1 FBD HOLDINGS PLC 2005 PRELIMINARY RESULTS. 2 Forward Looking Statements This presentation contains...

24

1 FBD HOLDINGS PLC 2005 PRELIMINARY RESULTS

-

Upload

bartholomew-carr -

Category

Documents

-

view

221 -

download

0

Transcript of 1 FBD HOLDINGS PLC 2005 PRELIMINARY RESULTS. 2 Forward Looking Statements This presentation contains...

1

FBD HOLDINGS PLC

2005 PRELIMINARY RESULTS

2

Forward Looking Statements

This presentation contains certain forward-looking statements. Actual results may differ materially from those projected or implied in such forward-looking statements. Such forward-looking information involves risks and uncertainties that could affect expected results

3

Introduction to FBD Holdings plc

• Core business …insurance underwriting. – leading position in target markets– strong brand identity

• Non – Core– property/leisure – financial services

• Excellent growth record.

4

Operational Highlights of 2005

Underwriting• Strong new business volumes more than offset reducing

premium rates.

• Policy count at 31st December 2005 up 12.5% on 2004 figure.

• Branch network enhanced.

• Dublin Market targeted

• New products introduced (Shops, Trades, Breakdown / Claims Assist 24 Hour service)

• Increased investment in infrastructure and human resources

5

Operational Highlights of 2005

Non-Underwriting

• 40 Residential units sold at La Cala Resort

• Third championship golf course (“The Europa”) opened for play at La Cala.

• Castlerosse Hotel, Killarney sold.

• Castleknock Hotel & Country Club opened.

6

Operational Highlights of 2005

Corporate

• KBC disposed of its 22% shareholding.

– FBD partakes in KBC sale…(€81m buyback) – Free float increased to 58%

7

Financial Highlights

2005 2004 %

€000s €000s

Gross written premiums 389,472 351,487 +10.8%

Net earned premiums 332,371 296,237 +12.2%

Underwriting result 90,450 65,939 +37.2%

Operating profit 162,624 124,724 +30.4%

Cent Cent

Operating earnings per share 363.54 256.18 +41.9%

Dividend per share 57.50 40.00 +43.75%

Net asset value per share 1,250.62 969.64 +29.0%

% %

Return on equity 36.53 31.61

8

Preliminary Results: Year to 31st December 2005Income Statement

2005 2004

€000s €000s %

Gross written premiums 389,472 351,487 +10.8%

Net earned premiums 332,371 296,237 +12.2%

Net claims incurred (202,475) (197,784) +2.4%

Net operating expenses (39,446) (32,514) +21.3%

Underwriting Result 90,450 65,939 +37.2%

Loss Ratio 60.9% 66.7%

Net Expense Ratio

Combined Ratio

11.9%

72.8%

11.0%

77.7%

9

Preliminary Results: Year to 31st December 2005Income Statement…. Contd.

162,624

27,739

134,885

162,624

27,739

44,435

90,450

€000s

2005

10,793

3,302

13,644

124,794

18,142

106,652

124,794

18,142

40,713

65,939

€000s

2004

3,651- Capital Fund

3,905- Financial Services

10,586- Property/Leisure

Non-Underwriting

Insurance Underwriting

Operating profit by activity

+30.3%Operating profit

+52.9%Non underwriting operating income

+9.1%Longer term investment return

+37.2%Underwriting Result

%

162,624

27,739

134,885

162,624

27,739

44,435

90,450

€000s

2005

10,793

3,302

13,644

124,794

18,142

106,652

124,794

18,142

40,713

65,939

€000s

2004

3,651- Capital Fund

3,905- Financial Services

10,586- Property/Leisure

Non-Underwriting

Insurance Underwriting

Operating profit by activity

+30.3%Operating profit

+52.9%Non underwriting operating income

+9.1%Longer term investment return

+37.2%Underwriting Result

%

10

Preliminary Results: Year to 31st December 2005Income Statement….. Contd.

2005 2004

€000s €000s

Operating profit 162,624 124,794

Short term fluctuation in investment return 25,956 10,298

Finance costs (3,425) (3,116)

Profit before tax 185,155 131,976

Income tax expense (23,701) (16,968)

