0 Wake Forest Case Competition Canyons Craft Soda Team: Eshna Bhaduri, Joshua Golub, Matt Niemczak,...

16

1 Wake Forest Case Competition Canyons Craft Soda Team: Eshna Bhaduri, Joshua Golub, Matt Niemczak, Shawn Tydlaska, & Victoria Hon

-

Upload

christal-skinner -

Category

Documents

-

view

229 -

download

0

Transcript of 0 Wake Forest Case Competition Canyons Craft Soda Team: Eshna Bhaduri, Joshua Golub, Matt Niemczak,...

1

Wake Forest Case Competition

Canyons Craft Soda Team:

Eshna Bhaduri, Joshua Golub, Matt Niemczak, Shawn Tydlaska, & Victoria Hon

1. Executive Summary

2. Situational Assessment

3. New Product Introduction

4. Right to Play, Right to Win

5. Consumer Engagement & Execution Plan

6. Impact Assessment

7. Appendix

Agenda

3

Executive Summary

Source: 1Mintel Report – “Carbonated Soft Drinks – US – June 2014”

4

Observed Market Trends

Declining Sales and Margins1 Increased Health Concerns Millennials and the Digital Age

Impacts on CSD market

• U.S. CSD sales projected to decline by 2.5% from 2009-2018

• Consumers are switching to natural drinks, like coffee, water, tea, and milk (See Exhibit 4)

• Gross margins are compressing• Pepsi down 0.9%, • Coke down 2.8% • Dr. Pepper down 1.9%

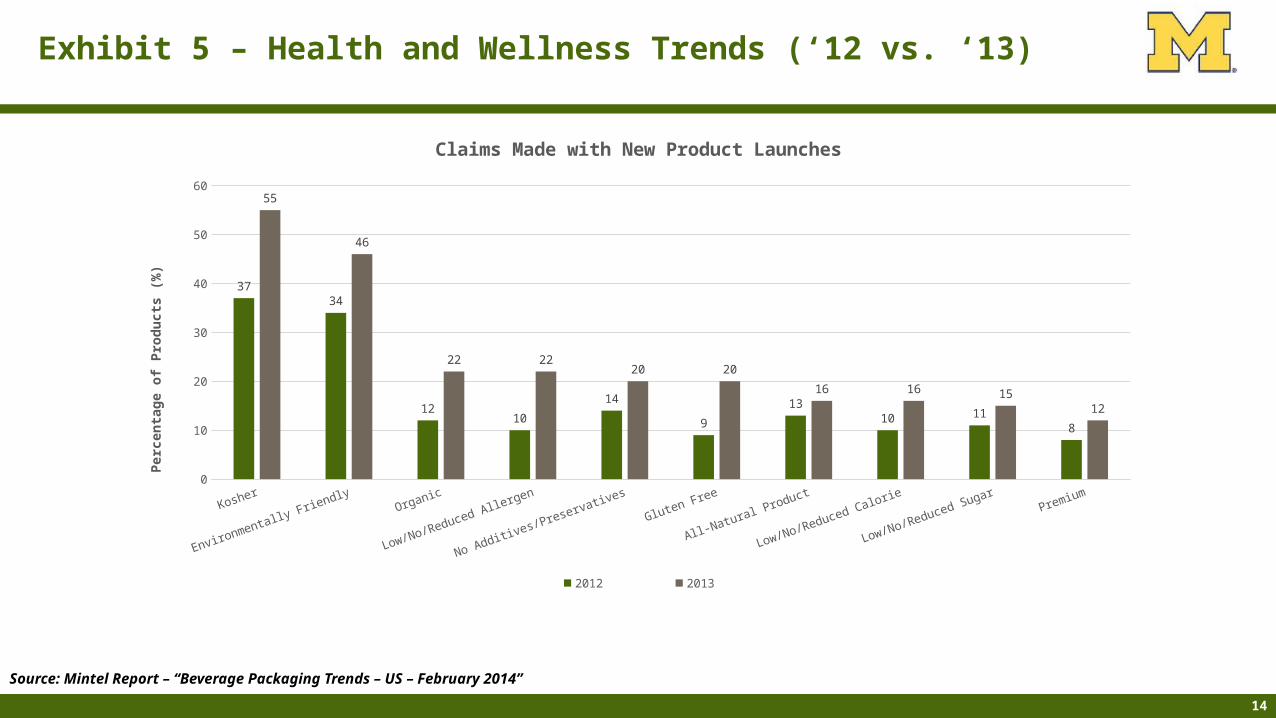

• New product launches promoting health claims is growing (2013 vs. 2014)3:• Organic up 83%• No Additives up 43%• Gluten Free up 122%• All-Natural up 23%• Lower Sugar up 36%• Premium up 50%

