yet extremely

Powerful Linear Programming methodology

c1 x1 + c2 x2 +…+ cn xn min or in vector notation:

a11x1 + a12x2 +…+ a1nxn > b1 cTx min

a21x1 + a22x2 +…+ a2nxn > b2 Ax > b

………………………… x > 0

am1x1+ am2x2 +…+ amnxn > bn

xij > 0

LP problem of IPM® may include as much as:

- 10,000,000 variables/columns

- 1,000,000 constraints/rows

-100,000,000 non-zero elements

85icfi.com |

Objective Function of IPM®

MIN )1(**_

....

1**cos_*capacity

1*cos_*_*generation1**capacity

)1(

_

_ _

)1(

)1()1(

ynss

season

nbb

segment

ontransmissicontractsprogramsDSM

buildnew lifebook

y

year plant season segment fuel

yy

dVLLloadunserved

dccrtinvestment

dVOMtfuelrateheatdFOM

Minimize present value of the total system costs and

unserved load

86icfi.com |

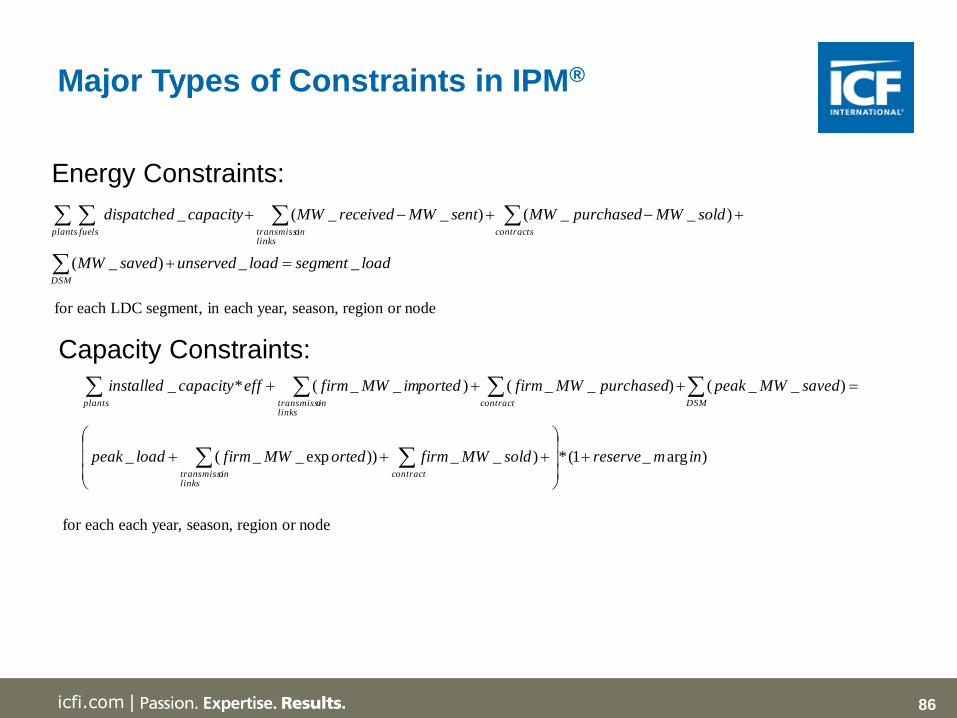

Major Types of Constraints in IPM®

Energy Constraints:

DSM

contractsplantslinks

ontransmissifuels

loadsegmentloadunservedsavedMW

soldMWpurchasedMWsentMWreceivedMWcapacitydispatched

__)_(

)__()__(_

for each LDC segment, in each year, season, region or node

Capacity Constraints:

)arg_1(*)__))exp__(_

)__()__()__(*_

inmreservesoldMWfirmortedMWfirmloadpeak

savedMWpeakpurchasedMWfirmimportedMWfirmeffcapacityinstalled

contractlinks

ontransmissi

DSMcontractplantslinks

ontransmissi

for each each year, season, region or node

87icfi.com |

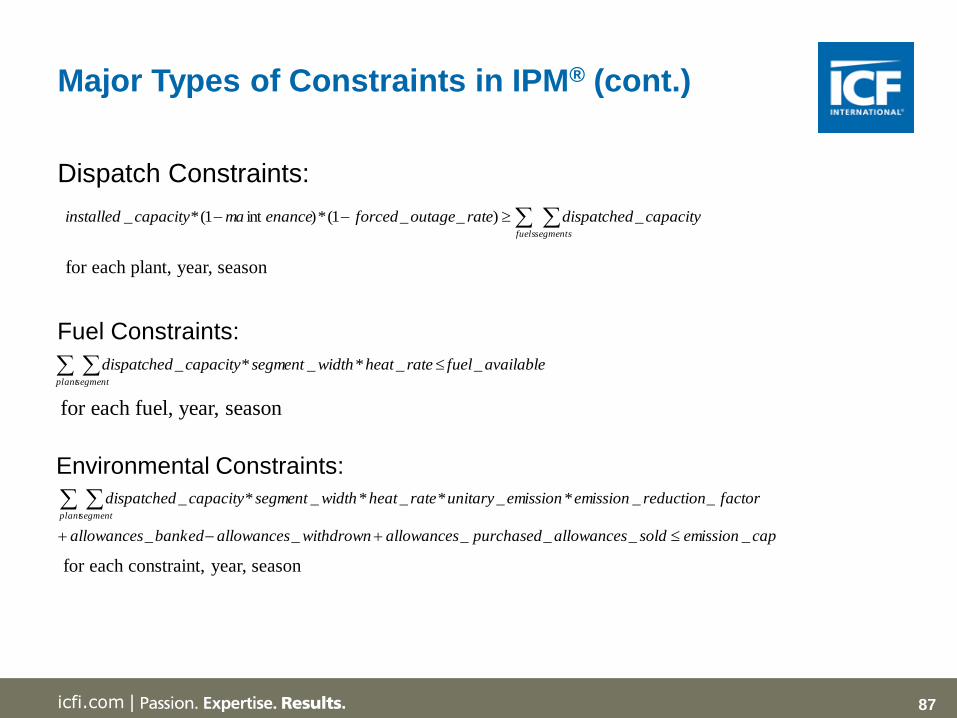

Major Types of Constraints in IPM® (cont.)

Fuel Constraints:

availablefuelrateheatwidthsegmentcapacitydispatchedplantsegment

__*_*_

for each fuel, year, season

Environmental Constraints:

for each constraint, year, season

capemissionsoldallowancespurchasedallowanceswithdrownallowancesbankedallowances

factorreductionemissionemissionunitaryrateheatwidthsegmentcapacitydispatchedplantsegment

______

__*_*_*_*_

Dispatch Constraints:

fuelssegments

capacitydispatchedrateoutageforcedenancemacapacityinstalled _)__1(*)int1(*_

for each plant, year, season

88icfi.com |

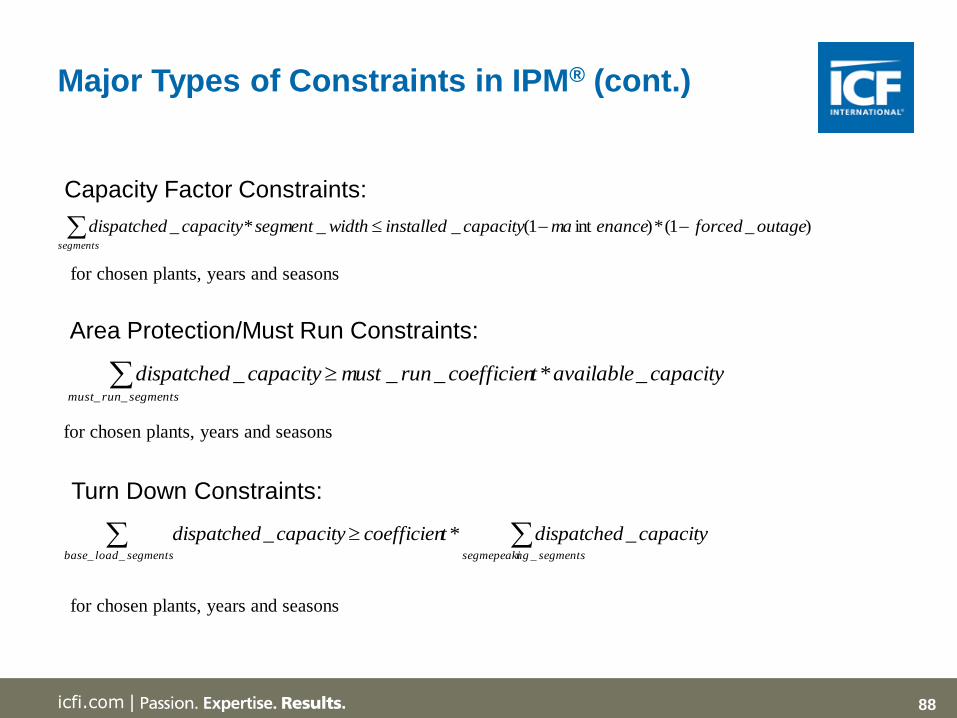

Major Types of Constraints in IPM® (cont.)

Capacity Factor Constraints:

segments

outageforcedenancemacapacityinstalledwidthsegmentcapacitydispatched )_1(*)int1(__*_

for chosen plants, years and seasons

Area Protection/Must Run Constraints:

segmentsrunmust

capacityavailabletcoefficienrunmustcapacitydispatched__

_*___

for chosen plants, years and seasons

Turn Down Constraints:

segmentsloadbase segmentsngsegmepeaki

capacitydispatchedtcoefficiencapacitydispatched__ _

_*_

for chosen plants, years and seasons

89icfi.com |

Cost Coefficients in Objective Function

Variable cost coefficients – assigned to dispatch operates

1))(1(

1*

)),(),(cos_(*),,s,(

),,,(

year

mappedyears yeardiscseasonfueladderyearfueltfuelyearseasonegmentplantHR

yearseasonsegmentplantVOM

horizontime

yearyeardiscyearplantCCRyearplanttCapitalyearplantFOM

1))(1(

1*),(*),(cos_),(

Fixed cost coefficients – assigned to capacity vectors

),(_),(11

),(),(

yearplantlifebook)yearplantr(

yearplantryearplantCCR

where:

Back to Modeling Framework

90icfi.com |

![Leszek Orzechowski - architectus.arch.pwr.wroc.pl · Kardashev [1] while creating the scale of a civilisation’s technological advancement based on the amount of ener gy used. The](https://static.fdocument.pub/doc/165x107/5fc58f5bba184a381b18f4ba/leszek-orzechowski-kardashev-1-while-creating-the-scale-of-a-civilisationas.jpg)