Profit for the year 161,454 115,008

11

Preliminary Results: As at 31st December 2005Balance Sheet - Assets

31/12/05 31/12/04

Property & Equipment €000s €000s

Hotels/golf 168,258 148,582

Property – own use 28,665 27,935

Fixtures & Fittings 13,302 210,225 10,547 187,064

Investments

Property 48,856 24,200

Financial 1,061,846 999,080

Reinsurers’ share of technical provisions 66,034 65,765

Other receivables/DAC’s 73,058 68,825

Other Assets

Development land 36,163 34,105

Work-in-Progress 26,333 36,438

Cash 41,897 104,393 51,362 121,905

Total Assets 1,564,412 1,466,839

12

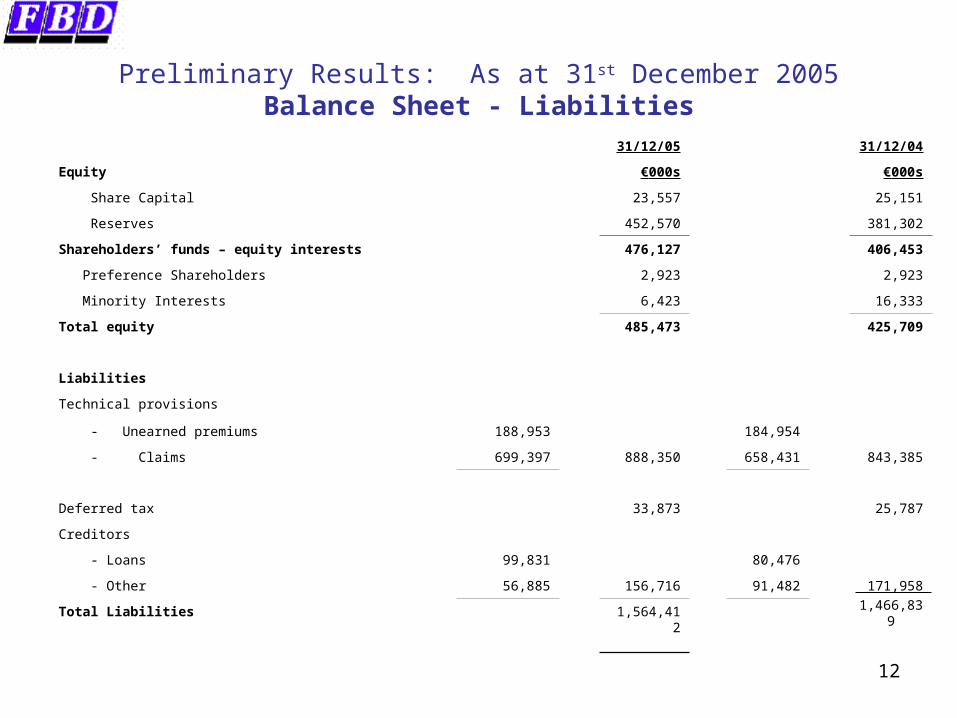

Preliminary Results: As at 31st December 2005Balance Sheet - Liabilities

31/12/05 31/12/04

Equity €000s €000s

Share Capital 23,557 25,151

Reserves 452,570 381,302

Shareholders’ funds – equity interests 476,127 406,453

Preference Shareholders 2,923 2,923

Minority Interests 6,423 16,333

Total equity 485,473 425,709

Liabilities

Technical provisions

- Unearned premiums 188,953 184,954

- Claims 699,397 888,350 658,431 843,385

Deferred tax 33,873 25,787

Creditors

- Loans 99,831 80,476

- Other 56,885 156,716 91,482 171,958

1,466,839Total Liabilities 1,564,412

13

Preliminary Results: Year to 31st December 2005Statement of Changes in Equity

31/12/05 31/12/04

€000s €000s

Balance at 1st January 425,709 326,696

Profit for the year 161,454 115,008

Gain on available-for-sale investments 10,196 4,681

Re-issue of ordinary shares 1,409 2,716

Buyback of own shares (81,238) -

Dividends paid (18,158) (12,614)

Purchase of minority interests (9,864) (495)

Actuarial loss on pension fund revaluation (3,802) (9,031)

Other (233) (1,252)