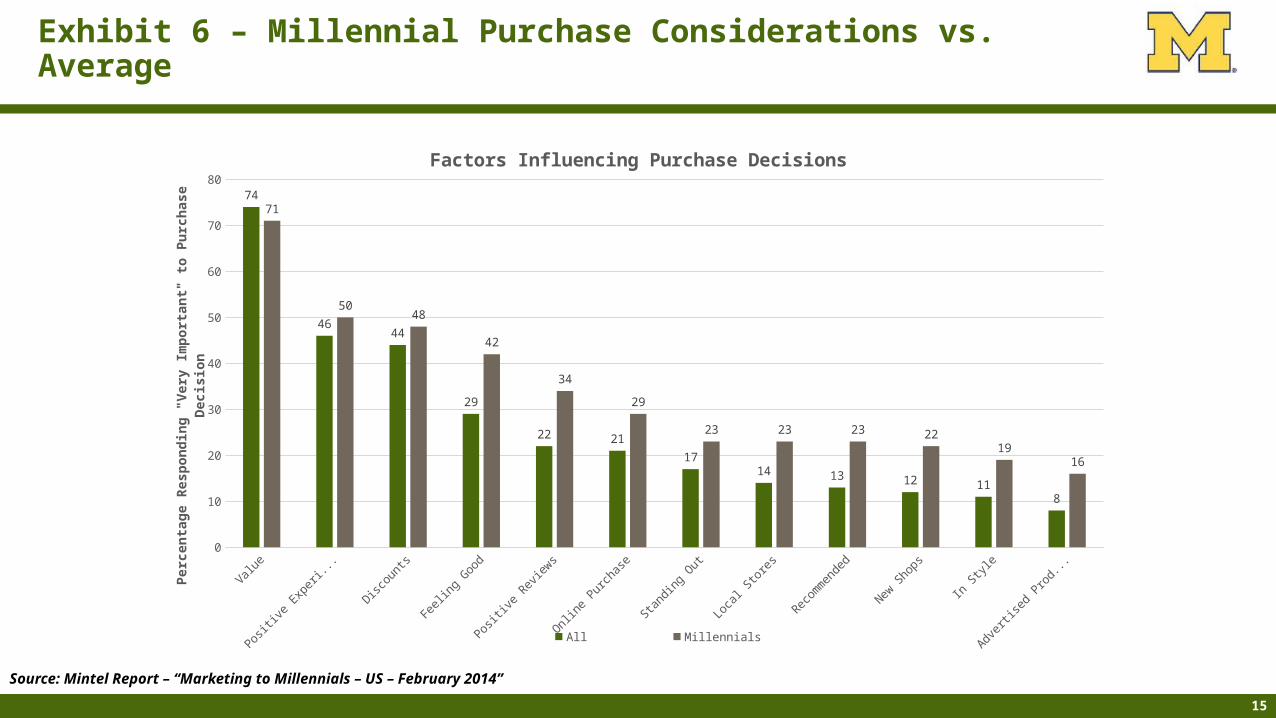

• Compared to the general population, millennials prefer4:• “Feel Good” Products: 42% vs 29%• Online Reviews: 34% vs 22%• Standing Out: 23% vs 17%• Local Stores: 23% vs 14%• Unique Stores: 22% vs 12%• Being in Style: 19% vs 11%

Opportunities

• Meet customers in the market by reformulating and launching new product

• Craft soda market is just 1% of the CSD category and comparable brands have projected revenue increases of 15% per year2

• Offer a healthier product with more natural ingredients and less processed sugar

• Build consumer loyalty by focusing on experiential aspects of usage occasions

• Engage consumers to co-create and collaborate on brand’s image and identity

Shifts in the CSD market create new opportunities for growth and innovation

Sources: 1Mintel Report – “Carbonated Soft Drinks – US – June 2014”; 2http://www.cnbc.com/id/101875502; 3Mintel Report – “Beverage Packaging Trends – US – February 2014”; 4Mintel Report – “Marketing to Millennials – US – February 2014” ; Yahoo Finance