Balance at 31st December 485,473 425,709

14

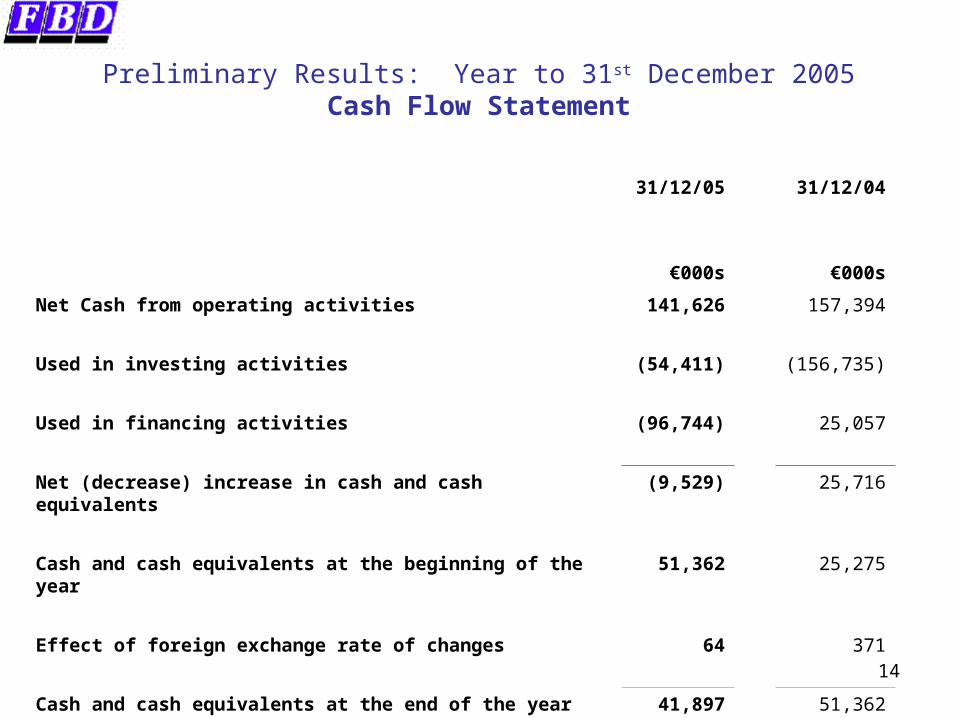

Preliminary Results: Year to 31st December 2005Cash Flow Statement

31/12/05 31/12/04

€000s €000s

Net Cash from operating activities 141,626 157,394

Used in investing activities (54,411) (156,735)

Used in financing activities (96,744) 25,057

Net (decrease) increase in cash and cash equivalents (9,529) 25,716

Cash and cash equivalents at the beginning of the year 51,362 25,275

Effect of foreign exchange rate of changes 64 371

Cash and cash equivalents at the end of the year 41,897 51,362

15

5 Year Financial Performance

2001 2002 2003 2004 2005 01/05

€000s €000s €000s €000s €000s % Inc

Gross written premiums 247,959 325,809 368,619 351,448 389,472 57%

Net earned premiums 192,864 240,325 290,320 296,237 332,371 72%

Underwriting result (15,088) (5,266) 60,967 65,939 90,450

Operating profit 30,184 37,531 110,456 124,724 162,624 439%

16

5 Year Financial Performance

2001 2002 2003 2004 2005

% % % % %

Loss ratio 94.9 91.8 66.5 66.7 60.9

Net expense ratio 12.9 10.4 12.5 11.0 11.9

Combined ratio 107.8 102.2 79.0 77.7 72.8

17

5 Year Financial Performance

2001 2002 2003 2004 2005 01/05

Cent Cent Cent Cent Cent % Inc

Operating earnings per share 59.59 75.34 227.38 256.18 363.54 510%

Dividend per share 19.50 22.00 27.50 40.00 57.50 195%

Net asset value per share 483.11 510.13 701.94 969.64 1,250.62 159%

18

Return on equity

2003 2004 2005

Underwriting 50.75% 43.78% 53.08%

Non underwriting 13.68% 8.63% 11.63%

Total 35.09% 31.61% 36.53%

19

Gross Claims Run-off

699245152105805065Claims outstanding

(84)(126)(101)(118)(118)(1,083)Cumulative payments

3292782061981681,148Estimate of cumulative claims

----168-Four years later

---198182-Three years later

--206209198-Two years later

-278225222201-One year later

329329262270205-

At end of underwriting year

Estimate of cumulative claims:

Outstanding

Claims

31/12/05

€ m

2005

€ m

2004

€ m

2003

€ m

2002

€ m

2001

€ m

Prior

Years

€ m

699245152105805065Claims outstanding

(84)(126)(101)(118)(118)(1,083)Cumulative payments

3292782061981681,148Estimate of cumulative claims

----168-Four years later

---198182-Three years later

--206209198-Two years later

-278225222201-One year later

329329262270205-

At end of underwriting year

Estimate of cumulative claims:

Outstanding

Claims

31/12/05

€ m

2005

€ m

2004

€ m

2003

€ m

2002

€ m

2001

€ m

Prior

Years

€ m

20

Market share (IIF) Gross written Premium

248

326

369

352

390

3229

3954

4176

4000

3900

2001

2002

2003

2004

2005

FBD Rest of Market

10%

8.8%

8.8%

8.2%

7.7%

€ m

21

Post Balance Sheet Events

• 23rd February 2006,

– Conditional agreement to sell 96 hectares of development land at La Cala

– Total consideration €201m. in cash, in phased payments.

– Estimated profit after tax… €90 m.

– Intention to distribute the net cash proceeds, estimated at €120m. in two special dividends.

22

OUTLOOK

Underwriting

• Year to date trading on target

• Price competition continues

• Ambitious new-business volumes targeted

• Further investment in people and infrastructure planned

• Road accident trends negative, pending Government action

• Increased claims incurred charge….higher exposures

• No significant changes in claims reserving approach envisaged, in the short term

• Combined ratio to move towards European norms

23

OUTLOOK…Contd.

Non -Underwriting

• Property / Leisure– Operating environment to remain challenging– New marketing strategies being implemented

• Financial Services– Falling premiums pressurising income– Increased sales activity planned

24

OUTLOOK…Contd.

Capital Retained

• Increasing dividend payout

• Opportunities to invest capital in core / related financial service businesses to be investigated

• All options to maximise returns to shareholders under ongoing review…….

• ………meanwhile , prudent investment.