5

To take advantage of shifting trends, Avalanche should enter the craft soda market with “Canyons Craft” soda

Millennial Trends

Indulgences

Unique Flavors

Artisanal

Artisanal Soda with Natural Ingredients

Packaged in Cans with Trendy Artwork

Occasions for Soda

Refreshment

Socializing

Energy

Industry Trends

Craft Beverages

Natural Ingredients

Innovative Packaging

By entering the Craft soda category, Avalanche can offer a differentiated product that satisfies key drinking occasions and takes advantage of the emerging millennial trends

Sources: Mintel Report – “Carbonated Soft Drinks – US – June 2014”; Mintel Report – “Marketing to Millennials – US – February 2014”

“Canyons Craft Soda”

6

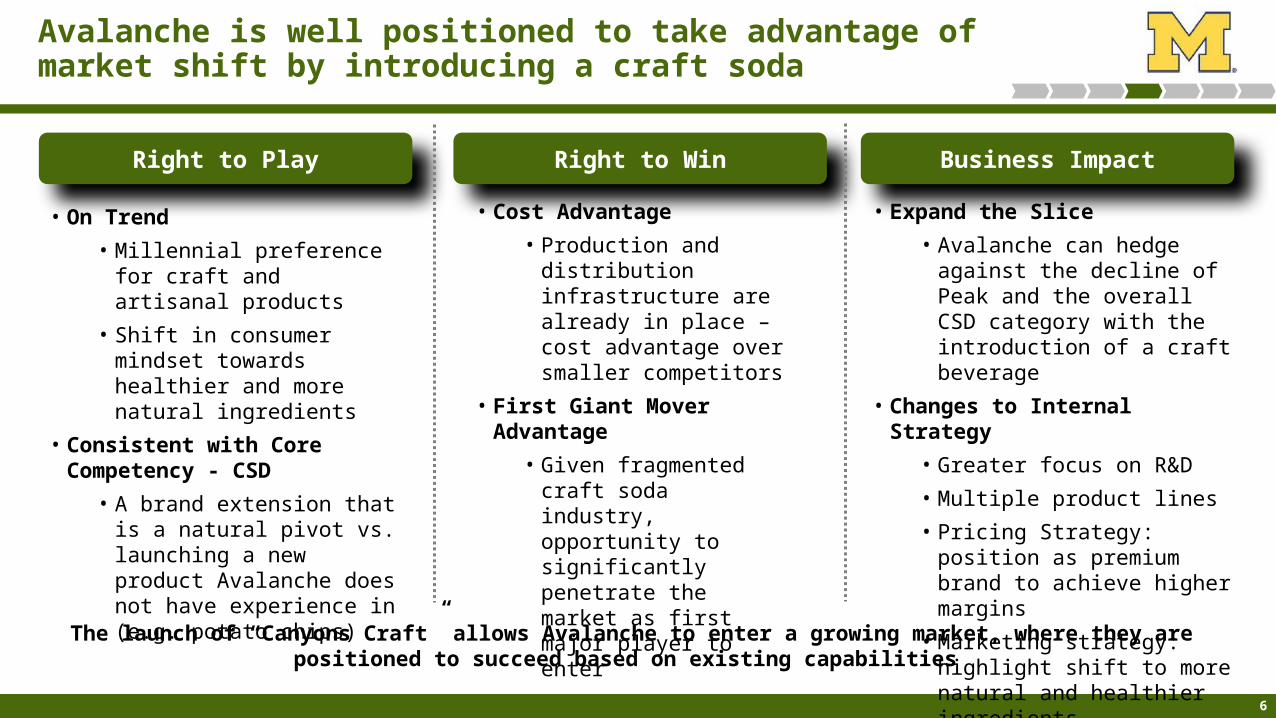

Right to Win Business ImpactRight to Play

• On Trend

• Millennial preference for craft and artisanal products

• Shift in consumer mindset towards healthier and more natural ingredients

• Consistent with Core Competency - CSD

• A brand extension that is a natural pivot vs. launching a new product Avalanche does not have experience in (e.g. potato chips)

• Cost Advantage

• Production and distribution infrastructure are already in place – cost advantage over smaller competitors

• First Giant Mover Advantage

• Given fragmented craft soda industry, opportunity to significantly penetrate the market as first major player to enter

• Expand the Slice

• Avalanche can hedge against the decline of Peak and the overall CSD category with the introduction of a craft beverage

• Changes to Internal Strategy

• Greater focus on R&D

• Multiple product lines

• Pricing Strategy: position as premium brand to achieve higher margins

• Marketing strategy: highlight shift to more natural and healthier ingredients

Avalanche is well positioned to take advantage of market shift by introducing a craft soda

The launch of “Canyons Craft” allows Avalanche to enter a growing market, where they are positioned to succeed based on existing capabilities

7

Traditional Marketing Tactics Millennial Consumer Engagement Plan

Focus on Digital Content• Generate consumable media content to build brand awareness • Utilize music platforms (Pandora, iTunes) and create branded playlists• Develop mini show series or video shorts to increase engagement

Encourage User-Generated Content and Co-creation• Utilize social media platforms to encourage sharing and peer discovery

(Ex: Pinterest, Instagram, Twitter - #CanyonsCraft)• Engage with local artists to customize product packaging designs• Invite heavy users and food industry mavens to co-create product flavors

Experiential Campaigns • To capture consumers loyalty, invite them to be a part of brand mission • Create brand experience around an active, adventure seeking lifestyle to

compliment brand image

National TV

Digital Display

Avalanche should develop a targeted digital marketing campaign that compliments traditional marketing tactics

Execute targeted approach along traditional channels to reach millennial consumers

Focus on utilizing digital platforms to facilitate brand awareness and build the brand experience

Source: Mintel Report – “Marketing to Millennials – US – February 2014”

8

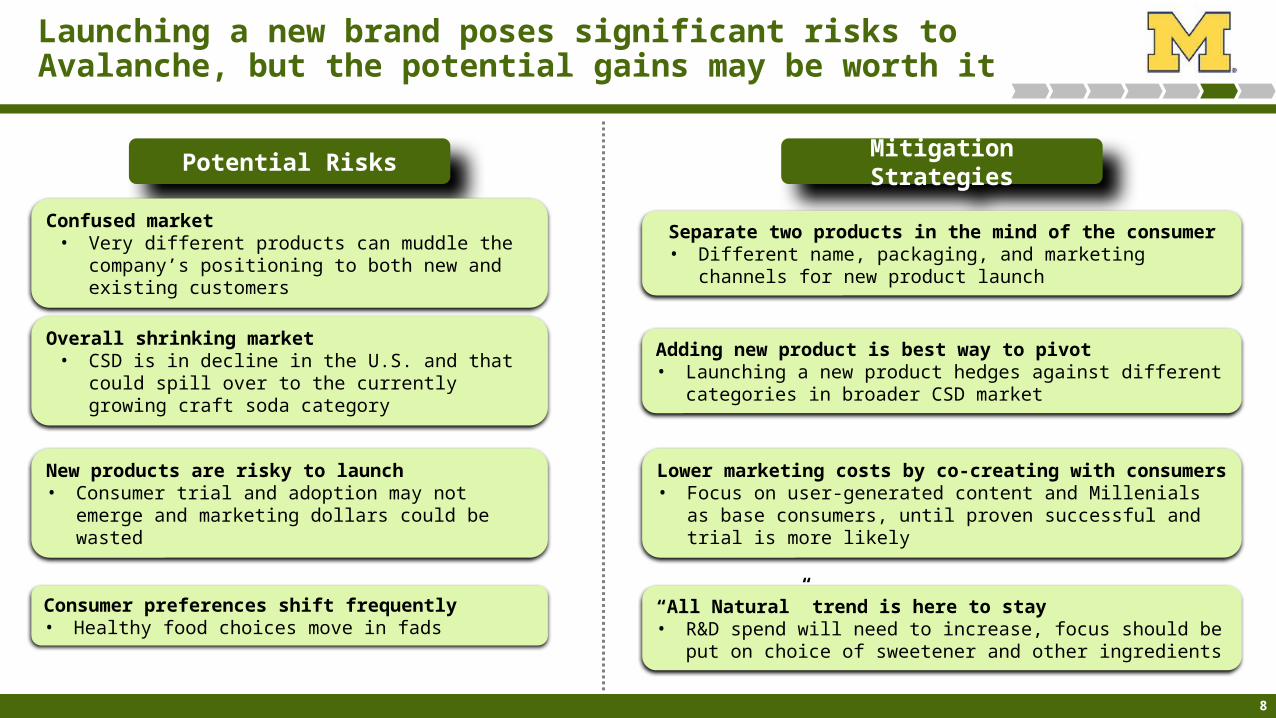

Launching a new brand poses significant risks to Avalanche, but the potential gains may be worth it

Potential Risks Mitigation Strategies

Confused market• Very different products can muddle the company’s

positioning to both new and existing customers

Overall shrinking market• CSD is in decline in the U.S. and that could spill over

to the currently growing craft soda category

Separate two products in the mind of the consumer• Different name, packaging, and marketing channels for new

product launch

Adding new product is best way to pivot • Launching a new product hedges against different categories in

broader CSD market

New products are risky to launch • Consumer trial and adoption may not emerge and

marketing dollars could be wasted

Lower marketing costs by co-creating with consumers• Focus on user-generated content and Millenials as base

consumers, until proven successful and trial is more likely

Consumer preferences shift frequently• Healthy food choices move in fads

“All Natural” trend is here to stay• R&D spend will need to increase, focus should be put on choice

of sweetener and other ingredients

9

Appendix

10

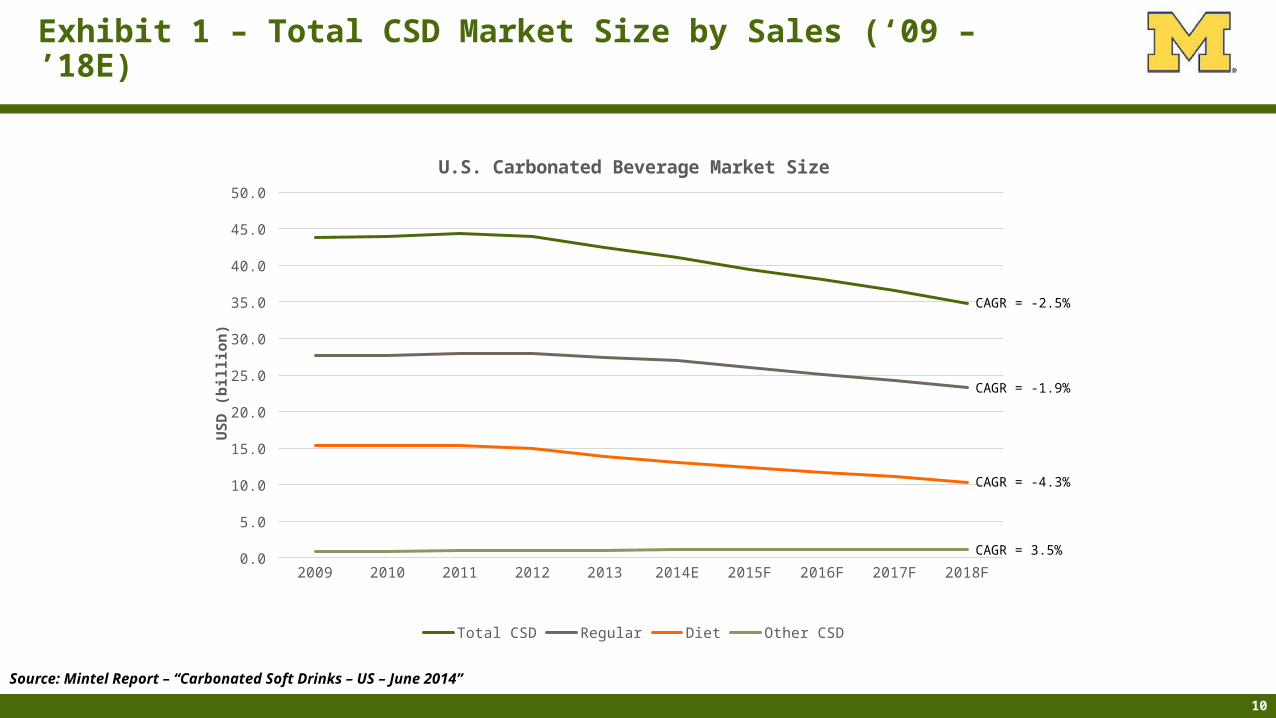

Exhibit 1 – Total CSD Market Size by Sales (‘09 – ’18E)

2009 2010 2011 2012 2013 2014E 2015F 2016F 2017F 2018F0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

U.S. Carbonated Beverage Market Size

Total CSD Regular Diet Other CSD

US

D (

bill

ion

)

CAGR = -2.5%

CAGR = -1.9%

CAGR = -4.3%

CAGR = 3.5%

Source: Mintel Report – “Carbonated Soft Drinks – US – June 2014”

11

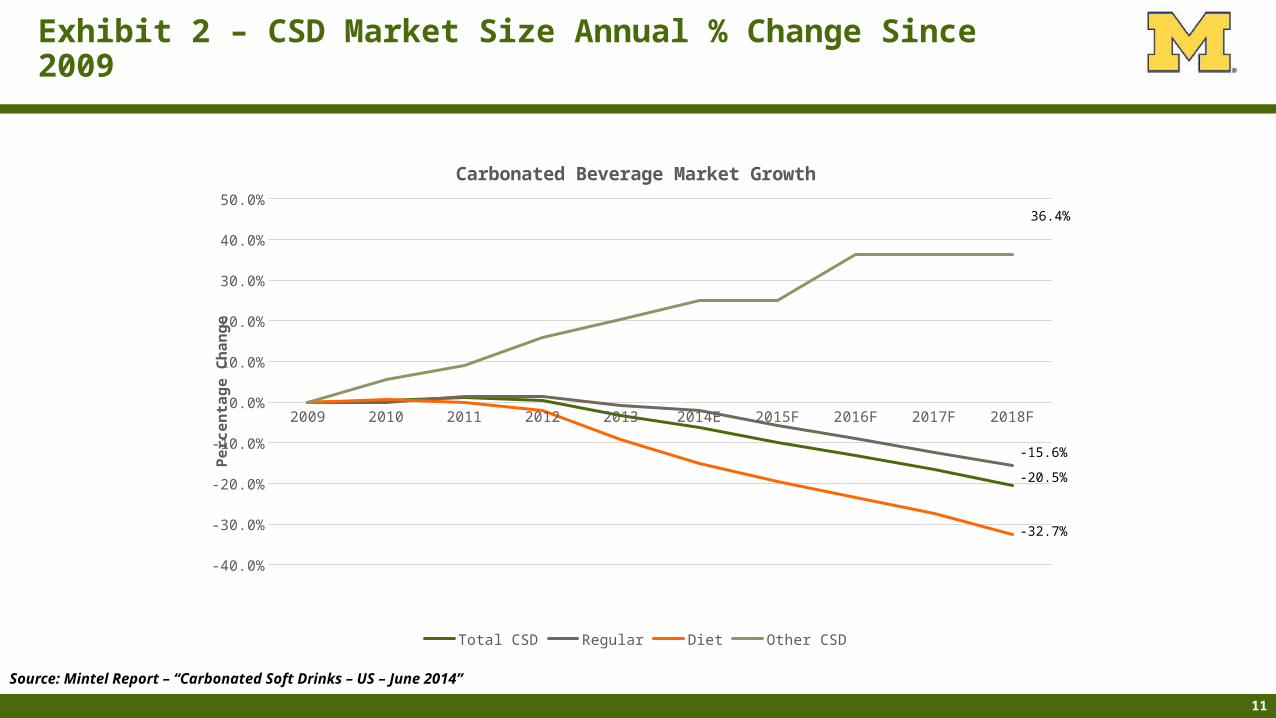

Exhibit 2 – CSD Market Size Annual % Change Since 2009

2009 2010 2011 2012 2013 2014E 2015F 2016F 2017F 2018F

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Carbonated Beverage Market Growth

Total CSD Regular Diet Other CSD

Per

cen

tag

e C

han

ge

36.4%

-15.6%

-20.5%

-32.7%

Source: Mintel Report – “Carbonated Soft Drinks – US – June 2014”

12

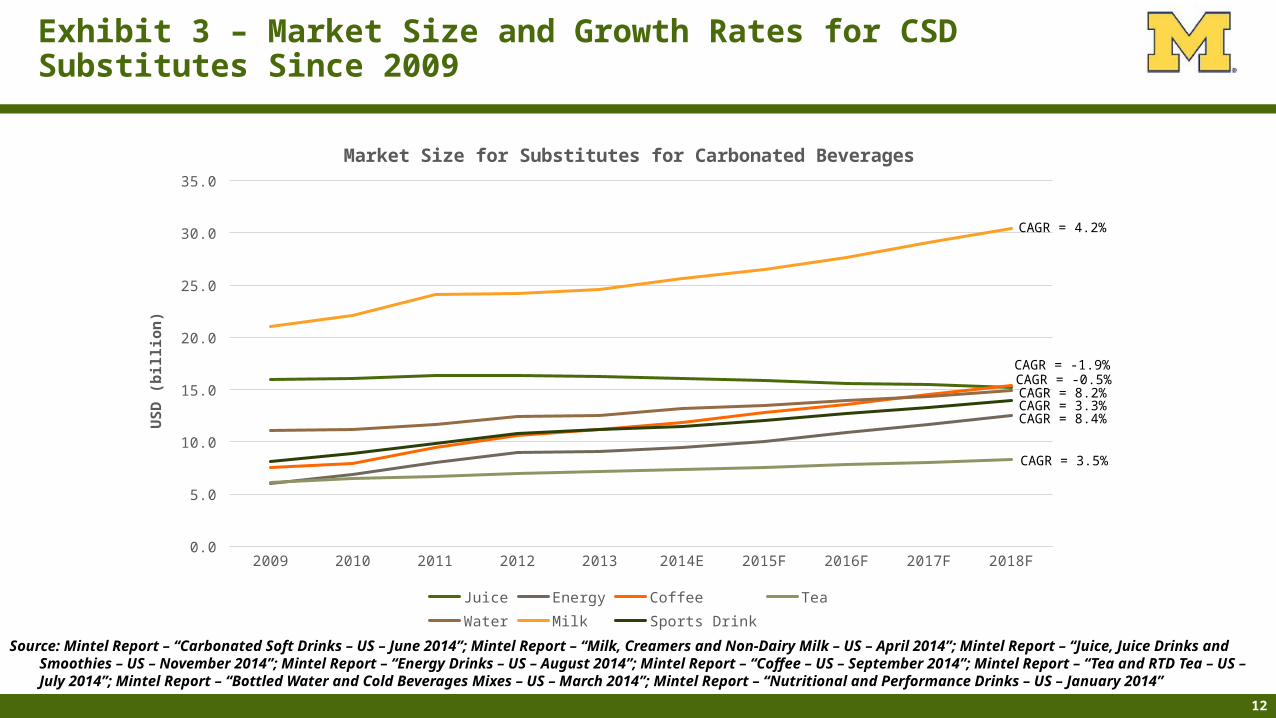

Exhibit 3 – Market Size and Growth Rates for CSD Substitutes Since 2009

2009 2010 2011 2012 2013 2014E 2015F 2016F 2017F 2018F0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Market Size for Substitutes for Carbonated Beverages

Juice Energy Coffee Tea Water Milk Sports Drink

US

D (

bill

ion

)

CAGR = -1.9%

CAGR = 4.2%

CAGR = -0.5%CAGR = 8.2%CAGR = 3.3%CAGR = 8.4%

CAGR = 3.5%

Source: Mintel Report – “Carbonated Soft Drinks – US – June 2014”; Mintel Report – “Milk, Creamers and Non-Dairy Milk – US – April 2014”; Mintel Report – “Juice, Juice Drinks and Smoothies – US – November 2014”; Mintel Report – “Energy Drinks – US – August 2014”; Mintel Report – “Coffee – US – September 2014”; Mintel Report – “Tea and RTD Tea – US – July 2014”; Mintel Report – “Bottled Water and Cold Beverages Mixes – US – March 2014”; Mintel Report – “Nutritional and Performance Drinks – US – January 2014”

13

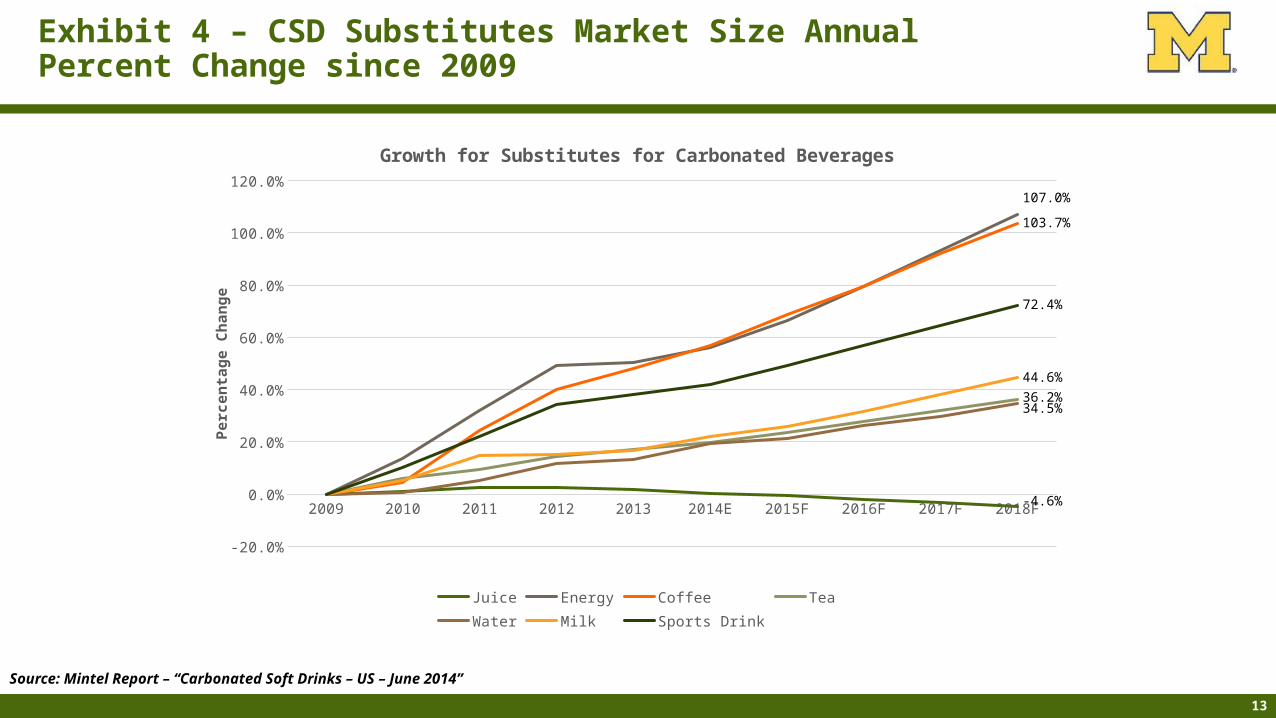

Exhibit 4 – CSD Substitutes Market Size Annual Percent Change since 2009

2009 2010 2011 2012 2013 2014E 2015F 2016F 2017F 2018F

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

Growth for Substitutes for Carbonated Beverages

Juice Energy Coffee Tea

Water Milk Sports Drink

Per

cen

tag

e C

han

ge

107.0%

-4.6%

103.7%

72.4%

44.6%

36.2%34.5%

Source: Mintel Report – “Carbonated Soft Drinks – US – June 2014”

14

Kosher

Environmentally FriendlyOrganic

Low/No/Reduced Allergen

No Additives/Preservatives

Gluten Free

All-Natural Product

Low/No/Reduced Calorie

Low/No/Reduced SugarPremium

0

10

20

30

40

50

60

3734

1210

14

9

1310 11

8

55

46

22 2220 20

16 16 1512

Claims Made with New Product Launches

2012 2013

Per

cen

tag

e o

f P

rod

uct

s (%

)

Exhibit 5 – Health and Wellness Trends (‘12 vs. ‘13)

Source: Mintel Report – “Beverage Packaging Trends – US – February 2014”

15

Exhibit 6 – Millennial Purchase Considerations vs. Average

Value

Positiv

e Exp

erie

nce

Discou

nts

Feel

ing

Good

Positiv

e Rev

iews

Onlin

e Pur

chas

e

Stand

ing

Out

Loca

l Sto

res

Recom

men

ded

New S

hops

In S

tyle

Adver

tised

Pro

ducts

0

10

20

30

40

50

60

70

80

74

4644

29

22 21

1714 13 12 11

8

71

5048

42

34

29

23 23 23 2219

16

Factors Influencing Purchase Decisions

All Millennials

Per

cen

tag

e R

esp

on

din

g "

Ver

y Im

po

rtan

t" t

o P

urc

has

e D

ecis

ion

Source: Mintel Report – “Marketing to Millennials – US – February 2014”

16

Exhibit 7 - Occasions For Drinking Soda

Soda Drinking Occasion

What is the Soda For? Important Traits in SodaUnimportant Traits in Soda

FitnessWhen you need a little extra boost to get through the workout

Energy Low caloric content

ProfessionalWhen work is getting long and you’ve hit a wall

Taste, Energy, & Appearance

Size/Quantity

AlcoholEither to kick off a night…or just keep it going

Taste, Size, & Energy Low caloric content

Everyday UseWhen you want to indulge with something sweet

Taste, Refreshment, & Low caloric content

Appearance & Energy

Social SettingTo keep the party going, but not with alcohol

Taste & AppearanceEnergy & Low caloric

content